What Is Motorcycle Courier Insurance?

Motorcycle courier insurance is coverage that explicitly allows you to carry food or parcels for pay, closing the “livery” or “public conveyance” gap that many personal motorcycle policies exclude. Personal policies are usually written for private use, so riders who deliver for hire should confirm in writing whether delivery activity is covered.

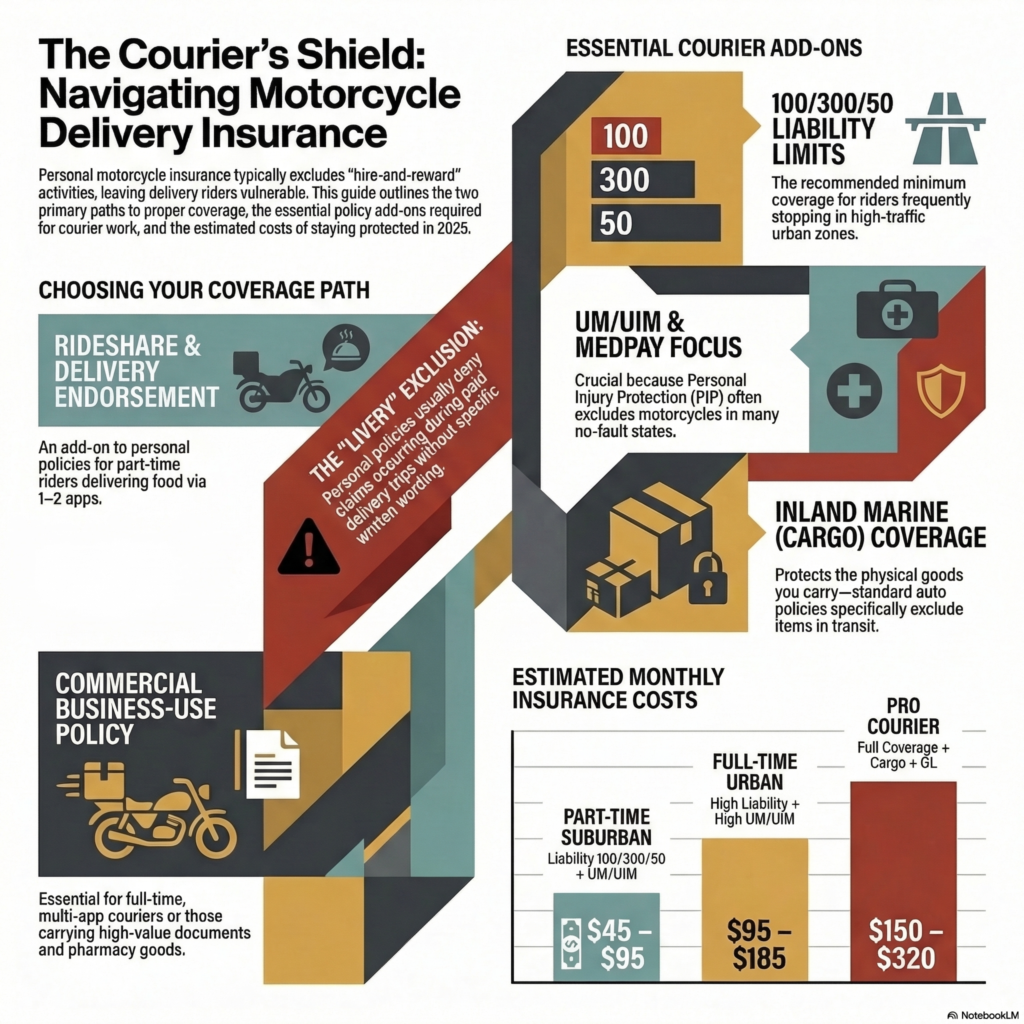

To stay properly insured, riders usually follow one of two paths. If available in your state, a rideshare or delivery endorsement may extend your existing motorcycle policy to cover delivery use. If your carrier does not offer that option, or if you deliver frequently, work across multiple apps, or carry higher-value goods, a business-use or commercial motorcycle policy may be the better fit.

Why personal policies fall short?

Motorcycle courier insurance is a policy or endorsement that explicitly permits paid delivery (hire-and-reward) on a motorcycle—removing the “livery/business-use” exclusion found in most personal policies.

Why personal policies fall short (and when they might work):

Most riders ask, “Does personal motorcycle insurance cover delivery?” —usually not during paid trips. Personal policies are priced for private use; delivery adds high-frequency stops, night riding, and tight timelines. If your carrier offers a rideshare/delivery endorsement for motorcycles, it can extend your personal policy to cover app phases. If not, you’ll need business use on a motorcycle policy (commercial form) so claims aren’t denied mid-delivery.

Endorsement vs. Commercial/Business Use (quick guide)

| Option | Best for | Coverage Phases | Paperwork & Proof | Pro Tips |

| Rideshare/Delivery Endorsement | Part-time riders, 1–2 apps, lower cargo value | Often “available/online” + “active delivery” (varies by carrier) | Keep the endorsement form and ID cards handy | Get written confirmation that “public/livery conveyance” is covered for motorcycles, not just cars |

| Commercial/Business-Use Motorcycle Policy | Full-time/multi-app riders, higher exposure, contracts needing certificates | Customizable; can pair with cargo/inland marine & GL | Request a Certificate of Insurance; list clients as additional insured only if required | Ask about accessory/gear limits and downtime options (roadside, rental) |

Mini checklist before you choose (“delivery rider insurance USA” ready)

- App(s) used: Uber Eats, DoorDash, Grubhub—do they require proof beyond your ID card?

- Hours & miles: Weekend side gig (endorsement may suffice) vs daily courier (commercial makes sense).

- Cargo value: Food only vs pharmacy/legal docs—consider cargo/inland marine add-ons.

- State rules: Minimum liability limits; no-fault quirks (PIP often excludes bikes); UM/UIM availability.

- Vehicle class: Motorcycle vs. moped/scooter—licensing/registration changes coverage.

- Documentation: Save in-app trip logs, photos of incidents, and your policy’s delivery wording for quick claims.

Essential Coverages for Motorcycle Delivery Insurance

Liability (BI/PD): minimums vs recommended limits

State minimum liability limits are a legal floor — not a financial safety net. A single serious crash during a delivery can exceed them easily. If you ride frequently, work in dense urban traffic, or depend on your bike for income, consider at least 100/300/50 liability coverage. Match your UM/UIM limits to your liability limit. This combination protects you whether the other driver is at fault or uninsured — which is common in high-traffic delivery zones.

UM/UIM for riders (why it matters)

Uninsured/Underinsured Motorist protects you if the other driver has little or no insurance—a common pain point for riders. It can cover your medical bills, lost wages, and sometimes pain and suffering.

Courier twist: riders spend more time exposed at intersections and curbside pickup zones. Many riders may want to consider strong UM/UIM limits because uninsured or underinsured drivers can create a major financial gap after a crash.

Medical Payments vs PIP (state-dependent caveats)

MedPay is a simple, no-fault medical add-on with small limits; Personal Injury Protection (PIP) is broader, but, in many no-fault states, PIP excludes or limits motorcycles.

Action step: Ask your agent two explicit questions:

- “Is PIP available for motorcycles in my state?”

- “If not, what MedPay limits do you offer, and does it stack with health insurance?”

Comprehensive & Collision (bike, accessories, gear)

These services fix or replace your bike in the event of crashes, theft, fire, or weather damage. For a full breakdown of what comprehensive insurance actually covers, including when it is worth adding to your policy, see our dedicated guide.

Couriers often add:

- Custom Parts & Equipment (CPE): bars, racks, windscreens. Specify values; keep receipts/photos.

- Riding gear coverage: helmet, jacket, gloves—sometimes a separate add-on or sub-limit.

Pro tip: Confirm whether installed accessories are covered automatically up to a sub-limit (e.g., $1–3k) and add CPE if you exceed it.

Cargo/Goods-in-Transit (“delivery insurance for motorcycles”)

Auto policies usually exclude cargo you’re carrying. If a drink spills, a hot bag is stolen, or a pharmacy package goes missing, you’ll want inland marine / goods-in-transit coverage.

What to ask for includes the per-occurrence limit (e.g., $5k+), per-item sub-limits, coverage for theft from an unattended but locked top box, and any exclusions related to temperature for hot or cold items. If you ever courier documents or higher-value items, increase limits accordingly.

General Liability (off-bike incidents)

If you knock over a lobby sculpture while waiting for an order—or your backpack scratches a counter—that’s not a motor vehicle claim. General Liability (GL) covers slip-and-chip moments off the bike.

Who needs it: full-timers, riders with direct business clients, or anyone asked for a Certificate of Insurance. (GL can sit inside a micro-BOP or as a standalone policy.)

Helpful add-ons: roadside, rental, legal, safety-course discounts

- Roadside/Recovery: fuel, towing, dead battery—worth it if you ride long hours.

- Rental reimbursement/downtime: rarer for bikes, but some carriers offer it—ask.

- Legal expense/traffic defense: helpful if your city is citation-prone.

- Safety course & device discounts: MSF completion, dashcams, trackers, or app-based safety programs can lower premiums.

To establish a documentation habit, save receipts, accessory photos, and a simple gear inventory on your phone; this will help claims move faster when the values are clear.

What the Apps Cover (and What They Don’t)

Delivery-platform coverage is usually limited and phase-based. For example, DoorDash says it provides third-party auto liability insurance during the “Delivery Available” and “Delivery Service” periods, while Uber states that occupational accident insurance covers injuries to drivers and delivery people and that separate third-party liability coverage applies across the US.

Phases at a glance

| App Phase | Your Status in the App | Typical Auto Liability from App | Injury to You | Notes |

| Offline | App closed | None | None from app | This is your personal/commercial policy only. |

| Available/Online | Logged in, waiting for an order | Often low or none; varies by app/state | Sometimes Occupational Accident not active yet | In the gray area, your own policy must address any gaps. |

| On-Delivery | Accepted order → drop-off complete | The app may provide third-party liability (limits vary) | Many apps include Occupational Accident (OAI) | Coverage usually ends once you mark the delivery complete. Document time stamps. |

Occupational Accident vs Auto Liability—know the difference

- Auto Liability (third-party): pays others if you cause a crash while on an active delivery. It does not repair your bike or replace the customer’s items.

- DoorDash and Uber both describe occupational accident insurance as a benefit that can help cover medical expenses, disability payments, and death benefits after covered accidents, but it is different from third-party liability coverage.

Why platform coverage isn’t a substitute

- Phase gaps: If you’re merely “online” or between orders, app liability may be minimal or zero.

- First vs excess: Even when app liability applies, your policy may still be primary or required by the app’s terms.

- Your bike & cargo:App policies typically won’t cover your motorcycle repairs (that’s collision) or the items you carry (that’s cargo/inland marine).

- State variance refers to the limits and triggers that can change from state to state and may update without any notice. You need a policy that always permits delivery use.

Workflow that protects you:

- Keep your own delivery-permitted policy active (endorsement or business use) + UM/UIM.

- Add cargo/inland marine if you carry anything you can’t afford to replace.

- Screenshot the app’s status screen when a trip starts/ends and keep order IDs—that time-stamp trail smooths claims.

- After any incident, make two calls: notify your insurer and start the app’s incident report to avoid finger-pointing over phases.

State Requirements & 2025 Updates for Motorcycle Courier Insurance (US)

Every state sets its own liability floor for motorcycles. Your policy must at least meet your state minimum motorcycle insurance (2025) limits to be road-legal—and courier work (hire-and-reward) doesn’t change that baseline; it just raises the wisdom of buying more than the minimum.

What changed in 2025 (headline example)

According to the California DMV, California’s minimum liability insurance limits are now $30,000 for injury or death to one person, $60,000 for injury or death to more than one person, and $15,000 for property damage.

Couriers should pay attention because state minimums are intended for everyday drivers, not for riders who frequently stop in traffic. For practical protection (and to satisfy many clients/platform checks), Many riders may consider limits above the legal minimum, especially if they ride in dense traffic or rely on the bike for income.

No-fault states & PIP: the motorcycle catches

In no-fault systems, Personal Injury Protection (PIP) pays medical bills regardless of fault—but motorcycles are often excluded or treated differently:

- According to the Florida Highway Safety and Motor Vehicles, proof of PIP and property damage liability is required before registering a vehicle with at least four wheels in Florida, which is why motorcycle riders should not assume standard Florida PIP protection applies to them.

- Massachusetts motorcycle insurance regulations state that insurers are not required to provide Personal Injury Protection (PIP) for owners, operators, or guests injured while operating or riding on a motorcycle, although pedestrians struck by motorcycles may still access PIP.

Cost: What Motorcycle Courier Insurance (US) Typically Costs

There’s no single price tag because courier risk swings with where, when, and how you ride. Think in bands.

What moves your premium (biggest to smallest for most riders):

- Location & garaging: dense, high-theft ZIPs and street parking cost more than suburban garages.

- Annual mileage & hours: late nights and rush hour add exposure; part-time weekends are cheaper than daily multi-app runs.

- Record & age: recent at-fault crashes, speeding, or license points will be priced in for 3–5 years.

- Bike CC & value: larger engines and expensive models raise comprehensive/collision.

- Coverage limits & deductibles: higher liability/UM and low deductibles raise price; reverse to save.

- Cargo/GL add-ons: Inland marine (goods) and general liability add cost—but protect your business.

- Discount signals: MSF/course completion, anti-theft, tracking, pay-in-full, bundling with renter’s/home.

Sample quote ranges (indicative only, not a promise)

| Rider profile | Core coverage (delivery permitted) | Typical monthly range* |

| Part-time suburban (few evenings/week, 300–500 mi/mo, mid-CC bike) | Liability 100/300/50 + UM/UIM; comp/coll with $500–$1k deductibles | $45–$95 |

| Full-time urban (multi-app, 1k+ mi/mo, high-traffic ZIP) | Same as above, plus higher UM/UIM; consider higher liability (250/500) | $95–$185 |

| Pro courier w/ cargo (contracts, pharmacy/docs) | Above + cargo/inland marine ($5k–$25k) + GL (e.g., $1M) | $150–$320 |

| Budget seeker (older bike, liability-only, delivery endorsement) | Liability 50/100/50 or 100/300/50; no comp/coll | $28–$65 |

* Ranges are broad US estimates. Your state, bike, record, and chosen limits can place you outside these bands.

Tactics to reach the “cheapest options” without underinsuring:

- Right-size deductibles: move comp/coll deductibles to $750–$1,000 if you can self-fund small repairs.

- Match UM/UIM to liability, then trim elsewhere: Riders need injury protection more than fancy add-ons.

- Prove the risk: garage photos, lock/tracker receipts, and MSF card—underwriters love documentation.

- Consolidate: bundle with renter’s/home; set autopay/pay-in-full; ask for “advanced riding/safety” discounts.

- Use mileage honesty to your advantage: if you truly ride part-time, keep a simple mileage log.

How to Get Covered (Step-by-Step)

1) Decide: Endorsement vs Business Use

- Endorsement path (if offered for motorcycles in your state): best for part-time riders on 1–2 apps, food-only cargo, and modest annual miles.

- Business-use/Commercial policy: better for full-time or multi-app riders, contracts that demand certificates, or higher-value cargo.

- Non-negotiable: get written wording that paid delivery (public/livery conveyance) on a motorcycle is covered across phases (waiting + on-delivery).

2) Commercial Motorcycle Insurance for Delivery Drivers

Choose this when:

- You ride daily, cross city lines, or do late nights.

- You need a Certificate of Insurance (COI) for building/property managers or business clients.

- You carry higher-value items or want the cleanest claims handling for business use.

- Ask for liability 100/300/50+, UM/UIM matched, MedPay where available, and comp/coll if the bike is critical to income. Confirm accessories/CPE limits for racks, mounts, and top boxes.

3) Add Cargo/Inland Marine & General Liability

- Cargo/Inland Marine (goods-in-transit): protects items you carry; set per-occurrence and per-item limits (e.g., $10k / $1k). Ask about theft from the locked top box and temperature exclusions for hot/cold food.

- General Liability (GL): covers off-bike mishaps (lobby scratches, spills). Some clients require $1M GL and a COI; only list “additional insured” if contractually required.

4) Compare Quotes & Prepare Proof

- Quote smarter: share mileage, riding hours, garaging address, MSF certificate, anti-theft evidence, and the apps you use.

- If you are also financing the motorcycle itself, our guide on how to compare financing options before committing can help you avoid overpaying on both the bike and the insurance.

- Ask for documents up front:

- Policy excerpt showing delivery is covered for motorcycles.

- ID cards and, if needed, COI with the correct certificate holder.

- Local backup plan: find one nearby independent broker (“delivery insurance near me”) who can issue same-day COIs if a building asks before pickup.

Scooters, Mopeds & E-Bikes: Beyond Delivery Insurance for Motorcycles

Small wheels, different rules. Don’t assume motorcycle terms apply.

- Definitions vary by state: a 49–50 cc moped might require a motorcycle endorsement in one state and not in another; speeds/engine size/power determine classification.

- Insurance form differences:

- Scooters/mopeds often still need motorcycle-type liability; confirm delivery use is permitted.

- Separate bike or e-bike coverage may be worth checking because insurers note that homeowners or renters’ policies may have low limits or may not fully cover bike or e-bike damage and liability exposures.

- Riders of street-legal Low-Speed Vehicles should also review our guide to Low-Speed Vehicle financing and insurance requirements, which covers how LSV classification affects both loan options and coverage obligations.

- Practical cover stack for e-bikes: GL for off-bike incidents + a specialty commercial e-bike or micro-mobility policy (some include third-party liability and limited physical damage).

- Cargo & theft: inland marine works here, too—ask for coverage of locked-to-object theft and in-transit protection.

- Compliance basics: licensing/registration/helmet rules still apply; building managers may ask for COIs even if your state doesn’t require insurance.

Claims: Who Pays First in a Delivery Accident?

The order of coverage depends on the phase and policy wording—but you can control the paper trail.

Typical order (simplified):

- Your policy (endorsement or business-use) often responds first—especially when the app provides excess liability only.

- App auto liability may step in during on-delivery (definitions vary).

- The other party’s insurance (if they’re at fault).

- Your UM/UIM if the other driver is uninsured/underinsured.

- Your comp/coll for your bike; cargo for customer items; GL for off-bike property damage.

- Occupational Accident (OAI) for your injury benefits (medical/disability) if the app includes it.

Documentation checklist for Motorcycle Courier Insurance

- Timestamped screenshots of app status (accepted order, pickup, drop-off).

- Order ID and restaurant/customer location.

- Photos/videos (dashcam helps), road conditions, and vehicle positions.

- Police report number and witness contacts.

- Medical records (even for minor injuries—motorcycle injuries can evolve).

- Notify both your insurer and the app the same day; keep reference numbers.

Pro tip: in write-ups, use the phrase “on an active delivery at [time]” and attach the status screenshots—this reduces back-and-forth over phases.

Common Mistakes to Avoid with Motorcycle Delivery Insurance

- Relying solely on app coverage: platform liability is phase-limited and rarely repairs your bike or covers your cargo.

- Assuming cargo is included: auto policies typically exclude items you transport; buy inland marine.

- Skipping UM/UIM: riders are exposed; match UM/UIM to your liability limits.

- Not disclosing business use: a livery exclusion can sink a claim—get the wording in writing.

- Underinsuring accessories/gear: racks, top boxes, and heated grips—raise CPE limits if needed.

- Wrong vehicle class: misclassifying a moped/e-bike can void coverage and tickets.

- Paperwork lag: no COI on hand when a building asks = lost time. Keep digital ID/COI files ready.

How this article was prepared

This article was researched using publicly available information from official websites, lender or insurer materials, and general consumer education sources. It is for informational purposes only.

About the Author

Nimra Saleem is the founder of MoneyMentorDesk, where she writes educational content on personal finance using independent research and publicly available information.

Editorial note

This content is not financial, legal, or insurance advice. Readers should confirm details with the relevant provider or official source.

Sources used for this article

- California DMV insurance requirements

- California Department of Insurance automobile coverage limits

- Florida Highway Safety and Motor Vehicles insurance requirements

- Massachusetts Division of Insurance motorcycle insurance regulations

- DoorDash help pages on auto insurance and occupational accident coverage

- Uber help pages on occupational accident and third-party liability coverage

- insurer guidance on courier, commercial, motorcycle, and e-bike coverage

FAQs: Motorcycle Courier Insurance

Does personal motorcycle insurance cover delivery work?

Usually no. Most personal policies exclude “public or livery conveyance,” which is exactly what paid delivery is. To stay covered, you need either a rideshare/delivery endorsement that explicitly includes motorcycles or a policy written for business use. Get the exact wording in writing from your insurer; it’s the simplest way to avoid claim denials later.

Do I need cargo insurance for food delivery?

Yes, if you want the items, you carry them protected. Auto liability covers other people and property—not customers’ goods. Ask for inland marine or “goods-in-transit” coverage with sensible per-occurrence and per-item limits. Confirm theft from a locked top box, misdelivery, and any temperature exclusions for hot or cold food. Adjust limits upward for pharmacy or document runs.

Are motorcycles eligible for rideshare/delivery endorsements?

Sometimes. Availability is carrier- and state-specific, and many endorsements were designed for cars first. If your insurer offers one, confirm in writing that it names motorcycles and covers both “available/online” and “on-delivery” phases. If no endorsement exists—or you ride full time—choose a business-use (commercial) motorcycle policy and add cargo and general liability as needed.

What are my state’s 2025 minimums?

Each state sets its own minimum liability limits for motorcycles, and some updated them for 2025. Treat those as a legal floor, not a safety net—courier exposure warrants higher limits like 100/300/50 or more. For precision, check your DMV/insurance department.

Is PIP available for motorcycles in my state?

In many no-fault states, Personal Injury Protection (PIP) excludes or restricts motorcycles. Don’t assume you have injury benefits. Ask your agent whether PIP applies to bikes where you live; if not, consider Medical Payments (MedPay) and strong Uninsured/Underinsured Motorist (UM/UIM) limits. Keep health insurance current, and verify how benefits coordinate after an accident.

Can I deliver on a scooter/moped—what insurance applies?

It depends on classification. Some states treat 49–50 cc mopeds as motorcycles for licensing and insurance; others don’t. E-bikes used for business are rarely covered by homeowners/renters’ policies. Make sure your policy explicitly permits business/delivery use for your vehicle class, add cargo for items carried, and keep Certificates of Insurance handy if buildings or clients request them.

Who pays first in a crash during a delivery?

Your policy (endorsement or business-use) often responds first; app auto liability may apply during an active delivery; the other driver’s insurance pays if they’re at fault. Your UM/UIM fills gaps, comp/collision fixes your bike, cargo covers goods, and occupational accident—if provided—addresses your medical/disability. Timestamp app screenshots to prove phase.

How much does motorcycle delivery insurance cost per month?

Expect broad ranges: roughly $28–$65 for liability-only part-time riders, $45–$95 for mid-coverage suburban use, $95–$185 for full-time urban riders, and $150–$320 when adding cargo and general liability. Prices vary by state, mileage, bike value, record, and chosen limits. To reach the cheapest options without underinsuring, raise deductibles and match UM/UIM to liability first.