What is APR in a car loan? Understand APR, how it differs from interest rate, and how it impacts your monthly payment and total repayment. When people compare car financing offers, one of the most important terms to understand is APR, or annual percentage rate. When people compare car financing offers, one of the most important terms to understand is APR, or annual percentage rate. APR helps show the yearly borrowing cost of a car loan more clearly than looking at the monthly payment alone. According to the Consumer Financial Protection Bureau, the annual percentage rate (APR) is a measure of the cost of credit expressed as a yearly rate.

Many buyers focus first on whether a payment feels affordable. But two car loans can have similar monthly payments and still cost very different amounts over time. That is why APR matters. It gives buyers a better way to compare loan offers before signing.

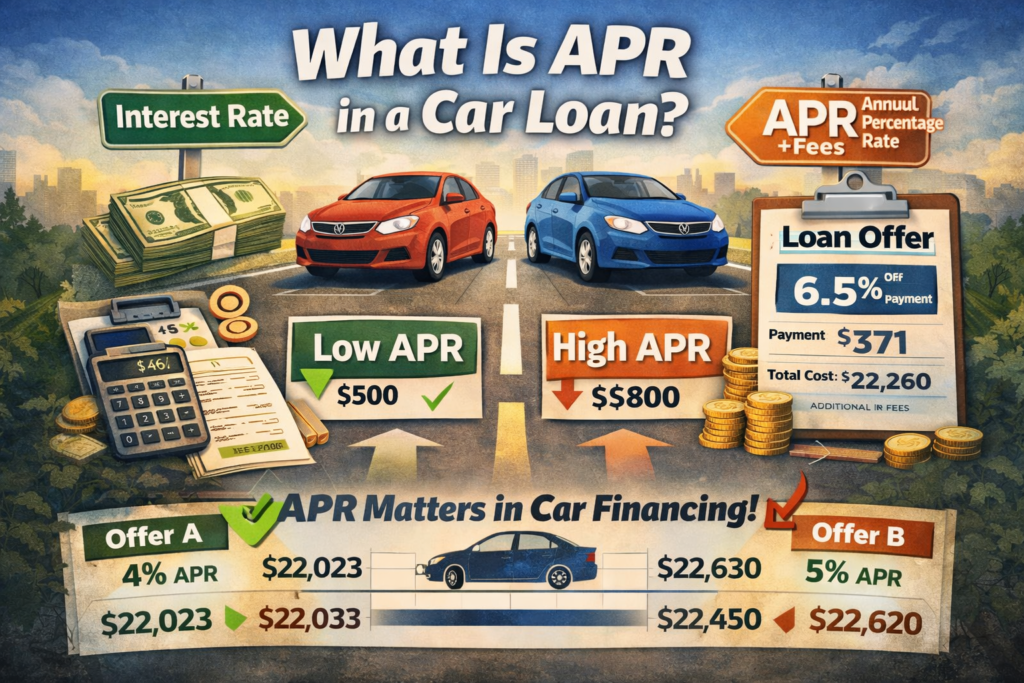

APR vs Interest Rate

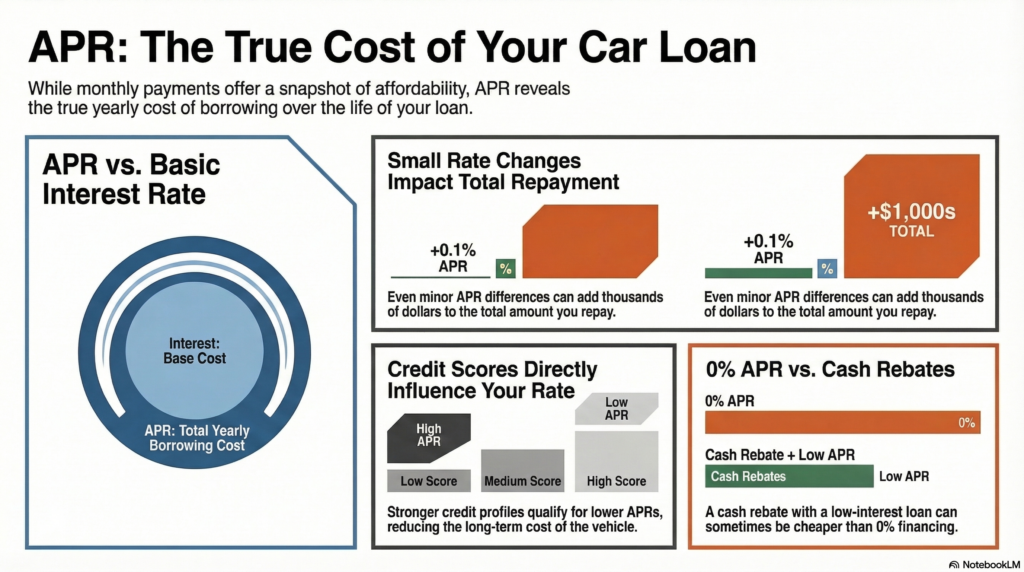

APR is often confused with the interest rate, but they are not always exactly the same. The interest rate is the percentage charged on the money you borrow. APR can provide a broader view of borrowing cost, depending on how the loan is structured.

In simple terms:

- Interest rate = the basic cost of borrowing the money

- APR = the yearly borrowing cost shown as a percentage

That is why APR is often the better number to compare when choosing between car-loan offers.

A Simple Example

Suppose you borrow $20,000 for 60 months.

- A lower APR can reduce both the monthly payment and the total amount repaid

- A higher APR can make the same car cost much more over time

Even if the monthly payment difference looks small, the long-term difference can still add up to hundreds or even thousands of dollars.

Why APR Matters in Car Financing

APR has a direct effect on:

- your monthly payment

- your total interest cost

- the full amount you repay over the life of the loan

A lower APR usually means you pay less overall, assuming the loan term and amount financed stay the same.

That is why buyers should compare more than just the monthly payment. A loan that looks affordable at first may still be expensive if the APR is high or the term is very long.

What Can Affect Your APR?

Lenders usually consider several factors when setting APR, including:

- your credit score

- your income and debt level

- the loan term

- whether the vehicle is new or used

- current market interest rates

Experian’s automotive finance data shows that borrowers with stronger credit profiles generally receive lower average APRs than borrowers with weaker credit profiles. In general, buyers with stronger credit profiles may qualify for lower APR offers, while borrowers with weaker credit may see higher rates.

0% APR Financing

Some dealerships and manufacturers advertise 0% APR financing. This means qualified buyers may borrow money without paying interest during the loan term.

While that can sound like the best deal, it is still important to compare it carefully with other offers. In some cases, taking 0% APR financing may mean giving up a cash rebate or discount.

For example:

- Offer A: 0% APR financing

- Offer B: a cash rebate with a low-interest loan

The better choice depends on the loan amount, the rebate size, the loan term, and the total repayment cost.

How to Compare Two Car-Loan Offers

Before choosing a financing offer, compare:

- the APR

- the loan term

- the monthly payment

- the total amount repaid

- whether a rebate or discount is included

Looking at all of these together gives a clearer picture than focusing on just one number.

How this article was prepared

This article was prepared using general consumer finance education sources, lender information, and publicly available financing guidance. It was reviewed for clarity, structure, and consistency before publication. It is intended for informational purposes only.

Editorial note

This content is not financial or legal advice. Readers should confirm loan terms, APR details, and lender disclosures directly with the dealership, lender, or official financing documents.

FAQs

Is APR the same as the interest rate on a car loan?

Not always. The interest rate is the percentage charged on the amount borrowed, while APR gives a broader view of borrowing cost.

Does a lower APR always mean a better deal?

Often, but not always. Buyers should also compare the loan term, monthly payment, total repayment, and any rebate or discount.

What credit score helps you get a lower APR?

Stronger credit profiles usually help buyers qualify for better rates, but lender standards can vary.

Is 0% APR better than a cash rebate?

Not in every case. Sometimes a rebate with a low-interest loan may create a better total deal.

How does APR affect monthly payments?

A higher APR usually increases both the monthly payment and the total amount repaid over time.

Bottom Line

APR is one of the most important numbers in car financing because it helps show the real borrowing cost of a loan. If you are comparing multiple offers, do not look only at the monthly payment. Check the APR, the loan term, the total amount repaid, and whether any rebate is included.

A car loan may look affordable at first, but a higher APR can quietly make it much more expensive over time. Understanding APR can help you make a smarter financing decision.