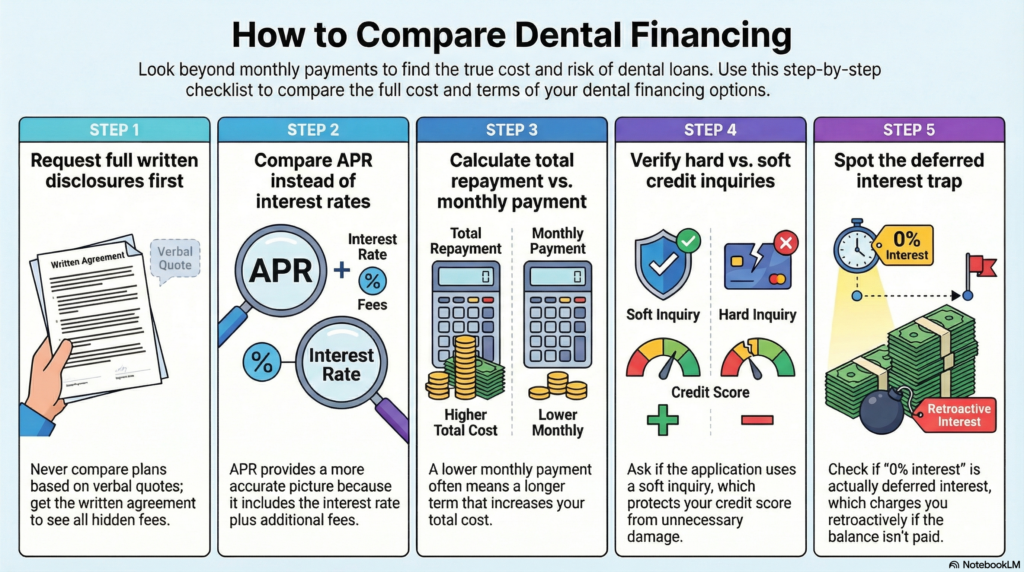

To compare dental financing plans, do not focus only on the monthly payment. Compare the APR, interest rate, fees, repayment term, total amount financed, total repayment, credit-check type, missed-payment consequences, and any promotional conditions such as deferred interest. A lower monthly payment can still cost more overall if the term is longer or the fees and interest are higher. The CFPB specifically advises consumers comparing loans to look at the APR, interest rate, loan term, and total amount financed, not just the payment amount.

What a dental financing plan is

A dental financing plan is any arrangement that lets you pay for dental care over time instead of all at once. In practice, that can include an in-house payment plan from the provider, third-party installment financing, a medical credit card, a general-purpose credit card, or sometimes a personal loan used for treatment costs. Some healthcare payment products are designed specifically for medical or dental expenses, while others are general borrowing options used for the same purpose.

The main types of dental financing plans

In-house payment plans

These are payment arrangements offered directly by a dental office. Terms vary by provider, so the key questions are simple: how long you have to pay, whether there are fees or interest, what happens if you miss a payment, and whether treatment must be completed at that office. Provider plans can be straightforward, but the details are not standardized, so the written agreement matters.

Third-party installment financing

These plans let you repay treatment costs over time through a financing company or lender. The lender may check your credit when you apply, and the cost depends on the APR, fees, term length, and payment rules. If a lender runs a hard inquiry when you apply, that can affect your credit score; soft inquiries generally do not.

Medical credit cards

Medical credit cards are designed for healthcare expenses, including dental treatment. The CFPB warns that some medical financing products can be costly and that consumers may not fully understand the terms, especially when deferred interest is involved. These products may look attractive upfront, but the details matter more than the headline offer.

General-purpose credit cards

A regular credit card may be convenient, but it is still borrowing. The real comparison points are the APR, fees, promotional conditions, and what happens after any introductory period ends. If the balance is not paid quickly, the overall cost can rise fast.

Personal loans

A personal loan can sometimes be part of the comparison if you are paying for a larger dental bill and want fixed payments over a set term. The same comparison logic applies: APR, fees, term, monthly payment, and total repayment.

What to compare first

APR vs. interest rate

Interest rate and APR are not the same. The CFPB explains that the interest rate is the cost of borrowing, while the APR reflects the interest rate plus certain additional fees. When you are comparing financing offers, APR is usually the better comparison tool because it gives a fuller picture of borrowing cost.

Monthly payment vs. total repayment

A longer term may lower the monthly payment, but it can increase the total amount repaid.

Fees

Check for application fees, account fees, late fees, processing fees, or any charge tied to missed payments or promotional financing. Not every plan has the same fee structure, and some provider or lender terms may only appear in the disclosures.

Credit-check type

If the plan requires an application, ask whether it involves a soft inquiry or a hard inquiry. The CFPB explains that hard inquiries are commonly tied to credit applications and can affect your credit score, while soft inquiries generally do not. That does not mean one plan is automatically better, but it does mean the credit-check type should be part of the comparison.

Prequalification vs. full application

Some dental financing providers may let you check offers through prequalification before you complete a full application. Prequalification can be useful, but it is not always the same as final approval. The final terms may still depend on a full review of your application, credit profile, and provider details. Before you move forward, confirm whether you are only being prequalified or fully approved, and ask whether the process involves a soft inquiry or a hard inquiry. This helps you compare offers more accurately and avoid confusion about your actual approval status.

Missed-payment consequences

Always check what happens if you miss a payment. Depending on the plan, that could mean a late fee, added interest, account delinquency, collections activity, or a credit impact. This is especially important with products that look simple at signup but become expensive when the terms are broken.

Deferred interest risk

Deferred interest is not the same as true zero-interest financing. The CFPB warns that some medical credit cards use deferred interest, which can lead to retroactive interest charges if the full balance is not paid by the end of the promotional period. Consumers have paid substantial deferred interest on healthcare financing, so this is not a minor footnote. If a dental financing offer uses promotional language, check whether it is truly no-interest or deferred-interest financing.

Where the plan can be used

Some financing options can only be used with participating providers or within one office, while general-purpose credit products are broader. That matters if your treatment plan changes, you need a specialist, or you want flexibility later. It is worth confirming this before treatment starts, especially if referrals or follow-up care may be needed.

How to compare dental financing plans step by step

Ask for the written terms

Do not compare plans from memory or based on what was said verbally. Get the written disclosures or agreement for each option.

Put the key terms side by side

For each option, list:

- APR

- interest rate

- fees

- repayment term

- monthly payment

- total amount financed

- total repayment if shown

- credit-check type

- missed-payment consequences

- early payoff terms

- provider restrictions

The goal is to compare like with like. If one plan gives only a monthly payment but not the full borrowing cost, it is not giving you enough to compare properly.

Look past the promotional headline

If a plan says “0%,” “low payment,” or “special financing,” read the conditions. Ask whether the offer is true no-interest financing or deferred interest, whether fees apply, and what happens if you are late. The CFPB has specifically warned consumers about medical financing products with terms that may not be fully understood at the point of care.

Decide what matters most for your situation

If cash flow is tight, the monthly payment matters. If you can pay faster, the total repayment may matter more. If you are protecting your credit, the inquiry type and delinquency rules matter more. A plan that is acceptable for one person may be risky for another.

Read the default and late-payment section

This is where many bad surprises live. Check the exact consequences of being late, missing a payment, or failing to repay a promotional balance on time.

Comparison table

| Option type | What to compare | Possible upside | Possible downside | Who it may suit |

| In-house payment plan | Fees, term length, missed-payment rules, office restrictions | May be simpler and easier to understand | Terms vary by office; may be usable only with that provider | Readers who want a direct provider arrangement |

| Third-party installment financing | APR, fees, term, total repayment, credit-check type | Structured payments may make budgeting easier | Cost and approval terms vary; hard inquiry may apply | Readers comparing fixed-payment options |

| Medical credit card | APR, promotional terms, deferred interest risk, late-payment rules | May offer short-term promotional financing | Deferred interest can be costly if the balance is not paid on time | Readers who can manage the promotional terms carefully |

| General-purpose credit card | APR, fees, promotional terms, total cost if balance carries | Flexible use beyond one provider | Can become expensive if the balance is not paid quickly | Readers who already have a card and a payoff plan |

| Personal loan | APR, origination fees if any, term, monthly payment, total repayment | Predictable repayment over a set term | Terms vary by lender and credit profile | Readers financing a larger treatment bill |

Risk / red flags section

The biggest red flag is a plan that looks affordable only because the monthly payment is low. A longer term can make the payment easier while increasing the total cost.

Another red flag is unclear promotional language. If the plan mentions “special financing,” “promotional financing,” or similar wording, check whether that means true no-interest financing or deferred interest. The CFPB has warned that deferred interest in medical financing is commonly misunderstood and can lead to retroactive interest charges if the full balance is not repaid in time.

Be careful if the provider or lender cannot clearly answer these questions:

- Is the credit check hard or soft?

- What is the APR?

- What fees apply?

- What happens if I miss one payment?

- Can I pay early without a penalty?

- Is this plan limited to this office or provider network?

If you do not get clear written answers, slow down.

Checklist section

Before choosing a dental financing plan, check:

- Compare APR to APR, not APR to interest rate.

- Look at the monthly payment and the total repayment

- Confirm all fees

- Check the repayment term

- Ask whether the application uses a hard inquiry or soft inquiry.

- Check whether any promotion is deferred interest

- Read the late-payment and default rules

- Ask whether early payoff changes anything. Check whether paying early lowers your total cost and whether any promotional terms change if you pay ahead of schedule.

- Confirm whether the plan is limited to one provider or participating providers only

- Do not sign until you have read the disclosures

FAQ section

Is the lowest monthly payment always the best dental financing plan?

No. A lower monthly payment can come from a longer term, which may increase the total amount you repay over time. The better plan is the one that fits your budget and has acceptable total cost and risk.

What is the difference between APR and interest rate?

The interest rate is the cost of borrowing money. APR includes the interest rate plus certain additional fees, so it is usually the better comparison tool when you are reviewing financing offers.

Can a dental financing application affect my credit score?

It can. If the lender uses a hard inquiry as part of the application, that can affect your credit score. Soft inquiries generally do not. Ask before you apply.

What is deferred interest and why does it matter?

Deferred interest means interest may be charged retroactively if you do not pay the full balance within the promotional period. The CFPB has warned that this feature is commonly misunderstood in medical financing products.

Is an in-house payment plan safer than a medical credit card?

Not automatically. An in-house plan may be simpler, but the right choice depends on the written terms, fees, missed-payment consequences, and whether the plan limits where you can receive care. Compare the terms, not the label.

What should I read before accepting a dental financing offer?

Read the APR, fees, repayment term, total amount financed, promotional conditions, credit-check type, late-payment rules, and any deferred-interest language before you agree.

Final verdict

The safest way to compare dental financing plans is to ignore the headline and compare the actual terms. Start with APR, fees, term length, total repayment, credit-check type, and missed-payment rules. Treat promotional financing with extra caution, especially if deferred interest might apply. If the provider or lender cannot give you clear written terms, that is a reason to pause, not a reason to rush.

Pingback: Cherry Dental Financing: Complete Guide to Making Dental Care - moneymentordesk.com