How Much Do Braces Cost Without Insurance?

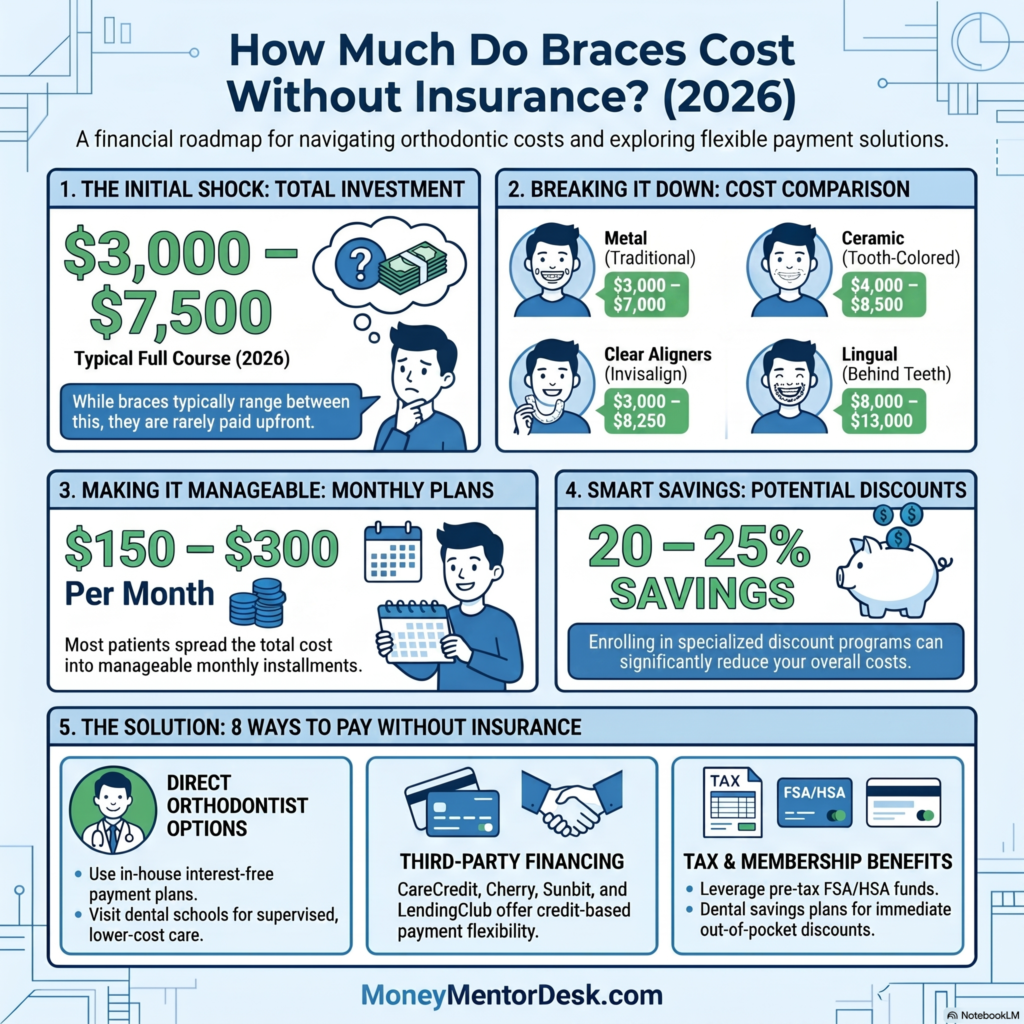

How much do braces cost without insurance? Typically, $3,000 to $7,500 in the United States, depending on the type you choose. Traditional metal braces are the most affordable, clear aligners and ceramic braces cost a little more, and lingual (behind-the-teeth) braces are the most expensive. The good news: you almost never have to pay it all at once. Most orthodontists offer in-house payment plans, and financing options like CareCredit, Cherry, or a tax-advantaged FSA or HSA can turn one big bill into small monthly payments. This guide breaks down how much braces cost without insurance in 2026 by braces type, what makes the price go up or down, and the cheapest ways to pay when you don’t have dental coverage.

Key takeaways

- Braces without insurance typically cost $3,000–$7,500; lingual braces can reach $13,000.

- Metal braces are the cheapest option; lingual braces are the most expensive.

- Where you live and how complex your case is can change the price by $1,000–$3,000 or more.

- You rarely pay upfront — in-house plans plus financing (CareCredit, Cherry, FSA/HSA) spread the cost monthly.

- No insurance doesn’t mean unaffordable: dental savings plans and dental schools can cut costs by roughly 20–25%.

How much do braces cost without insurance?

Without insurance, a full course of braces typically costs between $3,000 and $7,500, and most people pay around $5,000–$6,000 for traditional metal braces. The price covers your consultation, the braces themselves, regular adjustments, and usually a retainer at the end. Your final cost depends on four things: the type of braces, how complex your case is, how long you wear them, and where you live.

These ranges are consistent across major consumer-health sources, including GoodRx, Oral-B, and DentalPlans.com (figures current as of June 2026). Because orthodontics is priced per case, treat every number here as a typical range, not a quote — only an in-person exam gives you an exact price.

Braces cost by type (without insurance)

The type of braces is the biggest single factor in your price. Metal braces are the most affordable, ceramic braces cost a bit more for the tooth-colored look, clear aligners like Invisalign sit in a similar range, and lingual braces — fitted behind your teeth — are the most expensive because they’re harder to place. Here’s how the four main options compare without insurance:

| Type of braces | Typical cost without insurance | Best for |

| Metal (traditional) | $3,000 – $7,000 | The lowest price; works for all ages |

| Ceramic (tooth-colored) | $4,000 – $8,500 | A less visible look than metal |

| Clear aligners (e.g., Invisalign) | $3,000 – $8,250 | Removable and discreet |

| Lingual (behind the teeth) | $8,000 – $13,000 | Fully hidden; more complex cases |

Ranges compiled from GoodRx, Oral-B, and DentalPlans.com, June 2026. Prices vary by region and case.

Ceramic braces usually run about $1,000 more than metal because of the clear brackets. Clear aligners are often priced like ceramic braces, though very simple cases can cost less. Lingual braces are a specialty service, which is why they sit far above the rest.

What affects the price of braces?

Beyond the type of braces, your final cost comes down to how much work your smile needs and where you get it done. A simple alignment costs far less than a case that involves crowding, bite correction, or extra appliances. These are the main price drivers:

- Case complexity. Minor crowding is cheaper than a full bite correction.

- Treatment length. Longer treatment means more adjustment visits and a higher price.

- Type of braces. Metal is cheapest; lingual is priciest (see the table above).

- Where you live. Big-city orthodontists in places like Manhattan, San Francisco, or Los Angeles often charge $1,000–$3,000 more than offices in smaller towns, according to GoodRx.

- Extras. X-rays, retainers, and follow-up visits may be bundled in or billed separately — always ask what’s included.

Braces vs Invisalign — which is cheaper without insurance?

For most people, traditional metal braces are the cheapest option, while Invisalign costs about the same as ceramic braces. Metal braces typically run $3,000–$7,000 without insurance, and Invisalign and other clear aligners usually fall between $3,000 and $8,250. The right choice depends on your case: complex corrections often work better (and cost less) with braces, while mild-to-moderate alignment issues can be treated with clear aligners. Price difference aside, ask your orthodontist which option actually fits your teeth — the cheaper treatment isn’t a deal if it can’t fix the problem.

Is it cheaper to get braces without insurance?

Not usually. Paying cash sometimes earns a small discount, but dental insurance or a dental savings plan typically lowers your total cost more. Many dental insurance plans put a lifetime cap on orthodontic coverage (often a set dollar amount), so they reduce — rather than erase — the bill. If you have no coverage and don’t want to buy a full insurance plan, a dental savings plan can be the better move: these membership plans discount orthodontics by roughly 20–25%, per DentalPlans.com. The smartest approach is to compare the out-of-pocket cost three ways — cash price, dental insurance, and a savings plan — before you commit.

How to pay for braces without insurance

You don’t need to pay for braces all at once. Most orthodontic offices are set up to spread the cost over your treatment, and several outside financing options can help you start sooner. Here are seven ways to pay when you don’t have dental coverage:

- In-house orthodontist payment plans. Most practices let you split the cost into monthly payments — often interest-free over 12–36 months — after a down payment, as Smile Generation explains. This is usually the first option to ask about.

- Cherry. A buy-now-pay-later plan that uses a soft credit check, so checking your options won’t hurt your credit score. See our breakdown of whether Cherry runs a credit check and how it stacks up in Cherry vs CareCredit.

- CareCredit. A healthcare credit card you can use for braces and pay back over time, often with a promotional interest-free period if you qualify and pay it off in time. New to it? Read our guide on how to compare dental financing plans before you apply.

- Sunbit or LendingClub. Other third-party medical financing providers worth comparing for rate and approval odds.

- FSA or HSA. Pay with pre-tax dollars from a Flexible Spending Account or Health Savings Account, which lowers your effective cost depending on your tax bracket.

- Dental savings plans. Membership plans that discount orthodontics by about 20–25% — useful if you’ll skip insurance.

- Dental schools and nonprofit clinics. Supervised students and sliding-scale clinics offer reduced-cost orthodontic care if you’re flexible on timing.

Not sure which to pick? Start with our step-by-step guide to comparing dental financing plans so you weigh APR, fees, and total cost — not just the monthly payment.

How much are braces per month without insurance?

With a typical payment plan, braces often work out to roughly $150–$300 per month. Here’s a simple example: a $5,000 treatment split over 24 months at 0% interest through an in-house plan is about $208 a month ($5,000 ÷ 24). Many orthodontists will adjust the down payment and term to land on a monthly figure that fits your budget. Always confirm the interest rate and any fees, because a longer term with interest can quietly raise your total cost. (Figures are an illustrative example, not a quote.)

Frequently asked questions

How much do braces cost without insurance?

Without insurance, braces usually cost $3,000–$7,500 in the U.S. Metal braces are the most affordable (about $3,000–$7,000), while lingual braces cost the most ($8,000–$13,000). Your final price depends on the braces type, your case complexity, treatment length, and where you live.

How much are braces without insurance per month?

With a typical in-house payment plan, braces often work out to about $150–$300 per month. For example, a $5,000 treatment spread over 24 months at 0% interest is roughly $208 a month. Many orthodontists set the monthly amount and term to fit your budget.

What is the cheapest way to get braces without insurance?

The cheapest routes are traditional metal braces, a dental school clinic, or a dental savings plan that discounts orthodontics by about 20–25%. Paying in full sometimes earns a small cash discount, and using an FSA or HSA lowers your effective cost with pre-tax dollars.

Can you get braces with no money down?

Sometimes. Some orthodontists and financing providers like CareCredit or Cherry offer plans with little or no upfront payment, subject to approval. Terms vary by provider and credit profile, so ask your orthodontist which no-deposit plans they accept before you start treatment.

Does CareCredit cover braces?

CareCredit doesn’t “cover” braces like insurance does. It’s a healthcare credit card you use to pay for orthodontic treatment and then repay over time — often with a promotional interest-free period if you qualify and pay the balance off before it ends.

How much do braces cost for a child without insurance?

Children’s braces cost about the same as adults’ — typically $3,000–$7,000 for metal braces — though simpler cases can cost less. Treatment timing and complexity matter more than age. Some clinics and state programs (such as Medicaid in qualifying cases) offer reduced-cost care for kids.

About this guide

Author: Nimra Saleem, founder of MoneyMentorDesk.com, where she writes plain-English money guides researched from official and primary sources. Reviewed: Fact-checked against clinical and consumer-health sources (GoodRx, Oral-B, DentalPlans.com) and orthodontic practice pricing.

Sources: GoodRx — Cost of braces · Oral-B — How much do braces cost · DentalPlans.com — Braces cost without insurance · Smile Generation — Braces payment plans

Disclaimer:

This article is for general educational purposes only and is not financial, medical, or dental advice. Prices are researched ranges that vary by provider and region. Always confirm costs with a licensed orthodontist and consult a qualified professional before making financial decisions.