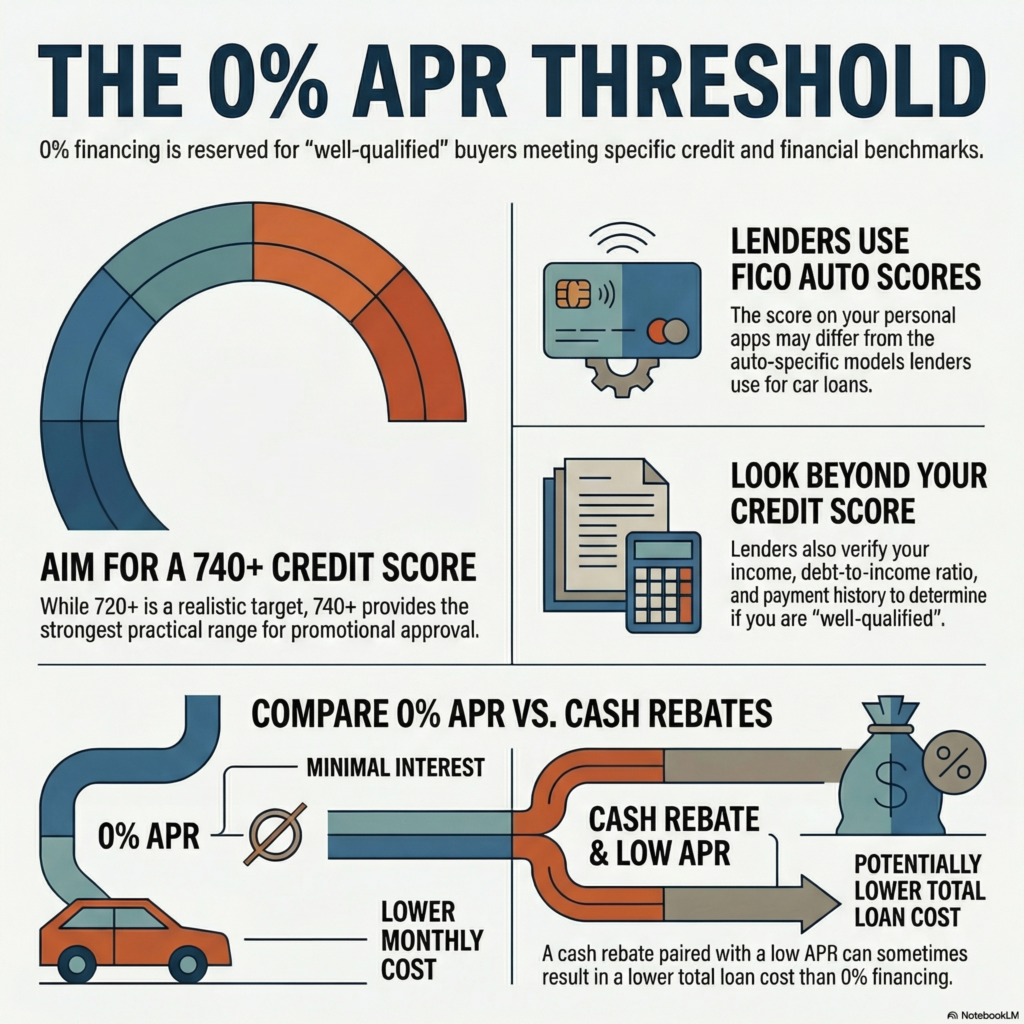

What credit score do you need for 0% car financing? In most cases, buyers need excellent credit, and a practical target is usually 720+, with 740+ giving stronger approval odds. But there is no universal minimum because 0% APR offers are typically limited to “qualified” or “well-qualified” buyers, and lenders may also review your income, debt-to-income ratio, and overall credit profile.

Many shoppers want one exact number, but auto lenders rarely work that way. Some lenders may use FICO Auto Scores rather than the same score you see in a free credit app, which is one reason two buyers with similar scores can get different results.

A Realistic Credit Score Range for 0% Car Financing

A useful rule of thumb looks like this:

- Below 700: usually a weak range for 0% APR offers

- 700 to 719: possible, but not ideal

- 720 to 739: realistic target range

- 740+: strongest practical range

This is not an official lender chart. It is a realistic benchmark based on current guidance that 0% car financing usually goes to borrowers with excellent credit and strong supporting factors.

Why the Required Score Can Vary by Lender

The exact score you need can change based on the lender, the vehicle, and the promotion. Official manufacturer offers pages often use wording like “well-qualified customers” instead of publishing one fixed cutoff. That means your score matters, but so do the specific financing program and the car you are buying. Many 0% deals are also tied to selected new vehicles, not every model on the lot.

What Lenders Check Besides Your Credit Score

Your score is only part of the decision. Lenders may also consider:

- income

- debt-to-income ratio

- payment history

- recent credit applications

- loan term

- total amount financed

The CFPB recommends comparing offers based on the APR, loan term, and total amount financed, not just the monthly payment. That matters because a buyer with a decent score but high debt may still miss a 0% offer, while a buyer with a slightly stronger profile may qualify.

Before you accept a 0% offer, compare these details, not just the monthly payment.

What to Check Before Accepting 0% Car Financing

| What to compare | Why it matters | Sources |

| APR vs interest rate | APR helps you compare the true borrowing cost more accurately than interest rate alone. | What is the difference between a loan interest rate and the APR? |

| Loan term | A longer term can change both affordability and approval odds. | How do I compare auto loan offers? |

| Amount financed | A lower financed amount can reduce risk and improve the structure of the deal. | How do I compare auto loan offers? |

| Score model used | Auto lenders may use a different score model than the one you usually see in credit apps. | Learn About FICO Score Versions and Their Uses |

| Qualification wording | 0% deals are often limited to qualified or well-qualified buyers rather than everyone. | Toyota APR Deals | Toyota Financing Specials |

| Total loan cost | The best deal is the one that costs less overall, not just the one with the lowest monthly payment. | Comparing Auto Loans |

That is why a 0% offer should always be compared with any rebate, loan term, and total borrowing cost before you decide.

Is 0% APR Always Better Than a Rebate?

Not always. Sometimes a cash rebate plus a low APR can beat a 0% deal.

For example, imagine one car comes with either:

- 0% APR for 60 months on a $30,000 price, or

- a $2,500 rebate with a 3.9% APR loan on $27,500

In this example, the 0% offer comes out about $330 cheaper overall, because the $2,500 rebate does not fully cancel out the interest cost on a 60-month loan at 3.9% APR. The 0% option keeps financing cost at $0 interest, while the rebate option lowers the amount financed but adds interest over time. That is why buyers should compare the total cost, not just the headline offer. The CFPB specifically advises comparing APR, loan term, and amount financed before choosing a loan.

What to Do If You Do Not Qualify

If you do not qualify for 0% financing, you still have options. You can compare dealer-arranged financing with banks or credit unions, and you may still qualify for a competitive auto loan even without the promotional rate. Preapproval can also help you compare offers with more confidence before you go to the dealership.

How This Article Was Prepared

This article was prepared using current guidance from Experian, myFICO, Toyota’s finance offers, and the Consumer Financial Protection Bureau. The information was cross-checked across these sources to compare 0% APR qualification wording, credit score expectations, auto-specific scoring models, and the loan terms that most affect total borrowing cost.

FAQs

Can I get 0% car financing with a 700-credit score?

Sometimes, but it is usually not the strongest range. Buyers with higher scores and cleaner credit files generally have better odds.

Do I need a down payment for 0% car financing?

Not always, but a down payment can reduce the amount financed and may improve the overall loan structure. Lender requirements vary.

Is 0% APR usually for new or used cars?

Most 0% APR promotions are tied to new vehicles, not used cars.

Do all lenders use the same credit score?

No. Some auto lenders may use FICO Auto Scores or different score versions, not the exact score you see elsewhere.

Is preapproval better than dealer financing?

Preapproval is not always better, but it gives you a benchmark so you can compare dealer offers more effectively.

Is 0% financing always the cheapest option?

No. Sometimes a rebate plus a low APR loan can cost less overall, so compare total loan cost before deciding.

Does a longer loan term improve approval odds?

Sometimes. A longer loan term can lower the monthly payment, which may help affordability, but it can also increase total interest cost if you do not qualify for a 0% offer.

Will multiple cars loan applications hurt my credit?

A few loan applications made within a short shopping window are often treated as a single rate-shopping event, but too many applications over a longer period can still affect your credit.

Is dealer financing easier to qualify for than bank financing?

Not always. Dealer financing can be more convenient and may include promotional offers, while banks and credit unions may offer better terms for some borrowers. The best option depends on your credit profile and the loan offer.

What is a FICO Auto Score, and why does it matter for 0% financing?

A FICO Auto Score is a credit score version designed for auto lending. Some lenders use it instead of a general credit score, which is why your auto loan decision may not exactly match the score you see in a credit app.

What do lenders verify besides my credit score for a 0% APR offer?

Lenders may also verify your income, debt-to-income ratio, payment history, loan amount, and sometimes your employment details. That is why a strong credit score alone does not always guarantee approval for a 0% financing offer.