How Many Personal Loans Can You Have at Once?

How many personal loans can you have at once? There is generally no fixed legal cap — you can hold several personal loans at the same time. In practice, individual lenders set their own limits (often one or two per borrower), and approval depends on your credit score, income, and debt-to-income (DTI) ratio. Whether you should take another loan comes down to affordability, not a magic number. This guide explains the real rules, shows real lender policies, helps you check what you can afford, and covers both the US and the UK.

Key takeaways

- There’s no single law capping how many personal loans you can have — but each lender sets its own limits and must check you can repay.

- Major lenders like SoFi and LendingClub cap you at two active personal loans, with conditions.

- You can also borrow from different lenders, but you must qualify each time, and every application adds a hard inquiry.

- Your debt-to-income (DTI) ratio is the deciding number. Many lenders want 36% or lower.

- On-time payments build credit, but more loans raise the risk of missed payments and a debt-trap cycle.

Can you have more than one personal loan?

Yes. There is generally no fixed legal cap on how many personal loans you can have at once. Nothing in US or UK law stops you from holding two, three, or more active loans at the same time. The limits come from individual lenders and from your own finances — a lender will only approve a new loan if it believes you can repay it on top of your existing debt.

So, the real question isn’t “is it allowed?” — it’s “will a lender approve me, and can I afford it?” That comes down to your credit profile and your DTI, which we break down below.

How many personal loans can you have — same lender vs. different lenders?

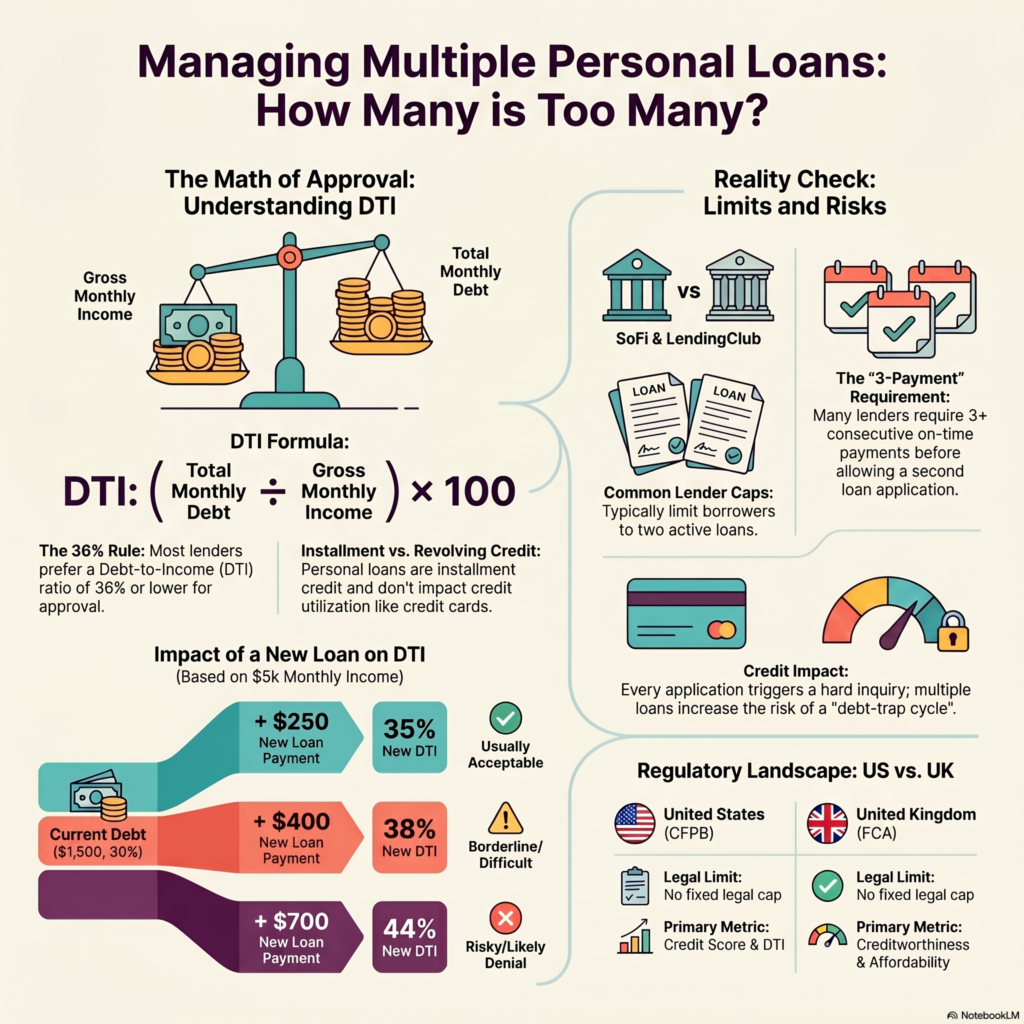

Most lenders allow one or two loans per borrower; there’s no overall cap across different lenders. With the same lender, you’ll often hit a limit of two loans or a maximum combined balance. With different lenders, there’s no industry-wide cap — but you must qualify for each loan separately.

| Scenario | Typical limit | What to know |

| Same lender | Often 1–2 loans, or a maximum combined balance | Many lenders require several on-time payments before a second loan |

| Different lenders | No overall cap | You must qualify each time; every application adds a hard inquiry and more debt to your DTI |

Real lender examples

The clearest way to see this is in published lender policies. Two of the largest US personal-loan lenders both cap borrowers at two loans, with conditions:

| Lender | Max active personal loans | Key conditions |

| SoFi | 2 | You must make 3 consecutive on-time payments on your first loan before applying for a second. Michigan residents are limited to 1. |

| LendingClub | 2 | Combined balance must stay under $50,000, and you need 3–12 months of on-time payments on the first loan first. |

Policies as published by SoFi and LendingClub (2026). Lender rules change and vary by state, so always confirm current terms on the lender’s own site before applying.

How do multiple personal loans affect your credit?

Multiple personal loans affect your credit in four main ways: hard inquiries, payment history, credit mix, and how much you owe. Used well, they can help your score; used carelessly, they can hurt it.

- Hard inquiries. Each application triggers a hard credit check, which Experian notes can lower your score by a few points temporarily. Several applications in a short window add up.

- Payment history. This is the biggest factor in your score. Every on-time payment helps; one missed payment on any loan can hurt.

- Credit mix. Adding an installment loan can slightly help your mix if you mostly have credit cards — but this is a minor factor.

- Amounts owed and DTI. More loans mean more debt. A high DTI makes future borrowing (a mortgage, a car) harder and pricier.

Because personal loans are installment loans (a fixed amount repaid in equal payments), they don’t affect your credit utilization ratio the way credit cards do. Utilization applies to revolving credit like cards. According to Experian, keeping card utilization under 30% protects your score — but that rule is about cards, not personal loans.

Quick DTI check: can you afford another personal loan?

To see if you can afford another loan, work out your debt-to-income ratio — the single number lenders use to decide. Divide your total monthly debt payments by your gross monthly income. Many lenders look for 36% or lower, though some accept up to 43–50% depending on your credit, per CFPB guidance.

Quick DTI formula Monthly debt payments ÷ gross monthly income × 100 = your DTI Example: $1,750 ÷ $5,000 × 100 = 35% DTI Aim to keep it at or below 36%.

Here’s how adding a second loan can change the math:

| Gross monthly income | Current debt payments | + New loan payment | New DTI | Likely lender view |

| $5,000 | $1,500 (30%) | +$250 | $1,750 → 35% | Usually acceptable (under 36%) |

| $5,000 | $1,500 (30%) | +$400 | $1,900 → 38% | Borderline — over the 36% comfort zone |

| $5,000 | $1,500 (30%) | +$700 | $2,200 → 44% | Risky — likely a higher rate or denial |

Figures are an illustrative example, not a quote. It’s not about how many loans you have — it’s whether the new payment keeps your DTI healthy. Run your own numbers before you apply.

Pros and cons of having multiple personal loans

Multiple personal loans can solve a real cash need and build credit, but they also raise your risk of missed payments and a debt spiral. Weigh both sides before you borrow again.

| Pros | Cons |

| Cover a second, separate expense | More monthly payments to juggle |

| On-time payments build credit history | Each application is a hard inquiry |

| Can consolidate other debts into one payment | Higher DTI limits future borrowing |

| May beat credit-card interest rates | Greater risk of missing a payment or defaulting |

A second loan can be smart for debt consolidation — using a new loan to pay off higher-interest debt. It’s risky if you’re borrowing to cover everyday bills, which can signal a deeper budget problem.

Warning: Don’t take out a second personal loan just to keep up with payments on the first. That’s a common path into a debt cycle. If you’re borrowing to cover existing repayments, speak with a nonprofit credit counselor in the US, or free, government-backed MoneyHelper in the UK, before borrowing more.

How to qualify for another personal loan

To qualify for another personal loan, strengthen the same things lenders checked the first time: your credit score, your DTI, your income, and your payment history. Work through these steps before you apply.

- Check your credit score so you know which lenders you can realistically target.

- Lower your DTI by paying down existing balances — the fastest way to improve your odds.

- Make several on-time payments on your current loan first; many lenders require this (SoFi asks for three).

- Avoid new hard inquiries in the weeks before you apply.

- Show steady or higher income, which improves your DTI and reassures lenders.

- Prequalify with a soft credit check where possible, so you can compare offers without hurting your score. (See our guide on what credit score you need for the best financing.)

Alternatives to taking out another personal loan

Before stacking another loan, compare alternatives that may cost less or protect your credit. Depending on your need, one of these may be a better fit:

- 0% APR credit card or balance transfer — useful for short-term needs you can repay quickly.

- Home equity loan or HELOC — often lower rates if you own a home, but your home is collateral.

- Refinance or top up your existing loan — one larger loan can be simpler than two. Learn how rates work in our guide to APR and the true cost of borrowing.

- Credit union loan — credit unions often offer lower rates and more flexible approval than banks.

- A debt-consolidation loan — rolls multiple debts into one payment, which can lower your rate and simplify repayment.

How many personal loans can you have in the UK?

In the UK there’s also no legal limit on how many personal loans you can have, but every lender must run affordability and creditworthiness checks. UK lenders are regulated by the Financial Conduct Authority (FCA), which requires them to check you can repay before lending. You can hold loans with several providers, but each application is assessed on your income, existing debt, and credit file, and each leaves a footprint on your credit report.

Here’s how the picture compares on each side of the Atlantic:

| Topic | United States | United Kingdom |

| Legal limit on number of loans | No fixed legal cap | No fixed legal cap |

| Main approval check | Credit score, income, DTI | Creditworthiness + affordability |

| Regulator / guidance | CFPB, credit bureaus | FCA, MoneyHelper |

| Main warning sign | High DTI | Unaffordable repayments |

If you’re juggling repayments in the UK, free and impartial help is available from MoneyHelper, which is backed by the UK government.

Bottom line: is a second personal loan right for you?

Having more than one personal loan is allowed and can be a smart move — but only if the new payment keeps your DTI healthy and you have a clear plan to repay. There’s no magic number; there’s only what your budget and your credit can support. Borrow only what you need, check your DTI first, compare lenders (and alternatives), and never take a second loan just to cover the payments on the first. If another loan would push you near or over a 36% DTI, that’s usually a sign to pause.

Frequently asked questions

Is it illegal to have multiple personal loans?

No. It is not illegal to have multiple personal loans in the US or the UK, and there’s no legal cap on the number. Limits are set by individual lenders and by your own finances — mainly your credit score and debt-to-income ratio — not by law.

Can you have two personal loans at once?

Yes. You can have two personal loans at once, from the same lender or from two different lenders. Major lenders like SoFi and LendingClub both allow up to two. You’ll need to qualify for the second loan separately, and the new payment must still fit your DTI.

Can you have two loans with the same lender?

Often, yes. Many lenders cap a single borrower at two loans or a maximum combined balance. SoFi and LendingClub both allow two, but require several on-time payments on the first loan first. Always check that lender’s specific policy.

Does having multiple personal loans hurt your credit?

It can go either way. Each application adds a hard inquiry that lowers your score slightly, and more debt raises your DTI. But making every payment on time builds a positive payment history, which is the biggest factor in your credit score.

How many personal loans is too many?

There’s no set number — it’s too many when the payments push your debt-to-income ratio too high (often above 36%) or when you struggle to keep up. If you’re borrowing to cover existing loan payments, you already have too many.

Is a personal loan installment or revolving credit?

A personal loan is installment credit: you borrow a fixed amount and repay it in equal monthly payments over a set term. Revolving credit, like a credit card, lets you borrow, repay, and borrow again up to a limit.

Can I use a second personal loan to pay off the first?

You can, and this is essentially refinancing or debt consolidation. It can help if the new loan has a lower interest rate or a single, more manageable payment. But watch for origination fees and longer terms that raise the total cost. Don’t roll into a new loan just to delay payments.

How long should you wait before applying for another personal loan?

It depends on the lender. SoFi and LendingClub require three or more consecutive on-time payments on your first loan before a second. Even where there’s no rule, waiting several months lets a hard inquiry fade and shows lenders you can manage the first loan.

Can multiple personal loans affect mortgage approval?

Yes. Personal loan payments raise your debt-to-income ratio, which mortgage lenders weigh heavily. Multiple loans — plus any recent hard inquiries — can lower the mortgage amount you qualify for or push up your rate. Many buyers pay loans down before applying for a mortgage.

About this guide

Written by: Nimra Saleem, founder of MoneyMentorDesk.com, who writes plain-English money guides researched from official and primary sources.

How we researched this guide: MoneyMentorDesk reviewed consumer-finance guidance from the CFPB, Experian, the FCA, and MoneyHelper, and checked the published multiple-loan policies of major lenders (SoFi and LendingClub). We then explained how holding more than one personal loan affects affordability, credit checks, and your debt-to-income ratio. This guide is educational only and does not recommend borrowing more than you can afford.

Sources: CFPB — debt-to-income ratio · Experian — credit utilization · Experian — hard inquiries · SoFi — multiple loans policy · LendingClub — additional loans · FCA · MoneyHelper

Disclaimer: This article is for general education only and is not financial advice. Lender rules, rates, and DTI thresholds vary and change over time. Confirm current terms with a lender and speak to a qualified professional, a nonprofit credit counselor (US), or a free service such as MoneyHelper (UK) before borrowing.