Do I need full coverage on a financed car? Many car buyers ask this right after getting approved for a loan. Full coverage means your policy includes liability, collision, and comprehensive insurance. It protects other drivers, property, and your own vehicle against accidents, theft, or damage. For financed cars, it’s not just a smart choice — it’s often required by your lender. The lender still owns part of the car until the loan is paid off, so they want to protect their investment. For you, full coverage helps avoid large out-of-pocket costs if something happens to the car before the loan is settled.

About the author: This article is published by MoneyMentorDesk to explain common car-loan insurance requirements in plain language. We use lender terminology (lienholder/loss payee, deductible limits) and general insurance definitions (collision, comprehensive, ACV) to help readers understand what may be required on financed vehicles. This content is educational and not legal or financial advice.

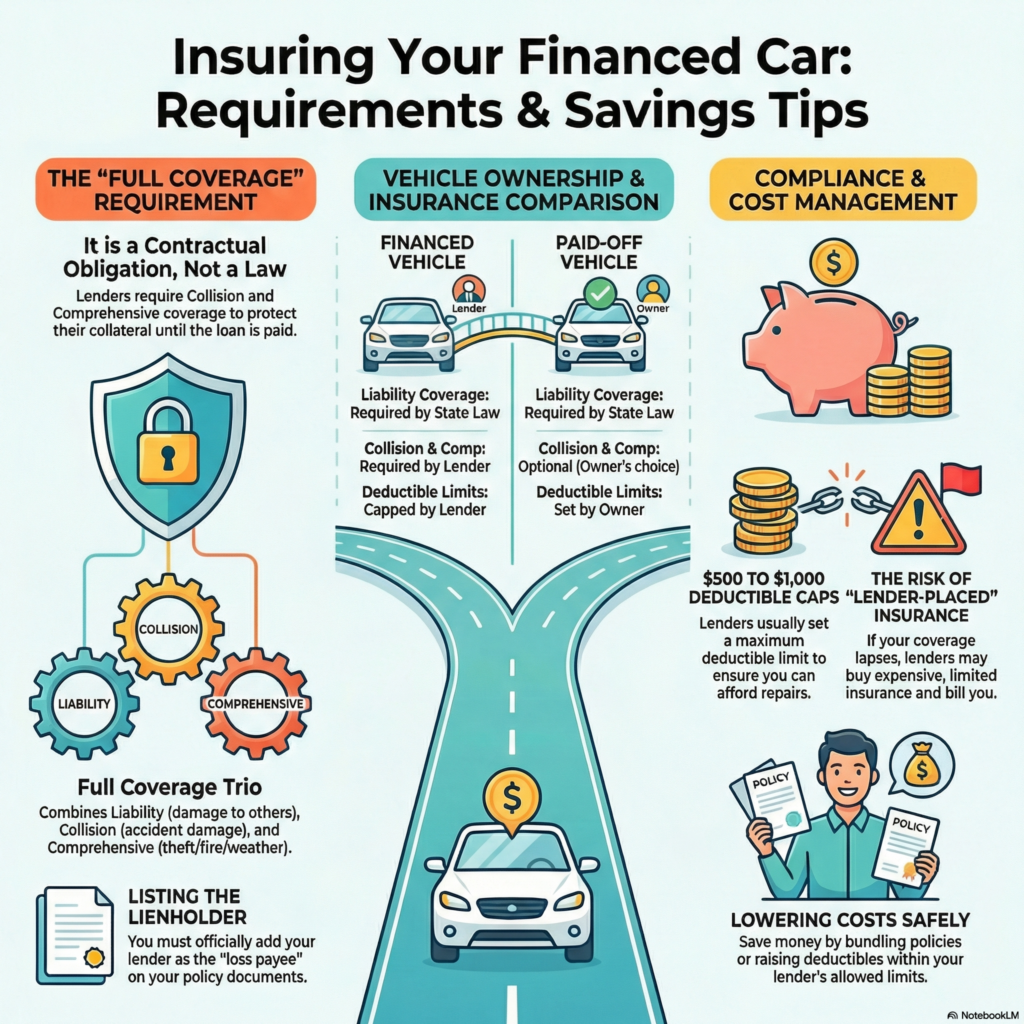

Quick Answer (Lender Rule vs State Law)

If your car is financed, your lender usually requires collision and comprehensive coverage until the loan is fully paid off. This requirement comes from your loan agreement, not state law.

State law typically only requires minimum liability insurance, but lenders add extra coverage rules to protect the vehicle they financed.

Understanding Full Coverage for a Financed Car

What Is Considered Full Coverage Insurance?

Full coverage insurance is not a single type of policy. It’s a combination of liability, collision, and comprehensive coverage. Liability covers damage or injury you cause to others. Collision covers damage to your own car in an accident, regardless of fault. Comprehensive covers non-accident events like theft, fire, vandalism, or weather damage. Together, these coverages can reduce financial risk for you and help meet common lender requirements while the loan is active.

Is “Full Coverage” a Real Insurance Policy?

“Full coverage” is not a single, official insurance policy. It’s an informal term commonly used to describe a combination of:

- Liability coverage

- Collision coverage

- Comprehensive coverage

Insurance companies sell these coverages separately within one policy. When lenders say they require “full coverage,” they usually mean collision and comprehensive must be included along with liability insurance.

Always review your policy documents to confirm exactly which coverages are included.

Minimum Full Coverage for Financed Car — What Lenders Require

The minimum full coverage for a financed car usually includes liability, collision, and comprehensive coverage. Some coverage requirements come from state law (such as UM/UIM in certain states), while lender requirements usually focus on collision, comprehensive, deductible limits, and listing the lienholder. These requirements are in your loan agreement. Lenders want to reduce the risk of financial loss if the vehicle is totaled or stolen, which is why they require coverage types designed to protect their collateral. Without adequate coverage, there may be a larger out-of-pocket risk after a major loss.

Legal Requirements vs Lender Requirements

State laws set minimum insurance requirements for all drivers, usually liability coverage only. Lender requirements are different. If your car is financed, your lender typically requires full coverage until the loan is paid off. This is a contract condition, not just a legal rule. Even if your state allows liability-only coverage, your lender can insist on more protection to secure their investment.

What Lenders Actually Check

When you finance a car, lenders typically verify the following:

- Active policy status (no lapse in coverage)

- Collision and comprehensive included

- Deductibles within allowed limits

- Lienholder listed correctly (also called “loss payee” or “additional interest”)

- Proof of insurance provided (insurance ID card or declarations page)

If coverage drops or doesn’t meet requirements, the lender may contact you and request updated proof.

Proof of Insurance: What Lenders Accept (And Where to Find It)

Most lenders accept:

- Declarations page: Shows coverages, deductibles, and lienholder listing.

- Insurance binder: Temporary proof for a new policy.

- Insurance ID card: Basic proof, but it may not show deductibles or lienholder details.

Where to find it: In your insurer’s app/website under “Documents” or “Policy.” Submit it through your lender portal or the method listed in your loan welcome packet.

How to Add Your Lienholder / Loss Payee (Step-by-Step)

Adding your lender to your policy is usually simple:

- Contact your insurance company (online account, app, or phone).

- Go to the section labeled “Additional Interest” or “Lienholder.”

- Enter your lender’s official name and mailing address (found in your loan documents).

- Confirm that the lender is listed on your declarations page.

- Send updated proof to your lender if required.

This ensures your lender is notified if coverage changes or if a total loss claim occurs.

Why You Need Full Coverage on a Financed Car

Do I Need Full Coverage Insurance on a Loaned Vehicle?

In many auto loans, lenders typically require full coverage until the loan is paid off. If your car is under a loan, the lender typically requires it. Full coverage protects both you and the lender from loss. If your car is damaged, stolen, or totaled, the insurance payout may help cover repair costs or the vehicle’s actual cash value, which can be applied toward your remaining loan balance, depending on policy terms. Actual Cash Value (ACV) refers to the car’s market value at the time of loss, after accounting for depreciation, mileage, and condition. Without adequate coverage, you may still owe money on the loan even if the vehicle is declared a total loss.

What Happens If You Don’t Have Full Coverage on a Financed Car?

If you reduce coverage below your lender’s requirements while the loan is active, you may be violating your loan agreement. The lender may arrange lender-placed insurance on your behalf. Lender-placed coverage can cost more than a standard policy you choose, and protections may differ—review the lender’s notice and policy summary if issued. You also risk paying the remaining loan balance out-of-pocket if the car is damaged or stolen. Depending on your loan agreement and state regulations, failure to maintain required coverage may lead to additional fees or loan enforcement actions.

Total Loss on a Financed Car: Who Gets Paid First?

If your financed vehicle is declared a total loss after an accident or theft, the insurance company typically pays the claim based on the car’s Actual Cash Value (ACV) at the time of loss.

Because the lender is listed as the lienholder (loss payee), the payment is usually issued:

- First to the lender (up to the remaining loan balance), and

- Any remaining amount (if applicable) goes to you.

If the insurance payout is less than what you still owe, you may remain responsible for the difference unless you have GAP coverage. Always review your policy terms and loan agreement for specific payout procedures.

How Depreciation Affects Insurance Payouts

Depreciation means your car loses value over time due to age, mileage, and wear. Because insurance payouts are usually based on Actual Cash Value (ACV), the amount you receive after a total loss may be lower than what you originally paid for the vehicle.

This is why some borrowers consider GAP coverage when the loan balance is higher than the vehicle’s current market value.

Typical Deductible Limits Lenders Require (And What to Do If Yours Is Higher)

Many lenders set a maximum deductible for collision and comprehensive coverage. While limits vary by lender, common caps are:

- $500 deductible

- $1,000 deductible

If your deductible is higher than allowed:

- Contact your insurer to adjust it within lender limits.

- Compare premium differences before making changes.

- Confirm the updated deductible appears on your declarations page.

Always check your loan agreement for the exact requirement.

What Is a Deductible Cap?

A deductible cap is the maximum deductible amount your lender allows for collision and comprehensive coverage while your loan is active.

For example, if your lender sets a $1,000 deductible cap:

- You can choose $500 or $1,000

- But you cannot choose $1,500 or $2,000

Lenders set deductible caps to reduce the risk that a high deductible would delay repairs or create financial strain after a claim. Always confirm your lender’s specific deductible limit in your loan agreement.

How to Lower Full Coverage Costs Without Losing Protection

Raise Deductibles to Reduce Premiums

Increasing your deductible — the amount you pay out of pocket before your insurance coverage kicks in — can significantly lower your monthly premiums. For example, increasing your deductible may lower your annual premium, although the exact savings depend on your insurer, vehicle, and driving profile. However, this strategy only works if you have enough savings set aside to cover the higher deductible in the event of a claim. It’s a balance between short-term savings and long-term financial readiness.

Bundle Policies for Discounts (Home/Renter + Auto)

Insurance companies often reward customers who hold multiple policies with them. By bundling your auto insurance with your home or renter’s insurance, you may receive a discount on your premiums, depending on the insurer and your eligibility. Not only does this simplify bill payments and account management, but it can also provide you with broader coverage options at a lower combined cost.

Maintain a Clean Driving Record

Your driving history plays one of the most significant roles in determining your premium. Avoiding accidents, traffic tickets, and claims can keep your rates low for years. Many insurers offer “safe driver” or “good driver” discounts, which may lower your premium, depending on the insurer’s discount structure and your driving history. If you have a blemish on your record, consider defensive driving courses — Some insurers may offer a discount after an approved course, but eligibility and savings vary by company and state.

Full Coverage vs Liability-Only After Payoff (Simple Decision Checklist)

Once your loan is fully paid, you are no longer contractually required to carry full coverage. At that point, consider:

- Is the car still valuable compared to repair costs?

- Could you afford to replace it out of pocket?

- How much are collision and comprehensive costing annually?

- What is your risk tolerance for damage or theft?

If the vehicle’s value is low and you can handle potential loss financially, some drivers choose liability-only. The right decision depends on your budget and comfort level.

If You Can’t Afford Full Coverage (Safe Options)

If full coverage feels expensive while your loan is active, consider these safer adjustments:

- Raise your deductible within lender limits

- Compare quotes from multiple insurers

- Ask about bundling discounts (auto + renters/home)

- Explore usage-based or low-mileage programs

- Review coverage limits to remove unnecessary add-ons

Avoid canceling required coverage without speaking to your lender first, as this could create issues with your loan agreement.

Step-by-Step: How to Get the Right Full Coverage Policy for a Financed Car

- Check your loan agreement for required coverage types, limits, and deductible caps.

- Compare quotes from at least three insurers using the same coverage levels.

- Choose deductibles that meet lender requirements and that you could afford in a claim.

- Add your lienholder/loss payee using your lender’s official name and address.

- Download proof of insurance (declarations page or insurance binder) and submit it if your lender requests it.

- Review your policy yearly and update lienholder info if you refinance.

Frequently Asked Questions (FAQ) About Full Coverage on a Financed Car

1. Do I need full coverage on a financed car by law or just by lender rules?

Full coverage is not required by state law, but most lenders make it a condition of your loan agreement. This ensures the vehicle — which serves as the lender’s collateral — helps reduce financial risk related to accidents, theft, and damage.

2. What is the minimum full coverage for a financed car?

Lenders typically require a policy that includes liability, collision, and comprehensive coverage. Some may also require GAP insurance or loan/lease payoff coverage. Coverage limits must meet or exceed the lender’s stated minimums, which can vary by lender and state.

3. What happens if I drop full coverage before the loan is paid off?

If you cancel or reduce your coverage below the lender’s requirements, the lender can purchase a policy on your behalf (known as force-placed insurance) and add the cost to your loan payment. This type of insurance is usually more expensive and offers less protection for you.

4. Can I switch to liability-only once my car is paid off?

Yes. Once your loan is paid in full, you can choose liability-only coverage if it meets your state’s legal requirements. However, you should evaluate your car’s value and your financial situation before dropping full coverage to ensure you’re not leaving yourself vulnerable to significant repair or replacement costs.

5. Does full coverage include GAP?

Usually no. “Full coverage” typically means liability + collision + comprehensive. GAP coverage is separate and may be offered by your insurer, lender, or dealer depending on availability.

Disclaimer

This article is for informational purposes only and does not constitute legal or financial advice. Always check your loan agreement and consult your lender or insurance provider for specific coverage requirements. Sources: State Department of Insurance consumer pages, insurer glossaries (collision, comprehensive, ACV), and lender documentation terminology for lienholder/loss payee and lender-placed insurance.