0% APR vs cash rebate: which is better for car buyers? The better option is the one that leaves you paying less overall, not the one with the flashier ad. In general, 0% APR is stronger when you qualify for promotional financing and keep the loan for the full term. A cash rebate is stronger when it lowers the amount financed enough to beat the interest you would pay on a low-rate loan. The CFPB says buyers should compare APR, interest rate, loan term, and total amount financed, not just the monthly payment.

0% APR vs Cash Rebate: Which Is Better for Car Buyers Who Care About Total Cost?

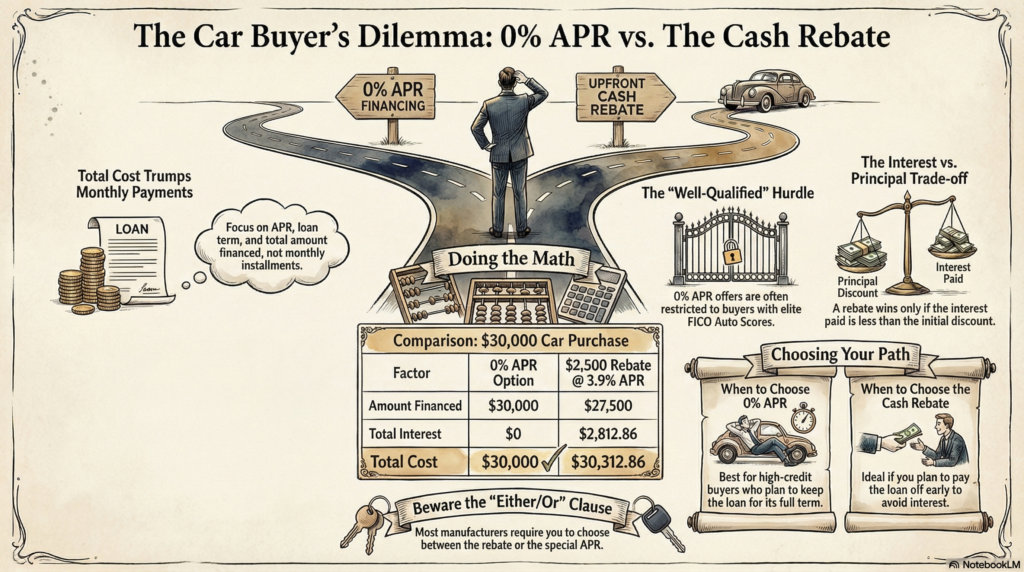

Before you choose, compare these five things:

- total amount financed

- APR

- loan term

- total cost over the life of the loan

- whether the offer is limited to qualified buyers

These are the same decision points the CFPB highlights when comparing auto loan offers, and official automaker pages also show that the lowest promotional APR is usually limited to qualified or well-qualified buyers.

Here is a simple example. Suppose a car is priced at $30,000 and you can choose either 0% APR for 60 months or a $2,500 rebate with a 3.9% APR loan on $27,500. At 3.9% for 60 months, the payment is about $505.21 and the total interest is about $2,812.86, so the rebate option ends up costing about $30,312.86 in total. In that example, the 0% APR offer is cheaper by about $313 overall. That is exactly why buyers should compare the full loan math rather than the headline offer alone.

A rebate can still win when the discount is bigger, the replacement APR is lower, or you expect to pay the loan off early. But if the interest cost over time is larger than the rebate benefit, the “discount” is not really the better deal.

How to Decide Between 0% APR and a Cash Rebate

- Choose 0% APR first if you qualify for promotional financing and plan to keep the loan for the full term

- Choose a cash rebate first if it meaningfully lowers the price and the replacement APR is still low

- Recheck the math if you may pay off the loan early

- Confirm whether taking 0% APR means giving up other discounts or incentives

- Compare the total cost, not just the monthly payment

When 0% APR Is Usually Better

0% APR is often better for buyers who have strong credit, want fixed and predictable payments, and qualify for a manufacturer-backed promotion on a selected new vehicle. Toyota’s current finance pages explicitly say these low-APR offers are generally for well-qualified customers or very well-qualified buyers, which shows how selective these deals can be.

Buyers should also check whether a cash rebate can be combined with a dealer discount or whether accepting special financing replaces other savings. In some offers, the rebate is an alternative to promotional APR, while in others it may also affect negotiated price flexibility. That is why the best deal is not just about the rebate amount itself, but about how the full offer changes the final sale price and total loan cost.

0% APR vs Cash Rebate: Which Is Better for Car Buyers with Strong Credit?

If you have strong credit, 0% APR is usually the first option worth testing, but you still should not assume it wins automatically. myFICO explains that lenders may use industry-specific FICO Auto Scores, and that your lender may use a different FICO score version than the one you see yourself. In plain terms, that means your “good score” in a consumer app may not be the exact score used for your car-loan decision.

The CFPB also notes that lenders look beyond score alone. They may price loans using your credit history, current debt, income, and down payment, so two buyers with similar scores can still get different offers.

When a Cash Rebate Is Usually Better

A cash rebate is often better when it creates a meaningful upfront price cut and the replacement loan still has a reasonable APR. It can also be the stronger option for buyers who do not qualify for the lowest promotional financing tier. In that case, the rebate may lower the amount financed enough to reduce total cost, even though the loan still carries interest.

Rebates can also matter more if you plan to pay the loan off early, because a lower principal means less interest builds over time. If you plan to pay the loan off early, a cash rebate can become more attractive because the lower amount financed may reduce your total interest cost before the full loan term ends. That does not make rebates automatically better; it just means the better option depends on the structure of the deal, not the marketing headline.

What to Verify Before Signing

Before you sign, check the final sale price, rebate amount, APR, loan term, monthly payment, total amount financed, and total cost over the life of the loan. Also confirm whether choosing 0% APR means giving up a cash rebate, dealer discount, or another incentive. Read the offer terms carefully to see whether the promotion applies only to certain models, loan lengths, or qualified buyers. A deal is only as good as the full paperwork, so make sure the final contract matches the offer you were shown.

How This Article Was Prepared

This article was prepared using current guidance from the Consumer Financial Protection Bureau, myFICO, and Toyota’s finance offers. The information was cross-checked to compare how these sources describe APR vs interest rate, loan comparison factors, auto-specific score models, and the qualification language used in real promotional financing offers.

FAQs

Is 0% APR always better than a cash rebate?

No. A 0% offer wins only when the interest savings are greater than the value of the rebate you give up. The right choice depends on the APR, loan term, rebate amount, and total cost.

Can I get both a rebate and 0% APR?

Usually not, but promotions vary by automaker and model. Many offers make buyers choose between special financing and a cash incentive. Check the offer terms carefully before assuming you can combine both.

What is a FICO Auto Score, and why does it matter?

A FICO Auto Score is a version of the FICO score designed for auto lending. Some lenders use it instead of a general score, which is why your car-loan result may differ from the score you usually see online.

What do lenders verify besides my credit score?

Lenders may also review your income, debt level, credit history, down payment, and loan amount when setting financing terms. A strong score helps, but it does not guarantee the best promotional offer by itself.

Does paying off the loan early make the rebate better?

Sometimes. If you pay the loan off early, a cash rebate can become more attractive because the lower amount financed may reduce the total interest you pay before the full-term ends.

Can dealer discounts be combined with a rebate?

Sometimes, but not always. Some offers let buyers stack a rebate with a negotiated discount, while others make the rebate a replacement for other savings. Always check the full offer terms before assuming the deals combine.

Should I get preapproved before choosing between 0% APR and a rebate?

Yes, preapproval can help you compare the manufacturer offer against a real outside loan option. That makes it easier to judge whether the rebate plus outside financing is actually better than the promotional APR.

Bottom Line

For most shoppers, the best approach is simple: compare 0% APR vs cash rebate using the APR, loan term, amount financed, and total cost. If you qualify for true promotional financing, 0% APR can be the better deal. If the rebate is large enough and the replacement rate is still low, the rebate may win. The smartest buyer compares the math first and the marketing second.

This article is for general educational purposes and is not personal financial advice.