Dealer vs Bank Financing: Which Is Better for Your Car Loan?

When you buy a car on finance, you usually have two main paths: arrange the loan yourself through a bank or credit union before you visit the dealership, or let the dealer arrange it for you on the spot. Both can work, but they work very differently — and the choice can affect how much you pay over the life of your loan.

This guide covers dealer vs bank financing in full — what each option means, how much each can cost, and how to use both to get a better deal.

Quick Answer

Dealer financing is arranged through the dealership, which submits your application to one or more lenders and may add a markup to the rate. Bank or credit union financing means you borrow directly from the lender before you shop, giving you a fixed rate and negotiating power at the dealer.

For most buyers, getting pre-approved by a bank or credit union first — then comparing that offer against what the dealer can beat — is the strategy most likely to result in a lower total cost.

Key Takeaways

- Dealer financing is convenient but often includes a markup above the lender’s base rate.

- Bank and credit union financing gives you a locked rate before you walk into a dealership.

- 0% APR deals from manufacturers are a genuine exception — they can be better than any bank offer.

- Getting pre-approved first gives you leverage to negotiate at the dealer.

- Always compare the total amount you will repay, not just the monthly payment.

What Is Dealer Financing?

Dealer financing — also called indirect financing — is when the dealership arranges a loan on your behalf. You fill out a credit application at the dealer, and the dealer submits it to one or more lenders they work with, such as banks, finance companies, or captive lenders owned by the manufacturer.

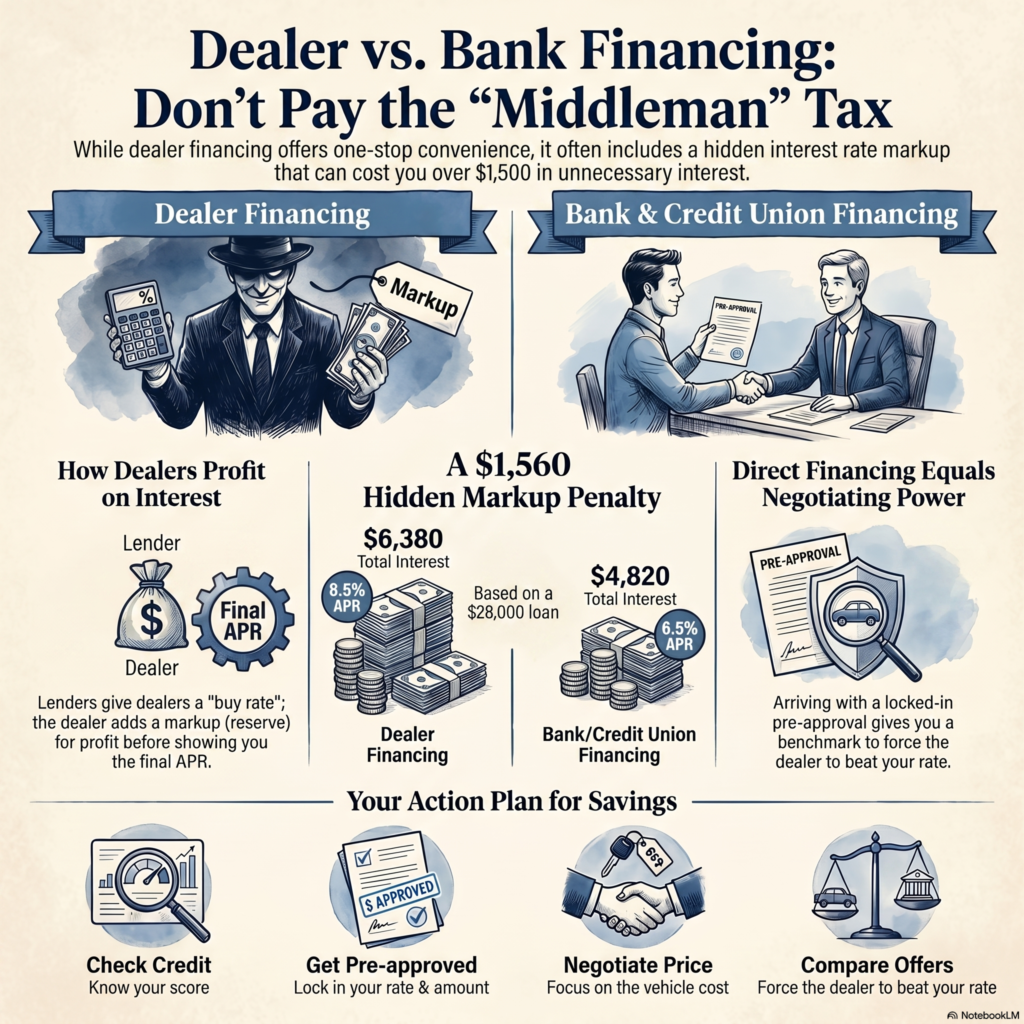

The lender gives the dealer a rate — called the buy rate — at which they are willing to fund the loan. The dealer is often allowed to mark up that rate before presenting it to you, keeping the difference as profit. This markup is sometimes called dealer reserve.

According to the Federal Trade Commission (FTC), when you finance through a dealer, the dealer is the one negotiating your loan terms — not you. This is why it is important to understand what you are being offered before you agree.

Dealer financing is also how 0% APR manufacturer deals are arranged. These are different — the manufacturer subsidises the rate to zero, so there is no markup. These can be genuinely good deals for qualified buyers.

What Is Bank or Credit Union Financing?

Bank or credit union financing — also called direct lending — means you apply for a loan directly with the lender before visiting the dealership. If approved, you receive a pre-approval letter stating the loan amount, interest rate, and term you qualify for.

You then use that pre-approval as your benchmark when visiting the dealer. If the dealer cannot match or beat your rate, you use your own financing.

Credit unions often offer lower rates than traditional banks because they are member-owned and not profit-driven. Online lenders are another option and allow you to compare rates from multiple sources quickly.

The CFPB’s auto loan shopping guide recommends getting a pre-approval from a bank or credit union first so you can better negotiate terms — whether you end up using that lender or the dealer’s offer.

Dealer vs Bank Financing: Full Comparison Table

| Dealer Financing | Bank Financing | Credit Union | Online Lender | |

| Rate control | Dealer sets rate (may mark up) | You see the exact rate | You see the exact rate | You see the exact rate |

| Pre-approval available? | No — rate set at dealership | Yes | Yes | Yes |

| 0% APR deals | Yes (manufacturer offers) | No | No | No |

| Rate typically | Higher (markup included) | Moderate | Usually, lowest | Varies |

| Convenience | High — one stop | Requires extra step | Requires extra step | Easy online |

| Negotiating power | Low — you see one offer | High — use as benchmark | High — use as benchmark | High — use as benchmark |

| Best for | Manufacturer 0% deals, speed | Buyers with existing banking relationship | Buyers prioritising lowest rate | Comparison shoppers |

When Dealer Financing Makes Sense

Dealer financing is not always the wrong choice. There are specific situations where it works in your favour:

1. Manufacturer 0% APR deals When a manufacturer offers 0% financing on a new model, the rate is subsidised — meaning there is no markup, and no bank will beat it. If you qualify (typically requires strong credit), this is often the best deal available. Check the manufacturer’s website directly to confirm current offers.

2. You are short on time If you need a car quickly and have not had time to shop lenders, dealer financing gets the deal done in one visit. Just know the trade-off: you may pay a higher rate than if you had shopped first.

3. The dealer can genuinely beat your pre-approval Dealers work with multiple lenders and sometimes have access to rates you cannot get directly. If you have a pre-approval and the dealer beats it with a verified offer showing the same term and total cost — take it.

When Bank or Credit Union Financing Makes Sense

For the majority of car buyers, going to a bank or credit union first is the better strategy:

1. You want to know your rate before you shop Walking into a dealership with a pre-approval removes uncertainty. You know your maximum rate, your monthly payment range, and your budget before a dealer says a word.

2. You want negotiating leverage Dealers make money on financing. When you show a pre-approval, you are in a stronger position to ask the dealer to match or beat it — or to walk away if they cannot.

3. You have time to compare lenders Checking your credit report first, then applying to two or three lenders, takes a few days but can save you hundreds or thousands of dollars over a 48–72 month loan. You can get your free credit report at AnnualCreditReport.com — the only site federally authorised to provide it free.

4. You are buying a used car Manufacturers only offer subsidised rates on new vehicles. For used cars, dealer financing is standard bank lending with a potential markup. Getting direct financing almost always makes more sense for used car purchases.

Which Option Is Right for Your Situation?

| Your Situation | Best Option | Why |

| New car, manufacturer offering 0% APR | Dealer financing | Subsidised rate — no markup, no bank will beat it |

| Buying a used car | Bank or credit union | No manufacturer deals on used cars; dealer adds markup |

| First-time buyer, good credit | Bank or credit union first | Get a benchmark rate, then give the dealer a chance to beat it |

| In a rush, no time to shop lenders | Dealer financing | Convenient, but expect to pay a higher rate |

| Member of a credit union | Credit union | Often the lowest available rate; member-owned, not profit-driven |

| Comparing multiple lenders | Online lender + bank/credit union | Get 2–3 pre-approvals, use the best rate at the dealer |

| Self-employed or irregular income | Credit union | Often more flexible underwriting than traditional banks |

| Lower credit score | Dealer financing (captive/subprime lender) | Dealers have relationships with more lenders across the credit spectrum |

The Dealer Markup: What It Is and How It Affects You

The dealer markup — sometimes called dealer reserve — is the difference between the rate the lender offers the dealer and the rate the dealer presents to you.

Example:

- Lender offers dealer a buy rate of 6.5% APR

- Dealer presents you a rate of 8.0% APR

- The dealer earns the difference over the life of the loan

On a $28,000 loan over 60 months, that 1.5% markup adds roughly $1,100 in extra interest — money that goes to the dealer, not the lender.

The FTC has noted that consumers are often unaware of this markup because dealers are not required to disclose the buy rate. This is one reason the FTC advises buyers to shop for financing before visiting a dealer.

You can reduce or eliminate the markup by:

- Coming in with a competing pre-approval

- Asking the dealer directly what rate they are offering and whether it can be lowered

- Focusing on total cost, not monthly payment — a dealer can lower the monthly payment by extending the term while keeping a high rate

How Much Does the Dealer Markup Actually Cost? Real Numbers

Based on a $28,000 loan over 60 months:

| APR | Who Typically Offers This | Monthly Payment | Total Interest | Extra Cost vs 6.5% |

| 6.5% | Credit union / bank pre-approval | ~$547 | ~$4,820 | — baseline — |

| 7.5% | Bank or dealer (+1% markup) | ~$560 | ~$5,600 | +$780 |

| 8.5% | Dealer with typical markup | ~$573 | ~$6,380 | +$1,560 |

| 9.5% | Dealer with higher markup | ~$586 | ~$7,160 | +$2,340 |

These are illustrative estimates based on standard loan calculations. Your actual rate depends on your credit score, lender, and market conditions at the time of application. Always confirm your exact rate and total cost with your lender before signing.

The monthly payment difference between 6.5% and 8.5% is only $26. But over 60 months, you pay $1,560 more — most buyers do not notice this when focusing only on the monthly figure.

How to Use Both to Get the Best Deal

The smartest approach is to use dealer and bank financing together:

- Get pre-approved before you shop. Apply to your bank, credit union, or an online lender. Understand the difference between prequalification and preapproval before you start — prequalification is a soft check with no impact on your credit score, while preapproval is a firm offer based on a hard inquiry.

- Know your rate going in. Your pre-approval gives you a benchmark. You are not guessing what a fair rate looks like.

- Visit the dealer. Once you agree on the car price, ask the dealer what financing they can offer. Give them a chance to beat your pre-approval.

- Compare total cost, not monthly payment. APR (Annual Percentage Rate) is the true annual cost of the loan including fees. A lower monthly payment achieved by extending the term can cost you far more overall — always compare the total amount repayable, not just the monthly figure.

- Choose the better offer. If the dealer beats your rate on the same term with the same total cost — use dealer financing. If not — use your pre-approval.

For a full breakdown of how auto loans work from start to finish, see our complete US auto loan guide.

Step-by-Step: Best Process for Getting a Car Loan

- Check your credit report — free at AnnualCreditReport.com. Dispute any errors before applying.

- Know your budget — decide your maximum monthly payment and total loan amount.

- Apply for pre-approval — use your bank, a credit union, or an online lender. Aim for at least two offers to compare.

- Shop for the car — with your budget and pre-approval confirmed, negotiate the car price first, separately from financing.

- Ask the dealer for their best rate — show your pre-approval and ask if they can beat it.

- Compare total cost — same loan amount, compare total interest paid and total repayable, not just monthly payment.

- Choose and sign — read the full agreement before signing. Confirm the rate, term, total amount, and any fees match what was discussed.

Questions to Ask Before You Sign

Use this checklist when comparing financing offers. Do not sign until you have answers to all of these.

Ask your bank, credit union, or online lender:

- What is my pre-approved APR?

- What is the loan term (number of months)?

- What is the total amount I will repay, including all interest?

- Are there any origination fees, prepayment penalties, or other fees?

- How long is this pre-approval valid?

Ask the dealer:

- What APR are you offering me?

- Which lender is funding this loan?

- What is the total amount I will repay over the full term?

- Is this rate the lender’s base rate, or has a markup been added?

- Are there any dealer fees included in this financing?

- Can you match or beat my pre-approval rate of [X]%?

Before you sign:

- Does the contract match what was discussed verbally?

- Is the rate, term, total cost, and any fees correct in writing?

- Have you read the full agreement — not just the payment summary page?

Frequently Asked Questions

Is dealer financing always more expensive than bank financing?

Not always. Manufacturer-subsidised 0% APR deals through dealers can be better than any bank rate. But for standard dealer financing — where the dealer arranges a loan through a third-party lender — there is often a markup above the lender’s base rate. Getting a bank or credit union pre-approval first gives you a benchmark to judge whether the dealer’s offer is competitive.

Does applying for a pre-approval hurt my credit score?

A pre-approval involves a hard credit inquiry, which may temporarily lower your score by a few points. However, if you apply to multiple auto lenders within a short period — typically 14 to 45 days — credit scoring models often count them as a single inquiry. Shopping around does not damage your credit the way applying for multiple credit cards would.

Can I negotiate the interest rate at a dealership?

Yes. The rate a dealer presents is not always their final offer. Having a competing pre-approval from a bank or credit union gives you the leverage to ask the dealer to match or beat it. Some buyers negotiate the rate down; others negotiate the car price down and accept the rate. Focus on the total cost, not just one number.

What is the difference between a captive lender and a third-party lender?

A captive lender is a finance company owned by the manufacturer — for example, Ford Motor Credit or Toyota Financial Services. They fund the manufacturer’s promotional financing deals, including 0% APR offers. A third-party lender is an independent bank or finance company that the dealer submits applications to. Captive lender rates may be subsidised; third-party lender rates often include a dealer markup.

Should I tell the dealer I have a pre-approval?

Generally, yes — but do it after you have agreed on the car price. Dealers sometimes adjust the car price upward if they know you are not using their financing, since they lose the financing profit. Agree on the car price first, then reveal your pre-approval when discussing payment.

Where can I check if a dealer’s financing offer is reasonable?

Compare the rate against published average auto loan rates. The Federal Reserve publishes consumer credit data including average auto loan rates at federalreserve.gov. You can also check rates directly with your bank, credit union, or lender comparison tools.

Sources

- FTC — Financing or Leasing a Car

- FTC — Financing a Car: Consumer Tips

- CFPB — Auto Loan Shopping Guide (PDF)

- Federal Reserve — Consumer Credit (G.19 Release)

- AnnualCreditReport.com — Free Credit Reports

Disclaimer:

MoneyMentorDesk.com is not a lender, financial adviser, or credit broker. This article is for educational purposes only. Information is based on publicly available sources and is intended to help readers understand their options. Always read the full loan agreement and confirm terms with your lender before signing. MoneyMentorDesk does not guarantee the accuracy of third-party rates or lender terms, which change frequently.