Introduction

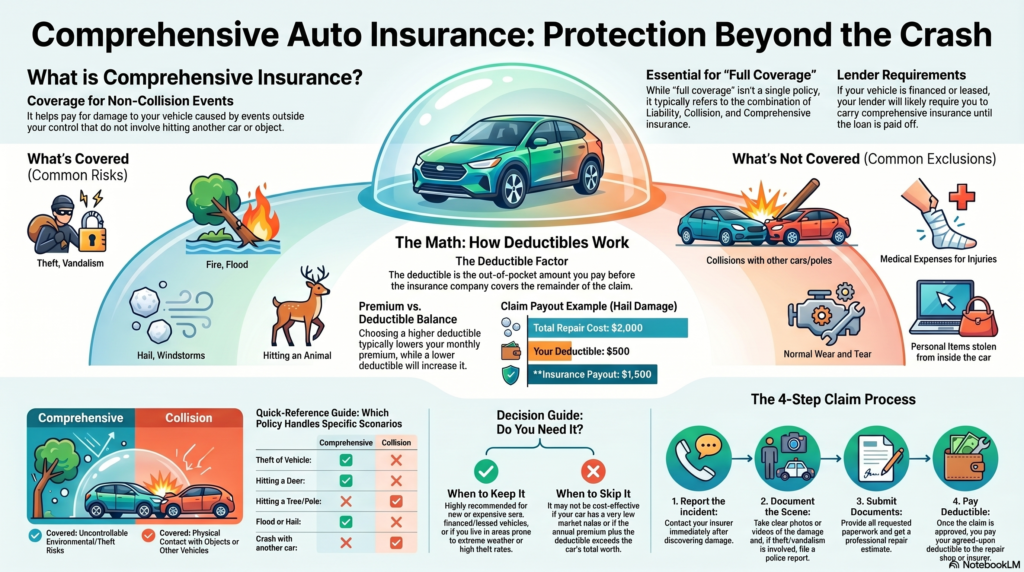

Comprehensive insurance is a type of auto insurance coverage that helps pay for damage to your vehicle from events other than a collision. These events may include theft, vandalism, fire, flood, hail, falling objects, windstorms, and animal damage.

According to the Insurance Information Institute, comprehensive coverage protects your car from damage caused by disasters “other than collisions.” The National Association of Insurance Commissioners also explains that comprehensive coverage may include theft, hail, windstorm, flood, fire, and animal impact.

Coverage can vary by insurer, state, country, and policy terms. For this reason, you should always read the policy details before buying comprehensive car insurance.

What Is Comprehensive Insurance?

Comprehensive insurance, also called comprehensive coverage, protects your vehicle from covered damage that is not caused by a crash with another vehicle or object.

In simple words, comprehensive insurance helps cover damage from events outside your control, such as theft, fire, flood, hail, vandalism, falling objects, and animal damage.

The NAIC auto insurance guide explains that collision coverage pays for physical damage caused by your car colliding with another object, while comprehensive coverage applies to many non-collision losses.

Comprehensive insurance is commonly part of an auto insurance policy. It should not be confused with health insurance, life insurance, or business insurance.

How Does Comprehensive Insurance Work?

Comprehensive insurance usually works with a deductible. A deductible is the amount you pay before your insurer pays the approved claim amount.

Example calculation

If your car is damaged by hail and the repair cost is $2,000:

| Item | Amount |

| Repair cost | $2,000 |

| Deductible | $500 |

| Insurance payout | $1,500 |

| Your out-of-pocket cost | $500 |

Calculation:

$2,000 repair cost − $500 deductible = $1,500 insurance payout.

The NAIC consumer guide explains that deductible choices can affect your premium. A higher deductible often lowers the premium, while a lower deductible usually increases it.

What Does Comprehensive Insurance Cover?

Comprehensive insurance may cover several types of non-collision damage, depending on your policy.

Common covered risks include:

- Theft

- Fire

- Flood

- Hail

- Windstorm

- Vandalism

- Falling objects

- Animal damage

- Glass or windshield damage

The Insurance Information Institute lists theft, vandalism, fire, flood, hail, falling rocks or trees, and animal damage as common examples of comprehensive coverage.

What Is Not Covered by Comprehensive Insurance?

Comprehensive insurance does not usually cover every type of vehicle loss.

It typically does not cover:

- Damage from collision with another vehicle

- Damage from hitting an object such as a tree or pole

- Medical expenses

- Liability for injury or damage caused to others

- Normal wear and tear

- Mechanical breakdown

- Personal belongings stolen from the vehicle

For crash-related vehicle damage, collision coverage is usually required. The NAIC explains that collision coverage pays for physical damage when your auto collides with an object, such as another car or a tree.

Comprehensive Insurance vs Collision Insurance

Comprehensive and collision insurance are both physical damage coverages, but they cover different causes of loss.

| Feature | Comprehensive Insurance | Collision Insurance |

| Theft | Usually covered | Not usually covered |

| Fire | Usually covered | Not usually covered |

| Flood or hail | Usually covered | Not usually covered |

| Animal impact | Usually covered | Not usually covered |

| Crash with another car | Not usually covered | Usually covered |

| Hit a tree or pole | Not usually covered | Usually covered |

The NAIC explains that comprehensive coverage applies to losses other than collision, while collision coverage applies when your vehicle collides with another object.

Comprehensive Insurance vs Full Coverage

“Full coverage” is not a single standard insurance policy. It usually refers to a combination of:

- Liability insurance

- Collision insurance

- Comprehensive insurance

The NAIC states that if you have an auto loan, your lender may require both comprehensive and collision coverage.

Full coverage does not mean every possible risk is covered. Every policy has limits, exclusions, deductibles, and conditions.

How Much Does Comprehensive Insurance Cost?

The cost of comprehensive insurance depends on multiple factors, including:

- Vehicle value

- Location

- Deductible amount

- Claim history

- Insurance provider

- Coverage limits

- Local risks such as theft, flood, hail, storms, or wildlife

I cannot confirm one fixed cost for comprehensive insurance because insurance prices vary by insurer, vehicle, driver profile, location, and policy terms.

The NAIC consumer auto insurance guide recommends comparing coverage, limits, deductibles, and insurer licensing before buying a policy.

Example of a Comprehensive Insurance Claim

Here is another simple example.

Your parked car is damaged by a falling tree branch.

| Item | Amount |

| Repair cost | $3,000 |

| Deductible | $750 |

| Insurance payout | $2,250 |

| Your out-of-pocket cost | $750 |

Calculation:

$3,000 repair cost − $750 deductible = $2,250 insurance payout.

This is only an example. Actual payouts depend on your policy, deductible, covered event, repair estimate, and vehicle value.

When Should You Buy Comprehensive Insurance?

Comprehensive insurance may be useful if:

- Your vehicle is financed or leased

- Your car is new or expensive

- You live in an area with theft risk

- You live in an area with flood, hail, fire, storm, or wildlife risk

- You cannot afford to repair or replace your vehicle after a covered loss

The NAIC explains that lenders may require comprehensive and collision coverage if you have an auto loan.

If you are managing multiple financial responsibilities, you can also read our guide on the smart benefits of refinancing private student loans to understand how refinancing may affect monthly financial planning.

Who May Not Need Comprehensive Insurance?

Comprehensive insurance may not be cost-effective for every vehicle.

You may consider skipping it if:

- Your vehicle has a very low market value

- Your deductible and premium are high compared with the car’s value

- You can afford to repair or replace the car yourself

- You do not have a lender or leasing company requiring the coverage

The Mississippi Insurance Department advises comparing the cost of coverage with the value of your car before making a decision.

Is Comprehensive Insurance Required by Law?

Comprehensive insurance is generally not required by law. However, a lender or leasing company may require it if your vehicle is financed or leased.

The NAIC explains that collision coverage is optional and not required by law, but may be required by a lending institution or lessor. The same source also explains that auto insurance requirements can depend on the type of coverage and financial agreement.

I cannot confirm legal requirements for every country, state, or province. You should check your local insurance rules or speak with a licensed insurance professional.

Why Is Comprehensive Insurance Important?

Comprehensive insurance can help reduce financial loss from covered non-collision events. It may protect you from paying the full cost of theft, fire, flood, hail, vandalism, falling objects, or animal damage.

This coverage may also matter if your car is financed or leased because lenders often require protection for the vehicle until the loan or lease is paid off.

Pros and Cons of Comprehensive Insurance

Pros

- Covers many non-collision risks

- May protect against theft, fire, flood, hail, and vandalism

- May be required by lenders or leasing companies

- Can reduce large repair or replacement costs after covered events

Cons

- Adds to your auto insurance premium

- A deductible usually applies

- Does not cover every type of loss

- May not be cost-effective for older or low-value vehicles

How to Choose the Best Comprehensive Insurance Policy

Before buying comprehensive coverage, check:

- What risks are covered

- What exclusions apply

- Deductible options

- Coverage limits

- Glass coverage rules

- Claim process

- Insurer licensing

- Total premium cost

The NAIC consumer guide recommends checking whether the insurer is licensed and understanding coverage options before choosing auto insurance.

How to File a Comprehensive Insurance Claim

Claim procedures vary by insurer, so I cannot confirm one universal process. However, a typical process may include:

- Report the incident to your insurer.

- Take photos or videos of the damage.

- File a police report for theft or vandalism if required.

- Submit requested documents.

- Get a repair estimate if required.

- Pay the deductible if the claim is approved.

- Follow the insurer’s repair or settlement process.

Always follow the claim instructions in your policy or insurer portal.

Common Myths About Comprehensive Insurance

Comprehensive insurance covers everything

This is incorrect. Comprehensive insurance covers specific non-collision risks listed in the policy. It does not cover every type of loss.

Comprehensive insurance is the same as collision insurance

This is incorrect. Comprehensive insurance covers many non-collision losses, while collision insurance covers crash-related damage.

Comprehensive insurance is always legally required

This is incorrect. Comprehensive insurance is generally optional by law, but lenders or leasing companies may require it.

FAQs

What is comprehensive insurance in simple words?

Comprehensive insurance helps pay for covered damage to your car from events other than collision, such as theft, fire, flood, hail, vandalism, falling objects, and animal damage.

Does comprehensive insurance cover accidents?

It depends on the type of accident. Damage from hitting another car or object is usually covered by collision insurance. Damage from animal impact, falling objects, fire, theft, or hail may fall under comprehensive coverage.

Does comprehensive insurance cover theft?

Yes, theft is commonly included under comprehensive coverage, according to the Insurance Information Institute.

Does comprehensive insurance cover flood damage?

Flood damage is commonly listed as a comprehensive coverage risk by the NAIC. However, you should check your policy because coverage terms can vary.

Is comprehensive insurance the same as full coverage?

No. Full coverage is not one standard policy. It usually refers to a combination of liability, collision, and comprehensive coverage.

Is comprehensive insurance required for a financed car?

Lenders often require comprehensive and collision coverage for financed vehicles. The NAIC states that if you have an auto loan, your lender may require both.

Is comprehensive insurance worth it for an old car?

It depends on your car’s value, premium, deductible, and ability to pay for repairs yourself. If the cost of coverage is high compared with the vehicle’s value, it may not be cost-effective.

Conclusion

Comprehensive insurance helps protect your vehicle from many covered non-collision risks, including theft, fire, flood, hail, vandalism, falling objects, and animal damage. It is different from collision insurance and should not be confused with full coverage.

This coverage may be valuable if your vehicle is financed, leased, new, expensive, or exposed to risks such as theft, storms, floods, or wildlife. However, it may not be cost-effective for every old or low-value vehicle.

Before buying, compare policy terms, deductibles, exclusions, claim rules, and total premium cost. Always confirm coverage with a licensed insurance provider before making a decision.