Golf carts are no longer limited to courses and private resorts. Street-legal Low-Speed Vehicles now operate in retirement communities, coastal towns, suburban neighborhoods, and rural properties across the United States. As demand has grown, so has the financing market.

In 2026, buyers have access to manufacturer 0% APR deals, specialty lenders, credit union loans, and in-house dealer programs — across a wider range of credit profiles than ever before. This guide covers current interest rates, how to qualify for the best offers, the legal difference between a golf cart and an LSV, and the steps to avoid overpaying. All rate data is sourced fromSheffield Financial, EZGO, Club Car, Yamaha, and Roadrunner Financial as of May 2026 — verify current offers directly with lenders before making a decision.

How do I finance one? The good news is that golf cart financing has expanded dramatically in 2026. Manufacturers are running aggressive 0% APR promotions. Specialty lenders have entered the market with competitive rates. Credit unions have quietly been offering some of the best terms available. And even buyers with less-than-perfect credit now have real options.

The bad news? Most buyers walk into a dealership, accept the first financing offer they see, and end up paying hundreds — sometimes thousands — more than necessary. Dealer-marked-up rates, misunderstood LSV classifications, and a lack of comparison shopping are the biggest culprits. This guide covers everything: current 2026 interest rates by credit tier, where to find 0% APR deals, how LSV rules affect your loan options, lender-by-lender breakdowns, monthly payment examples, and the exact steps to get the best deal available to you right now.

Golf Cart Financing at a Glance — What’s Changed in 2026

Before diving into rates and lenders, it helps to understand where the market stands today. Three things define golf cart financing in 2026:

- More competition among lenders. Sheffield Financial, Roadrunner Financial, and credit unions are all actively competing for golf cart buyers. That competition has pushed rates down and improved terms for qualified buyers.

- Aggressive manufacturer promotions. Club Car, EZGO, and Yamaha all run 0% APR campaigns through their authorized dealer networks — typically for 36 to 48 months. These are genuine 0% offers, not deferred interest schemes.

- Growing LSV complexity. As more buyers purchase street-legal LSVs instead of standard golf carts, lenders are drawing clearer lines about what qualifies for what type of loan. Understanding these distinctions can save you money.

What hasn’t changed: the market still heavily rewards buyers who do their homework. The difference between accepting a dealer’s first offer and shopping around can easily be 2 to 3 percentage points — which on a $15,000 cart over 60 months is roughly $1,200 to $2,400 in extra interest payments.

Current Golf Cart Interest Rates in 2026

Interest rates for golf cart financing in 2026 vary widely depending on your credit score, the type of lender you use, and whether the cart qualifies as an LSV. Here is a clear breakdown of what to expect:

By Credit Score Tier

| Credit Score | Typical APR Range | Best Available Rate | Notes |

| Excellent (750+) | 5.99% – 8.99% | 0% (promotional) | Qualifies for manufacturer 0% offers |

| Good (700–749) | 7.99% – 11.99% | 5.99% (credit union) | Most options available |

| Fair (650–699) | 12.99% – 17.99% | 10.99% | Specialty lenders needed |

| Poor (below 650) | 18.99% – 24.99%+ | 17.99% | In-house financing likely required |

| No Credit History | 15.99% – 22.99% | 14.99% | Cosigner can improve rate significantly |

By Lender Type

| Lender Type | Typical APR | Best For |

| Manufacturer Promotional (0% APR) | 0% – 4.99% | Buyers with excellent credit, 36–48 month terms |

| Credit Union | 5.99% – 9.99% | Members with good-to-excellent credit |

| Specialty Lender (Sheffield, Roadrunner) | 7.99% – 19.99% | Wide credit range, fast approval |

| Traditional Bank / Personal Loan | 9.99% – 24.99% | General buyers without dealer access |

| In-House Dealer Financing | 12.99% – 29.99% | Bad credit or no credit situations |

| Buy Now Pay Later (Affirm, Klarna) | 0% – 36% | Small purchases, accessories only |

The single most important takeaway from this table: the gap between the best and worst rates is enormous. A buyer with excellent credit who finds a 0% promotional offer versus a buyer with poor credit using in-house financing on the same $12,000 cart could see a difference of over $5,000 in total payment over the life of the loan.

The 0% APR Deals — What They Are and How to Get Them

Zero-percent financing on a golf cart sounds too good to be true. It is not — but it comes with conditions worth understanding.

Who Offers 0% APR in 2026?

The three major golf cart manufacturers all run promotional 0% financing through their dealer networks:

- EZGO: Currently offering 0% for 36 months, 2.99% for 48 months, and 4.99% for 60 months on qualifying new models, including the 2026 Liberty LSV. These offers are managed through Sheffield Financial.

- Club Car: Runs comparable 0% promotions, typically available seasonally. Spring and fall are historically the strongest promotional periods. Financed through Sheffield Financial as well.

- Yamaha: Offers 0% through select dealer partnerships. Availability varies by region and model year.

The Conditions That Matter

Before you get excited about 0% APR, here is what to watch for:

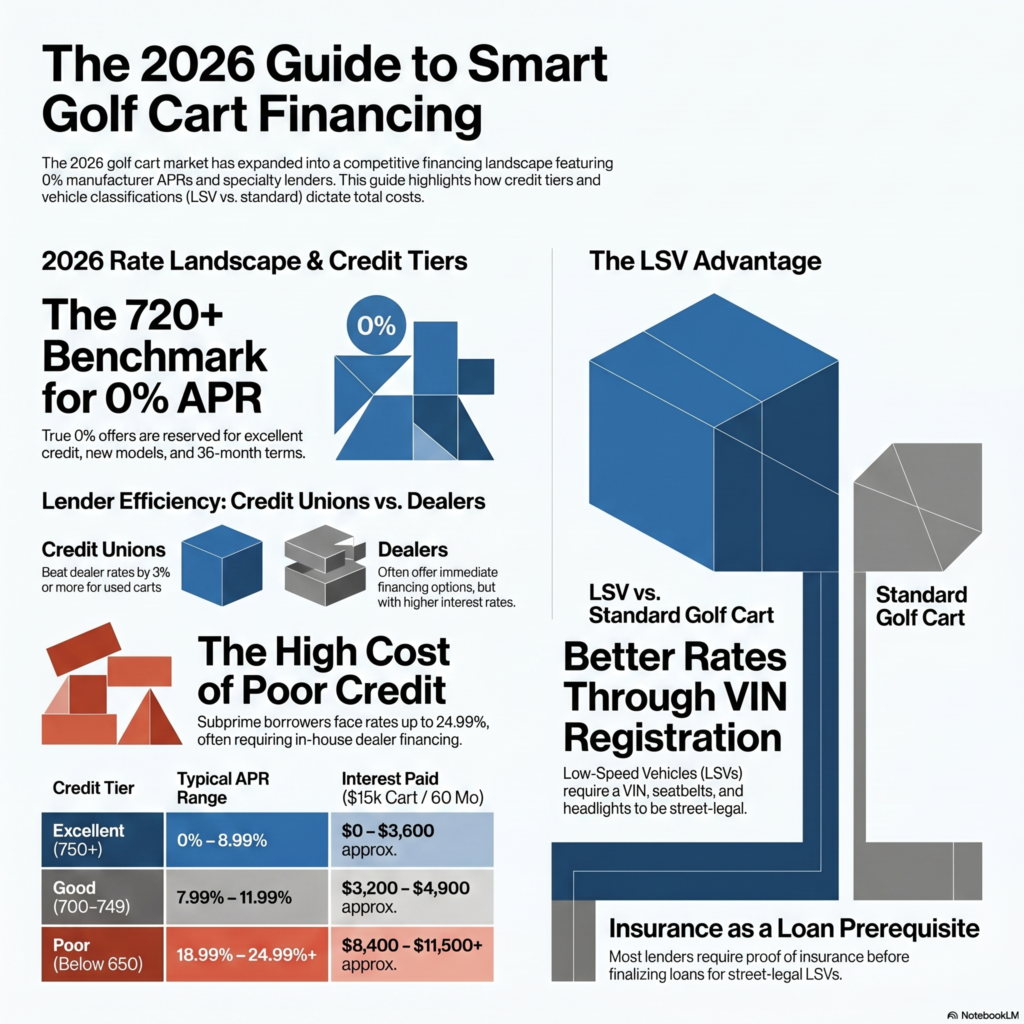

- Credit requirement. These offers are almost universally reserved for buyers with excellent credit — typically 720 or above. If your score is below that, you may be offered a higher rate after applying, despite the advertised 0%.

- Shorter terms. The true 0% offers are typically capped at 36 months. Longer terms come with a rate. On a $10,000 cart at 0% for 36 months, your payment is $278/month. Manageable — but not everyone can commit to that.

- New carts only. Used carts generally do not qualify for manufacturer promotional rates. You will be shopping in the open lending market for a used cart.

- Not all dealers participate. Call ahead to confirm the dealer is enrolled in the promotional program before making the trip.

| 💡 Pro Tip If you qualify for 0% APR, take it — even if you have cash. Keeping your cash invested while borrowing at zero interest is free leverage. Just make sure you can comfortably make the monthly payments. |

- You qualify with strong credit

- The cart and dealer participate

- The term fits your budget

- No hidden fees in the contract

- You can hold the payments comfortably

- Excellent credit (~720+)

- New cart purchase only

- Short 36–48 month term

- Selected models only

- Approved application

Lender-by-Lender Breakdown

Here is what you need to know about each major financing source in 2026:

Sheffield Financial

Sheffield is the dominant player in golf cart specialty lending. They power most of the 0% promotional offers you see advertised through Club Car, EZGO, and Evolution dealers. They also offer standard fixed-rate loans for buyers who do not qualify for promotional rates.

- Rates: Promotional 0% to 4.99%; standard rates from 7.99% to 19.99% depending on credit

- Terms: 24 to 72 months

- Best for: Buyers purchasing new carts from Sheffield partner dealers

- Watch out for: Standard rates can be higher than credit union alternatives; always compare before accepting

Verify current rates at sheffieldfinancial.com

Roadrunner Financial (Octane)

Roadrunner Financial, a subsidiary of Octane Lending, has built a strong reputation in the powersports and recreational vehicle lending space. They accept a wide range of credit profiles — including subprime buyers — and offer instant prequalification with no hard credit pull.

- Rates: Vary widely by credit; competitive for prime buyers, accessible for subprime

- Terms: 36 to 72 months

- Best for: Buyers who want to know their rate before visiting a dealership; fair-to-poor credit applicants

- Standout feature: Instant decision with no credit score impact; offer valid for 30 days

Credit Unions

This is the most overlooked financing source in the golf cart market — and often the best one for buyers with good credit. Credit unions offer personal loans and recreational vehicle loans at rates that often beat both dealer financing and specialty lenders, with no markup incentive.

- Rates: Typically 5.99% to 9.99% for qualified members

- Terms: Up to 60 months for most

- Best for: Existing members with strong credit history; buyers who want the lowest possible rate on a used cart

- Action step: Call your credit union before visiting any dealer. Get a preapproval letter. Use it as leverage.

In-House Dealer Financing

Many dealerships — particularly those selling refurbished or custom carts — offer their own financing programs. These are designed for buyers who cannot qualify elsewhere: bad credit, no credit, or unconventional financial situations.

- Rates: Typically 12.99% to 29.99%

- Terms: Some offer up to 84 months with same-as-cash periods of 6 to 12 months

- Best for: Buyers with FICO below 600 who have no other options

- Caution: Always read the full contract. Some same-as-cash offers retroactively charge full interest if the balance is not paid within the promotional window.

Monthly Payment Examples

Seeing real numbers makes the decision clearer. Here are monthly payment estimates for common cart prices across different loan terms and interest rates:

$8,000 Cart

| APR | 36 Months | 48 Months | 60 Months |

| 0% | $222/mo | $167/mo | $133/mo |

| 6.99% | $247/mo | $191/mo | $158/mo |

| 9.99% | $258/mo | $203/mo | $170/mo |

| 14.99% | $277/mo | $222/mo | $190/mo |

$15,000 Cart

| APR | 36 Months | 48 Months | 60 Months |

| 0% | $417/mo | $313/mo | $250/mo |

| 6.99% | $463/mo | $358/mo | $297/mo |

| 9.99% | $484/mo | $380/mo | $319/mo |

| 14.99% | $520/mo | $416/mo | $357/mo |

These figures exclude taxes, registration fees, and insurance. Always ask the dealer for an out-the-door price before calculating your financing.

| 📊 Key Insight On a $15,000 cart, the difference between a 0% rate and a 14.99% rate over 60 months is roughly $6,420 in total interest. That is real money — and it is exactly why shopping your rate before visiting a dealership is so important. |

LSV Rules — Why They Matter for Financing

· Some lenders may treat it as a vehicle loan with better rates

· Insurance is required in most states before loan is finalized

· Registration with your state DMV is typically required

· Stronger resale value helps as loan collateral

This is the section most golf cart financing articles skip — and it is one of the most practically important topics for buyers in 2026. Understanding the difference between a standard golf cart and a Low-Speed Vehicle (LSV) can directly affect your loan options, insurance requirements, and where you can legally drive.

What Is an LSV?

A Low-Speed Vehicle is a four-wheeled electric or gas-powered vehicle with a maximum speed of 20 to 25 mph. At the federal level, LSVs must comply with Federal Motor Vehicle Safety Standard 500 (FMVSS 500), which requires:

- Headlights, taillights, and turn signals

- Mirrors (rearview and side)

- Windshield

- Seatbelts for all occupants

- A Vehicle Identification Number (VIN)

- Reflectors

A standard golf cart — the kind you rent at a golf course — does not meet these requirements and is not legally an LSV. This distinction matters enormously for road legality and financing.

LSV vs. Golf Cart: The Key Differences

| Feature | Standard Golf Cart | LSV |

| Max Speed | Typically 12–15 mph | 20–25 mph |

| VIN Number | No | Yes |

| Street Legal | Only on private property | On roads ≤35 mph (varies by state) |

| Registration Required | No | Yes (most states) |

| Insurance Required | Often not required | Required in most states |

| Financing Options | Personal loan, dealer financing | Auto loan, personal loan, dealer financing |

| Resale Value | Lower | Higher |

How LSV Status Affects Your Loan

Here is something most buyers do not realize: because LSVs have a VIN and qualify as registered motor vehicles in most states, some lenders — particularly credit unions and banks — will treat them like auto loans rather than personal loans or recreational equipment loans. This matters because:

- Auto loans tend to have lower rates than personal loans for the same borrower. If your LSV qualifies, you could access better terms.

- Some specialty lenders restrict financing to LSVs only. They want the VIN and registration as collateral. A non-LSV golf cart may only qualify for an unsecured personal loan at a higher rate.

- Certain promotional offers (like EZGO’s Liberty LSV promotions) are LSV-specific. A standard cart purchase through the same dealer may not qualify for the headline deal.

State-by-State LSV Road Rules (Key States)

LSV legality on public roads is determined at the state level. Here is a quick reference for the most active golf cart markets:

| State | LSV Road Legal? | Max Road Speed Limit | Registration Required? | Insurance Required? |

| Florida | Yes | 35 mph | Yes | Yes |

| California | Yes | 35 mph | Yes | Yes |

| Arizona | Yes | 35 mph | Yes | Yes |

| Georgia | Yes | 35 mph | Yes | Yes |

| Texas | Yes | 35 mph | Yes | Yes |

| South Carolina | Yes | 35 mph | Yes | Recommended |

| Nevada | Yes | 25 mph | Yes | Yes |

| North Carolina | Yes | 35 mph | Yes | Yes |

Note: Rules vary by municipality even within states that allow LSVs. Some cities and counties have additional restrictions or permit requirements. Always verify with your local DMV before purchasing an LSV for street use.

| ⚠️ Important If you are planning to drive on public roads, always buy a VIN-equipped LSV — not a converted golf cart. Converted carts may look street-legal but fail to meet federal safety standards, creating liability, insurance, and financing complications. |

How to Get the Best Golf Cart Financing Deal in 2026

Here is the step-by-step playbook for any buyer looking to finance a golf cart this year:

Know Your Credit Score Before You Shop

Pull your credit report at AnnualCreditReport.com (free) and check your score through your bank or credit card provider. Know exactly where you stand before any lender does a hard pull. This prevents surprises and helps you target the right lenders from the start.

Get Preapproved Before Visiting a Dealer

Contact your credit union or bank and ask for a preapproval on a recreational vehicle or personal loan. Then use Roadrunner Financial’s online tool to get an instant rate offer. Walk into the dealership with competing offers already in hand. This single step gives you significant negotiating leverage.

Check Manufacturer Promotions Directly

Before settling on a lender, visit the official websites for EZGO, Club Car, and Yamaha to see current promotional offers. Cross-reference with the specific dealer you plan to visit to confirm they are enrolled in the promotion. Do not assume — ask explicitly.

Ask About the Out-the-Door Price, Not the Monthly Payment

Dealers prefer to negotiate on monthly payments because it obscures the total cost. Instead, negotiate the purchase price first, then apply financing. Calculate the total amount you will repay (monthly payment × number of months) to compare offers apples-to-apples.

For LSVs, Ask About Registration and Insurance Requirements

Before signing, confirm whether the cart qualifies as an LSV in your state, whether you need to register it with the DMV, and what insurance is required. Factor these ongoing costs into your total ownership budget. Some lenders will also require proof of insurance before finalizing an LSV loan.

Read the Fine Print on Promotional Offers

Zero-percent and same-as-cash offers can contain deferred interest clauses that retroactively charge all interest if the balance is not paid within the promotional window. Read every line of the financing agreement. Ask the dealer to explain what happens if you make a late payment or carry a balance past the promotional period.

Financing a Used Golf Cart

Used golf cart financing works differently from new cart financing, and buyers often find fewer options and higher rates. Here is what to expect:

- Manufacturer promotions do not apply. The 0% APR deals are exclusively for new carts. For a used cart, you are working with the open lending market.

- Age restrictions exist. Many specialty lenders — including Eglin Federal Credit Union and others — limit financing to carts that are three years old or newer. Older carts may require an unsecured personal loan, which typically carries a higher rate.

- Condition matters. Unlike cars, golf carts do not have standardized value guides in most lending systems. Lenders may rely on the asking price or a simple market check. Have a mechanic inspect the cart before purchase, and bring documentation of its condition to support your loan application.

- The math can still work. A two-year-old LSV at $9,000 with a 7.99% credit union loan over 48 months costs roughly $220/month and substantially less total interest than a new cart at a higher rate. Used is not always the worse financial decision.

Bad Credit Golf Cart Financing

A credit score below 650 limits your options but does not eliminate them. Here is what is realistically available in 2026 for buyers with challenged credit:

- Roadrunner Financial: One of the most accessible specialty lenders for subprime borrowers. They accept a wide credit range and provide instant rate offers without impacting your score.

- In-house dealer financing: Many golf cart dealers — particularly those selling refurbished or custom carts — offer programs for buyers with bad credit or no credit history. Rates will be high (often 18% to 29%), but down payments of 20 to 30% can improve terms significantly.

- Add a cosigner: A cosigner with good credit can dramatically improve both your approval odds and your rate. This is one of the most effective tools available to subprime borrowers.

- Save a larger down payment: Lenders view a larger down payment as reduced risk. Putting 25 to 30% down can open doors that are otherwise closed at lower credit scores.

- Buy Now Pay Later (for accessories only): Services like Affirm are available at some dealers for accessories and upgrades, not full cart purchases. Do not count on BNPL for a primary cart financing solution.

| 🔑 Reality Check If your credit score is below 600 and you have no cosigner or substantial down payment, expect to pay a premium. The financially sound approach may be to delay the purchase, spend 6 to 12 months improving your credit score, and then revisit financing at significantly better rates. |

Frequently Asked Questions

Can I finance a golf cart with bad credit?

Yes, though your options are more limited and rates will be higher. Roadrunner Financial, in-house dealer programs, and adding a cosigner are your best paths. Expect APRs in the 18% to 29% range without strong credit.

What credit score do I need to get 0% APR financing?

Most manufacturer 0% promotional offers require a minimum credit score of 720, though some lenders use 700 as the cutoff. Below that, you will likely receive a standard rate offer even at dealers advertising 0% APR.

Is a golf cart an LSV?

Not automatically. A golf cart only qualifies as an LSV if it meets federal FMVSS 500 safety standards — including lights, signals, mirrors, windshield, seatbelts, and a VIN. Many standard golf carts do not meet these requirements and are not legally classified as LSVs.

How long can you finance a golf cart?

Most lenders offer terms from 24 to 72 months. Some in-house dealer programs extend to 84 months. Shorter terms at 0% APR are available through manufacturer promotions. The optimal term depends on the rate: a 0% offer at 36 months is almost always better than a 7.99% offer at 60 months for the same cart.

Do I need insurance to finance a golf cart?

For an LSV that will be registered and driven on public roads, yes — most lenders require proof of insurance before finalizing the loan. For standard golf carts used on private property, insurance is not always required by lenders, though it is still recommended.

Is it better to pay cash or finance a golf cart?

If you can access 0% APR financing, paying cash offers no financial advantage and surrenders the opportunity to keep your money working elsewhere. If financing rates are above what your savings could conservatively earn, paying cash makes more sense. This is a personal calculation based on your alternatives.

Can I use a personal loan to buy a golf cart?

Yes. Personal loans are a common financing vehicle for golf carts, especially for used carts or non-LSV models that do not qualify for specialty lending programs. Rates tend to be higher than dedicated golf cart loans but lower than in-house dealer financing for buyers with good credit.

Conclusion

Golf cart financing in 2026 is more accessible and more competitive than at any point in the market’s history. Whether you are chasing a 0% APR deal on a new EZGO Liberty LSV or financing a used cart with fair credit through Roadrunner Financial, the deals are there — but only for buyers who take the time to understand their options.

The five things that matter most:

- Know your credit score before you walk into a dealership.

- Get preapproved elsewhere before accepting dealer financing.

- Understand whether the cart you want qualifies as an LSV — it affects your legal rights, insurance requirements, and loan options.

- Compare the total repayment cost, not just the monthly payment.

- Read every line of promotional financing offers before signing.

A golf cart is a purchase that should bring enjoyment, not financial regret. The difference between a smart financing decision and a hasty one in this market is measurable in thousands of dollars. Take the time. Do the homework. The right deal is out there.

Sources

Sheffield Financial — sheffieldfinancial.com

EZGO Official — ezgo.com

Club Car Official — clubcar.com

Roadrunner Financial — roadrunnerfinancial.com

NHTSA FMVSS 500 — nhtsa.gov

Disclaimer

The information in this article is for educational purposes only and does not constitute financial advice. Interest rates, promotional offers, and lender terms change frequently. Always verify current rates directly with lenders before making any financing decision. MoneyMentorDesk.com is not a lender and does not originate loans.

© 2026 MoneyMentorDesk.com — All rights reserved.