Private student debt can feel heavy, especially when the monthly payment takes too much of your budget. That is why many borrowers look into refinancing private student loans. In simple terms, refinancing means replacing your current loan or loans with a new loan from a private lender. The new loan may offer a lower interest rate or a different repayment period, depending on the lender and your borrower profile.

For some borrowers, refinancing can lower interest costs or change the monthly payment, depending on the terms of the new loan. For others, it may not be the right move, especially if important borrower protections would be lost. The key is understanding how private student loan refinance works before you apply. This article is for general education only. It is not personal financial advice. Terms, approval standards, and rates vary by lender, so official lender disclosures and trusted consumer finance sources should be reviewed before making a decision.

Quick summary

Refinancing private student loans may help you:

- get a lower interest rate

- reduce student loan monthly payments

- combine multiple loans into one

- move from a variable interest rate to a fixed interest rate

- shorten or extend your loan term

But it also has risks. A longer repayment period can lower your monthly bill while increasing the amount of interest you pay over time. Approval is not guaranteed, and the best offers usually go to borrowers with stronger credit and stable income.

What is refinancing private student loans?

Refinancing private student loans means taking out a new private loan to pay off one or more existing student loans. After that, you make payments on the new loan instead of the old ones.

This can be useful when the new lender offers:

- a better rate

- a lower monthly installment

- a more suitable repayment period

- an option to refinance multiple private student loans into one account

For example, imagine a borrower with three private student loans at different rates. If that borrower qualifies for one new loan at a better rate, refinancing could simplify payments and possibly save money.

How private student loan refinance works

The process is usually simple on paper, but the details matter.

- You compare lenders.

- You check prequalification, if available.

- The lender reviews your credit history, income, and debt-to-income ratio.

- If approved, the new lender pays off your existing student loans.

- You begin repaying the new refinance loan.

Some lenders offer prequalification, which lets you see possible rates before a full application. In many cases, prequalification uses a soft credit pull that will not affect your credit score. A full application may trigger a hard credit inquiry.

When to refinance private student loans

A refinance can make sense when your financial profile is stronger than it was when you first borrowed.

Good times to consider refinancing

1. Your credit has improved

A better credit score for student loan refinance can help you qualify for stronger terms. Lenders often look more favorably on borrowers who now have a solid payment history and lower credit risk.

2. Your income is more stable

If you have a steady job, regular pay, and manageable debt, lenders may be more willing to approve your application.

3. You want a lower interest rate student loan refinance

Even a small rate reduction can matter over a long repayment period.

4. You want to reduce student loan monthly payments

Extending the repayment period can lower the monthly bill. Just remember that lower monthly payments may mean higher total interest over time.

5. You want to move from a variable rate to a fixed rate

A fixed interest rate offers predictability. A variable interest rate can change over time, which may increase your payment or total cost.

6. You want to release a cosigner

Some borrowers use a refinance to move the debt into their own name. This may help with cosigner release, but approval depends on the borrower’s profile.

Benefits of refinancing private student loans

Lower interest costs

The biggest reason people refinance is the chance to save money. A lower rate can reduce the total loan cost, especially if you keep a reasonable loan term.

Simpler repayment

A borrower who wants to refinance multiple private student loans may prefer one payment instead of several. That can make tracking due dates easier.

Better repayment structure

A new lender may offer a repayment period that fits your budget better.

More predictable payments

Switching from variable interest rate debt to fixed interest rate debt can make future budgeting easier.

Possible cosigner relief

A refinance may allow the original cosigner to be removed, which can help both the borrower and the cosigner.

When refinancing private student loans may be a bad idea

Refinancing can be helpful, but it should not be judged by the monthly payment alone. A lower payment may come from a longer repayment period, and that can raise the total loan cost over time. This is why borrowers should compare both the monthly payment and the full lifetime repayment amount before making a decision.

Approval may also be harder than expected. Lenders often review your credit profile, income, and debt to income ratio before making an offer. A borrower who looks stronger on paper is more likely to receive better terms than a borrower with weaker credit or unstable income. Official lender pages such as SoFi’s student loan refinance rates page, Earnest’s refinance page, and Citizens’ student loan refinance page make clear that final rates and approval depend on underwriting and borrower qualifications.

Important Terms and Application Risks

Another risk is relying too much on early rate checks and not enough on the final disclosure. Some lenders let you check rates before a full application, but a full application may involve a hard credit inquiry. The CFPB’s explanation of credit inquiries and Equifax’s guide to hard and soft inquiries can help borrowers understand that difference before applying.

Borrowers should also review lender-specific terms closely. These can include repayment flexibility, rate type, available term lengths, and cosigner release rules. For example, Citizens Bank’s student loan refinance page includes lender-specific product details that borrowers should compare before choosing an offer.

Private student loan consolidation vs refinance

These two terms are often confused.

| Topic | Refinance | Consolidation |

| Main purpose | Replace old loans with a new private loan | Combine loans into one loan |

| Interest rate | May be lower, higher, fixed, or variable depending on lender and borrower profile | May not always reduce cost |

| Credit review | Usually yes | Depends on the product type |

| Savings potential | Possible if you get better terms | Depends on the structure |

| Common use | Lower cost, better rate, simpler repayment | Simplify payments |

When people search private student loan consolidation vs refinance, they are often trying to decide between convenience and savings. In practice, refinancing may also combine loans, but its bigger goal is usually to improve the loan terms.

Refinance vs consolidation: why the difference matters

Many borrowers use the words refinancing and consolidation as if they mean the same thing, but they do not. The two options may both combine loans, yet they serve different purposes.

A federal Direct Consolidation Loan combines eligible federal student loans into one new federal loan with one monthly payment. Private loans are not eligible for that federal program. Federal Student Aid also explains that federal loans cannot be refinanced within the federal student aid system, even though they can be consolidated there.

Refinancing and Consolidation Are Not the Same

Refinancing, on the other hand, is done through a private lender. The goal is usually to get a new interest rate, a different loan term, a different rate type, or a more suitable repayment structure. A refinance loan may also combine more than one loan into a single payment, but its main value is improvement of terms rather than simple loan grouping. The Consumer Financial Protection Bureau explains this distinction clearly for borrowers comparing their options.

This difference matters because the right choice depends on the borrower’s goal. If the goal is simpler repayment for federal loans, consolidation may be the relevant concept. If the goal is a lower rate, a fixed rate, or a more manageable term, refinancing is usually the better comparison point.

If a borrower has any federal loans mixed into the picture, this decision needs extra care. The CFPB student loans resource center is a good place to review borrower protections and key differences before choosing a private refinance route.

Private student loan refinance requirements

Each lender has its own rules, so there is no single approval formula. Still, these are common factors:

Credit history

The lender may review your payment history, open accounts, and overall credit strength.

Income

Stable income helps show that you can handle the new repayment obligation.

Debt to income ratio

This compares your monthly debt obligations with your income. A lower ratio is often stronger.

Employment stability

A consistent job history can support your application.

Graduation status

Some lenders may prefer applicants who completed their program, though this varies.

Cosigner support

If you cannot qualify alone, a cosigner may improve your approval chances. On the other hand, some borrowers refinance to remove a cosigner once their own profile is strong enough.

How to refinance private student loans step by step

Review your current loans

List each balance, rate, monthly payment, and repayment period. This gives you a clear picture of what you are replacing.

Set your goal

Ask yourself what matters most:

- lower monthly payments

- lower total loan cost

- fixed rate stability

- simpler repayment

- cosigner release

Your goal should shape your lender comparison.

Check your credit and budget

Before applying, review your credit and monthly budget. This helps you judge whether you are likely to qualify and what payment is realistic.

Compare lenders

Look at:

- fixed and variable rate options

- loan term choices

- borrower protections

- prequalification availability

- repayment flexibility

- cosigner policies

Use prequalification where possible

Prequalification can give you a preview of possible terms before a full application.

Review the final offer carefully

Do not focus only on the monthly bill. Review:

- annual rate

- repayment period

- total loan cost

- payment start date

- late payment rules

Complete the refinance

Once approved, the new lender usually pays the old loan directly. Keep making payments on your current loan until the payoff is confirmed.

What lenders usually review

When lenders assess a refinance application, they often focus on whether the borrower looks financially stable today, not just when the original student debt was taken out.

A lender comparison should include:

- credit profile

- income level

- employment consistency

- existing debt load

- requested loan term

- whether you apply with or without a cosigner

This is why borrowers often get better results when they refinance after improving their finances.

Fixed interest rate vs variable interest rate

This choice matters.

Fixed interest rate

- stays the same over time

- easier to budget

- more predictable

Variable interest rate

- can go up or down

- may start lower

- less predictable over the full repayment period

Borrowers who value stability often prefer fixed rates. Borrowers who accept more risk may consider variable rates, but they should understand that future payments can change.

Common mistakes to avoid

Choosing the lowest monthly payment without checking the full cost

A lower payment can hide a longer repayment period and more interest.

Applying before improving your credit

A stronger profile may lead to better offers.

Ignoring lender details

Not all refinance loans offer the same protections or service quality.

Focusing only on the rate

The loan term, flexibility, and repayment rules matter too.

Forgetting the cosigner issue

If your goal is releasing cosigner student loan refinance, confirm that the new loan will actually remove the prior cosigner obligation.

Practical tips before you apply

- Check your credit report for errors

- Pay down other debt if possible

- Avoid taking on new debt before applying

- Compare several lenders, not just one

- Use prequalification first when available

- Read every disclosure carefully

- Keep copies of all loan details and payoff confirmations

Myths vs facts

Myth: Refinancing always saves money

Fact: It can save money, but only if the new terms are actually better for your situation.

Myth: The lowest rate is always the best deal

Fact: A shorter term with a slightly different rate may still be better than a long term with lower monthly payments.

Myth: You should refinance the moment you graduate

Fact: Sometimes waiting until your income and credit improve can lead to better results.

Myth: You cannot refinance multiple private student loans

Fact: Many lenders allow borrowers to combine several private loans into one refinance loan.

Myth: Refinancing is only about lower payments

Fact: It can also be about predictability, simplicity, and cosigner release.

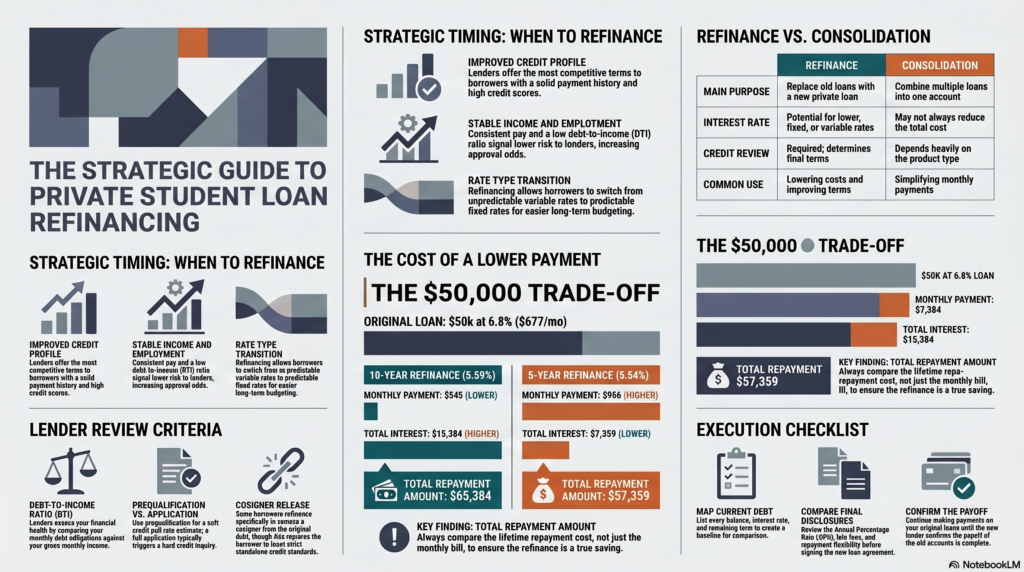

A simple real-world example

Suppose a borrower has $50,000 in student debt at a 6.8% fixed APR, is paying about $677 per month, and has 8 years left on repayment. To compare refinancing options, the borrower reviews credit reports and then checks official lender refinance offers.

In Citizens’ public example, the borrower considers a 5-year refinance at 5.54% APR, a 7-year refinance at 5.57% APR, and a 10-year refinance at 5.59% APR. Those options produce estimated monthly payments of about $956, $720, and $545, with total interest paid of about $7,359, $10,494, and $15,384. This shows why refinancing should be judged by both the monthly payment and the total repayment cost. A lower monthly bill can help cash flow, but a longer term can still increase what the borrower pays over time.

FAQ

Can I refinance private student loans with bad credit?

It may be harder. Some lenders require a stronger credit profile. A cosigner may help in some cases, but rules vary by lender.

Does refinancing private student loans hurt credit?

A full application may involve a hard credit inquiry. That can affect credit temporarily, but the impact depends on the borrower’s overall credit profile and later payment behavior.

Can I refinance multiple private student loans into one?

Yes, many lenders allow borrowers to combine multiple private student loans into one new refinance loan.

What credit score do I need for student loan refinance?

There is no universal number because lender standards differ. In general, stronger credit tends to improve approval odds and rate offers.

When should I refinance private student loans?

It may make sense when your income is stable, your credit has improved, and you can qualify for terms that clearly support your fin