Leveraged finance is a type of borrowing used by companies that already have higher debt or lower credit ratings. Because lenders take on more risk, the loans or bonds usually offer higher interest rates and stronger investor protections.

In simple terms:

- Companies borrow large amounts of money even if their credit is below investment grade.

- The financing is commonly used for leveraged buyouts (LBOs), mergers and acquisitions, refinancing, or expansion projects.

- Deals are usually structured by investment banks and funded by institutional investors such as CLOs, hedge funds, and high-yield bond funds.

- Common instruments include Term Loan B, revolving credit facilities, high-yield bonds, and unitranche loans.

- Lenders analyze metrics like leverage (Debt/EBITDA) and interest coverage to assess risk.

Why it matters:

Leveraged finance allows companies and private equity sponsors to execute large transactions quickly while using debt to amplify potential returns.

What Is Leveraged Finance?

Leveraged finance is borrowing by below-investment-grade companies (credit ratings BB+/Ba1 or lower) or issuers with above-average leverage. Because risk is higher, investors demand higher coupons/yields (and often fees, call protection, and tighter documentation) than in investment-grade debt.

Typical use cases:

- LBOs and sponsor-backed M&A (including add-ons)

- Dividend recapitalizations (returning cash to owners)

- Refinancing or extending maturities of existing leveraged debt

- Growth/capex programs when equity is costly or dilution is undesirable

Appropriate when:

- Cash flows are resilient and coverage metrics (e.g., EBITDA/Interest) comfortably exceed covenants

- The business has a credible deleveraging path (organic growth, synergies, asset sales)

- Timing/certainty of funds matters (e.g., competitive M&A)

- The capital structure benefits from tax shields and flexible terms (loans/bonds mix)

Not appropriate when:

- Cash flows are volatile, early-stage, or cyclical with weak visibility

- Interest-rate or refinancing risk is high relative to cash generation

- Leverage required would push metrics to unsustainable levels (e.g., thin interest coverage, minimal liquidity)

- The company needs operational turnaround first (fix-the-business before adding debt)

How Leveraged Finance Works

A) Deal flow overview (mandate → close)

Mandate & commitment

Sponsor/issuer selects banks (sole/MLAs). Underwritten or best-efforts commitments; initial term sheet.

Due diligence & modeling

- Commercial, legal, accounting (QoE). Build LBO/cash-flow model; set leverage, structure, pricing, covenant framework.

Ratings

- Prelim (“shadow”) views from S&P/Moody’s/Fitch; target rating drives leverage, pricing, investor base.

Documentation

- Draft credit agreement/indenture, security/guarantees, intercreditor. Lender presentation/OM prepared; MFN, baskets, RP/debt capacity set.

Syndication / placement

- Loans (TLB/RCF): Launch price talk (SOFR + margin), OID, covenant package; bookbuild with CLOs/loan funds; flex if needed.

- Bonds (HY): Roadshow (144A/Reg S), finalize coupon, call protection; price and allocate.

- (If private/club) Direct lenders sign and fund without broad syndication.

Closing & funding

- Conditions precedent satisfied; collateral perfected; funds flow to acquire/refi/dividend/capex.

Post-close

- Ongoing reporting, covenant testing, amendments, potential add-ons or refinancings.

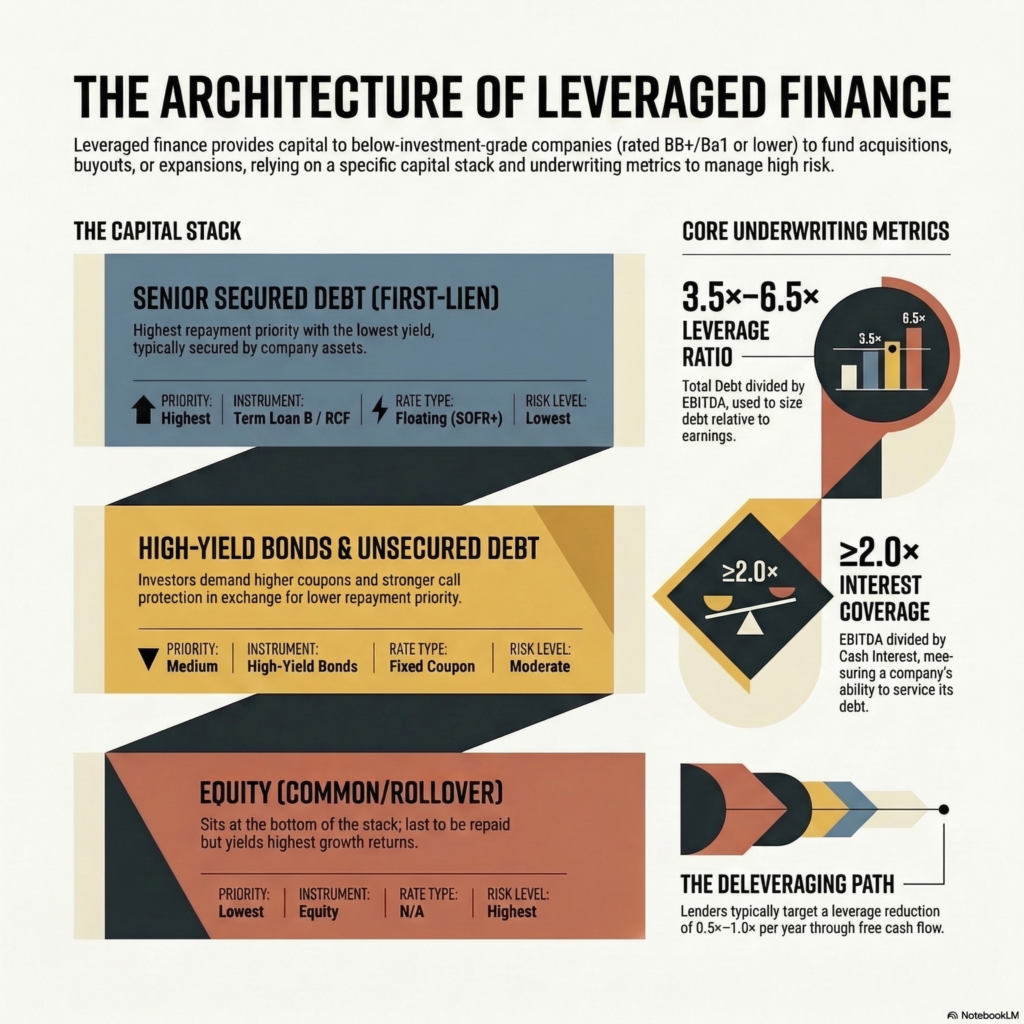

Capital stack (priority, covenants, pricing)

Highest priority/lowest yield → Lowest priority/highest return

In leveraged finance, the capital stack shows the order in which different investors are repaid if a company faces financial distress. The structure generally moves from lowest risk and lowest yield at the top to highest risk and highest return at the bottom.

From highest priority to lowest priority:

1. Senior Secured Debt (First-Lien Loans)

- Typically includes Term Loan B (TLB) and the Revolving Credit Facility (RCF).

- Secured by company assets and guarantees.

- Usually priced at SOFR + a margin, giving them the lowest interest rates in the capital stack.

2. Senior Unsecured or Second-Lien Debt

- May be unsecured or secured with a junior claim on collateral.

- Investors demand higher spreads and stronger call protection because repayment priority is lower.

3. Subordinated / Mezzanine / PIK / Preferred Capital

- Contractually junior to senior debt.

- Often includes PIK (payment-in-kind) interest or preferred equity features.

- Carries higher coupons to compensate for greater risk.

4. Equity (Common or Rollover Equity)

- Sits at the bottom of the capital structure.

- Equity investors are the last to be repaid in a default, but they benefit most if the company’s value grows.

Instruments in Leveraged Finance

Overview: Lev-fin uses a mix of loans and bonds tailored to speed, flexibility, and cost. Below are the core instruments, plus how rate type and security/guarantees typically work.

Term Loan B (TLB)

- What it is: Institutional, first-lien senior secured term loan; minimal amortization (often 1%/yr) with a large bullet at maturity.

- Pricing: Floating (SOFR + margin; may include a SOFR floor) with OID/upfront fees; soft-call protection common.

- Docs: Usually covenant-lite (incurrence covenants).

- Use: Core debt in LBOs/M&A; flexible for add-ons and repricings.

Revolving Credit Facility (RCF)

- What it is: Committed revolving line for working capital and letters of credit; often super-senior first-lien.

- Pricing: Floating; commitment/unused fees on undrawn amounts.

- Docs: Often includes a springing maintenance covenant when drawn.

- Use: Liquidity backstop and seasonal swings.

High-Yield (HY) Bonds

- What it is: Fixed-income securities, secured or unsecured, with incurrence covenants in an indenture.

- Pricing: Typically fixed-rate coupon with call schedule/make-whole.

- Use: “Permanent” capital, push out maturities, diversify investor base.

Unitranche (Direct Lending)

- What it is: Single facility that blends 1st/2nd-lien economics; privately negotiated with direct lenders.

- Pricing: Floating or fixed; higher cost than syndicated TLB but faster/greater certainty.

- Docs: Streamlined; bespoke covenants; non-call periods common.

- Use: Speed/certainty in mid-market or volatile markets; fewer parties.

Mezzanine / PIK / Preferred

- What it is: Subordinated (often unsecured) capital; may include PIK interest and/or warrants/preferred equity.

- Pricing: Highest coupons/IRR targets; tighter covenants.

- Use: Fill equity gap, preserve ownership, add leverage when senior capacity is maxed.

Bridge Loans

- What it is: Underwritten, short-term bank financing that backstops a takeout (HY bonds or TLB).

- Pricing: Step-up interest/ticking fees; strong incentives to refinance.

- Use: Certainty of funds at signing when markets are timing-sensitive.

Floating vs Fixed Rate (why it matters)

- Floating: TLB, RCF, many unitranches → benefit if base rates fall; expose borrower to rate risk (often hedged with swaps/caps).

- Fixed: HY bonds (and some unitranches) → stable interest cost; can be pricier upfront but reduce rate volatility.

Security/Collateral and Guarantees (what’s pledged)

- Secured loans (TLB/RCF): First-lien on material assets (PP&E, IP, equity pledges, sometimes receivables/inventory) with guarantees from restricted subsidiaries.

- Secured bonds: May share collateral on a pari or junior lien basis under an intercreditor agreement.

- Unsecured/mezz: No lien; rely on subordination and covenants for protection.

- RCF position: Often super-senior in the waterfall, especially if paired with an ABL; provides liquidity priority.

Key Metrics & Covenants

Core credit metrics (what lenders underwrite)

Leverage

- Gross/Net Debt ÷ EBITDA. Net = Debt – Cash.

- Use: Sizing debt; setting step-downs and covenant levels.

- Rule of thumb: Closing leverage often 3.5×–6.5× (sector-dependent). Target delever 0.5–1.0×/yr.

Interest coverage

- EBITDA ÷ Cash Interest. Sometimes EBIT/Interest or EBITDA–Capex ÷ Interest.

- Healthy: ≥2.0×; stronger deals sit higher.

Free Cash Flow (FCF)

- EBITDA – cash taxes – capex – cash interest – working-capital needs.

- Use: Deleveraging, add-ons, dividends. FCF conversion ≥60–70% is attractive.

DSCR / Fixed-charge coverage

- (EBITDA – Maintenance Capex) ÷ (Interest + Required Amortization + Leases + Dividends).

- More common in asset/real-estate heavy or project-like credits; lenders want >1.2×.

Liquidity & runway

- Cash + undrawn RCF (minus minimum cash) vs upcoming needs; stress for rate +200–300 bps and EBITDA –10–20%.

Refinancing profile

- Maturity wall timing, weighted-average life, mix of floating vs fixed; call protection on bonds.

Collateral/guarantor coverage

- % of EBITDA/assets pledged within the restricted/guarantor group; look for leakage to unrestricted subs.

Mini example: EBITDA 100; Net Debt 480 → 4.8× leverage; interest 43 → 2.3× coverage; capex 15 → FCF ~ (100–15–43–tax/working cap) to assess delever path.

Covenant architecture (how behavior is controlled)

Covenants are the rules in a loan or bond agreement that limit what a borrower can do (like taking more debt or paying dividends). They exist to protect lenders if performance weakens.

Two types:

- Maintenance covenants: tested regularly (often quarterly).

- Incurrence covenants: tested only when the company takes an action (like issuing new debt).

Why it matters: Covenants don’t stop risk — they define when lenders get protection.

| Type | When tested | Common in | Simple meaning |

| Maintenance | Every quarter | RCF / private credit | “You must stay healthy all the time” |

| Incurrence | Only when acting | HY bonds / cov-lite loans | “You must pass the test before doing X” |

Typical Use Cases

1) Leveraged Buyouts (LBOs)

- Goal: Acquire a company using a mix of debt and equity, then delever via cash flow and growth.

- Fit: Core stack is 1st-lien TLB + RCF, sometimes plus HY or 2nd-lien.

- Lenders focus on: Cash-flow durability, synergy plan, leverage/coverage at close and path to deleveraging.

2) Add-on Acquisitions

- Goal: Bolt smaller targets onto a platform company to scale revenue, margins, or capabilities.

- Fit: Incremental TLB capacity, accordion features, or unitranche upsizes for speed.

- Lenders focus on: Pro-forma leverage, integration risk, and covenant headroom (RPs/debt baskets).

3) Dividend Recapitalizations

- Goal: Return cash to owners without selling the business.

- Fit: TLB repricing/upsizing or secured HY; sometimes mezz/PIK to avoid over-gearing seniors.

- Lenders focus on: Post-dividend leverage/coverage and remaining liquidity; stricter scrutiny in cyclical sectors.

4) Refinancings & Maturity Management

- Goal: Lower interest cost, loosen terms, or push out a maturity wall.

- Fit: Exchange into HY, reprices of TLB, or bridge-to-bond when timing is tight.

- Lenders focus on: Refi risk, covenant improvements vs. leverage, fees/OID vs. savings.

5) Growth & Capex Programs

- Goal: Fund expansion (new plants, product launches, market entries) without heavy dilution.

- Fit: RCF for working capital swings, TLB for multi-year projects; hedging if rates are floating.

- Lenders focus on: ROI/IRR on projects, ramp timing, and cushion to absorb delays.

Note: Many deals blend instruments (e.g., TLB + HY or unitranche + mezz) to balance cost, speed, and flexibility.

Leveraged finance vs private credit

| Dimension | Leveraged Finance (Syndicated loans/bonds) | Private Credit (Direct lenders/BDCs) |

| Source of capital | Broad syndicated markets: CLOs, loan funds, HY bond funds; arranged by banks | Direct lenders/BDCs holding larger tickets themselves; club deals for size |

| Execution speed & certainty | Slower, market-dependent; subject to windows and flex/market pushback | Faster, high certainty; one-stop or small club, terms set upfront |

| Flex language | Common—arrangers can change margin/OID/tenor/covenants to clear the book | Rare—terms are bilaterally negotiated; pricing fixed once agreed |

| Pricing (rate type) | Loans: SOFR + margin (floating). Bonds: fixed-rate coupons with call schedules | Typically, SOFR + spread (floating). Some fixed; usually higher all-in than TLB |

| Leverage levels | Competitive in open markets; may be constrained when risk-off | Can stretch leverage on resilient credits due to hold size and bespoke risk views |

| Covenants | Loans often covenant-lite (incurrence only); bonds are incurrence-based | More maintenance covenants and tighter terms; bespoke reporting |

| Documentation complexity | More standardized (NY/LMA) but multi-party negotiations | Bespoke docs; faster negotiation with fewer parties |

| Call protection | Loans: soft-call (e.g., 101 for 6–12m). Bonds: hard call (NC1–2 with step-downs) | Often non-call 1–2 years with prepayment premiums |

| Hold sizes & scalability | Very large deals via broad syndication; individual holds smaller | Larger single-lender holds (e.g., 50–500m+); scale via clubs for bigger deals |

| Use-case fit | Lowest cost in receptive markets; desire for trading liquidity and broad investor base | Need speed/certainty, complexity, confidentiality, or markets are shut/volatile |

| When sponsors prefer it | Cost matters most; desire for covenant-lite and liquid takeout (future refi) | Need to sign fast, keep terms tight/confidential, or execute through volatility |

| Hybrid solutions | Bridge-to-bond, TLB + secured HY, 1st-/2nd-lien stacks | Unitranche + second lien, club unitranche, private 1st-lien plus mezz/PIK |

Leveraged finance example

Deal setup (simple LBO):

- Purchase price (EV): $900m (9.0× EBITDA = $100m)

- Sources: $400m 1st-lien TLB @ 8.5% (floating); $140m HY bond @ 9.5% (fixed); $360m equity

- Uses: $900m enterprise value (ignore cash/debt adjustments for clarity)

- Opening leverage: 5.4× (Net Debt $540m / EBITDA $100m)

- Opening interest expense: $47.3m (TLB $34.0m + HY $13.3m) → Coverage ≈ 2.1× (100 / 47.3)

Assumptions for Years 0–3: EBITDA grows ~6%/yr, capex $15m/yr, cash taxes $5m/yr, mandatory TLB amortization $4m/yr; any free cash flow (FCF) sweeps the TLB first. Rates held constant for simplicity.

Mini table (illustrative)

| Year | EBITDA ($m) | Interest ($m) | FCF* ($m) | Net Debt (End, $m) | Leverage (Net Debt / EBITDA) |

| 0 | 100.0 | 47.3 | 32.7 | 503.3 | 5.03× |

| 1 | 106.0 | 44.2 | 41.8 | 457.5 | 4.32× |

| 2 | 112.36 | 40.3 | 52.1 | 401.4 | 3.57× |

| 3 | 119.10 | 35.5 | 63.6 | 333.8 | 2.80× |

* FCF shown is after interest, taxes, and capex but before debt repayment; the model assumes all FCF + $4m mandatory amortization pay down the TLB each year. Coverage improves from ~2.1× → ~3.3× over Years 0–3, illustrating the deleveraging path as EBITDA grows and interest falls with lower debt.

Risks & Considerations

- Refinancing & maturity walls: Concentrated maturities can force refinancings in tough markets; manage tenor mix and open a refi window 12–24 months ahead.

- Rate risk (floaters): TLB/RCF at SOFR + margin expose cash flows to hikes; use swaps/caps and size leverage for +200–300 bps stress.

- Cyclicality & volatility: EBITDA drawdowns compress coverage and can trip covenants or block add-on capacity; build headroom in downside cases.

- Covenant headroom: Even “cov-lite” deals have incurrence tests and springing RCF maintenance; monitor leverage tests, RP/debt baskets, and MFN exposure.

- Liquidity in downturns: Preserve cash + undrawn RCF to fund seasonality, rate shocks, and working-capital swings; avoid over-reliance on revolver draws.

- Sponsor/borrower alignment: Healthy equity cushion and realistic value-creation plan (growth, margin, synergies) are critical to sustain the capital structure through cycles.

FAQs

What is leveraged finance in one sentence?

Debt financing for below-investment-grade or highly levered companies, priced with higher coupons and tighter docs to compensate for risk.

What does a leveraged finance investment banking team do?

They structure, underwrite, price, and syndicate loans/bonds; coordinate ratings, documentation, and investor bookbuilding to get the deal funded.

How does leveraged finance vs private credit differ?

Lev-fin taps syndicated markets (CLOs/HY funds) with more liquidity and potential covenant-lite terms; private credit is direct lending with faster execution, more bespoke maintenance covenants, and typically higher all-in cost.

What leverage and coverage levels are typical?

Closing leverage often ~3.5×–6.5× Net Debt/EBITDA (sector-dependent) with EBITDA/interest ≥ ~2.0×; underwriters want a path to delever ~0.5–1.0× per year.

How do rising rates affect floating-rate TLBs and RCFs?

Interest expense rises with SOFR + margin, pressuring coverage and FCF; borrowers often hedge with swaps/caps and size leverage to withstand +200–300 bps shocks.

Are covenants looser in bonds than in loans?

Generally, yes: high-yield bonds use incurrence covenants only; many TLBs are covenant-lite too, but RCFs can have a springing maintenance test when drawn.

How long does a lev-fin deal take from mandate to close?

Typically, 6–10 weeks in stable markets; 3–5 weeks for smaller add-ons or direct-lending/unitranche executions.

What is OID and why does it matter?

Original Issue Discount (OID) is a pricing tool that sells debt below par (e.g., 98.0) to boost investor yield without changing the headline margin/coupon—affects issuer proceeds and effective cost.

Is leveraged finance only for PE-backed companies? Can SMEs access it?

No. Corporates also use it for M&A, capex, or refis. Mid-market/SME borrowers often access private credit/unitranche rather than broadly syndicated markets.

Can you give a quick leveraged finance example?

A sponsor buys a $900m EV business with $540m debt (5.4×) and $360m equity; EBITDA grows and FCF pays down debt, improving leverage from ~5.4× to <3× over ~3 years (see the “Leveraged finance example” section above).

Disclaimer

This article is for educational purposes only and explains leveraged finance concepts using commonly available information from financial publications, corporate finance resources, and rating agency research such as Moody’s, S&P Global, and Fitch. Examples in this guide are simplified to help explain the concept and do not represent financial advice. Readers should consult qualified professionals before making financial or investment decisions. This article was written to explain complex corporate finance concepts in simple terms for students, learners, and readers interested in understanding leveraged finance.