Can You Trade In a Financed Car? (Negative Equity Explained)

Yes, you can trade in a financed car, even if you still owe money on it. Having an active auto loan does not block a trade-in. What decides whether the trade helps or hurts you is the gap between two numbers: your payoff amount (the total needed today to fully settle the loan) and your car’s current market value (what a dealer or buyer will actually pay).

If your car is worth more than the payoff, you have positive equity. If it’s worth less, you have negative equity. This guide explains both in plain English, walks through the dealer payoff process step by step, and shows how trading in a financed car works in the United States and the United Kingdom.

Key takeaways

- You can trade in a financed car at any point in the loan — the dealer pays your lender directly.

- Your payoff amount is not the same as your statement balance; it includes interest accrued up to the payoff date and possible fees.

- Positive equity lowers the cost of your next car. Negative equity must be paid in cash or rolled into the new loan, which makes the new loan more expensive (Consumer Financial Protection Bureau).

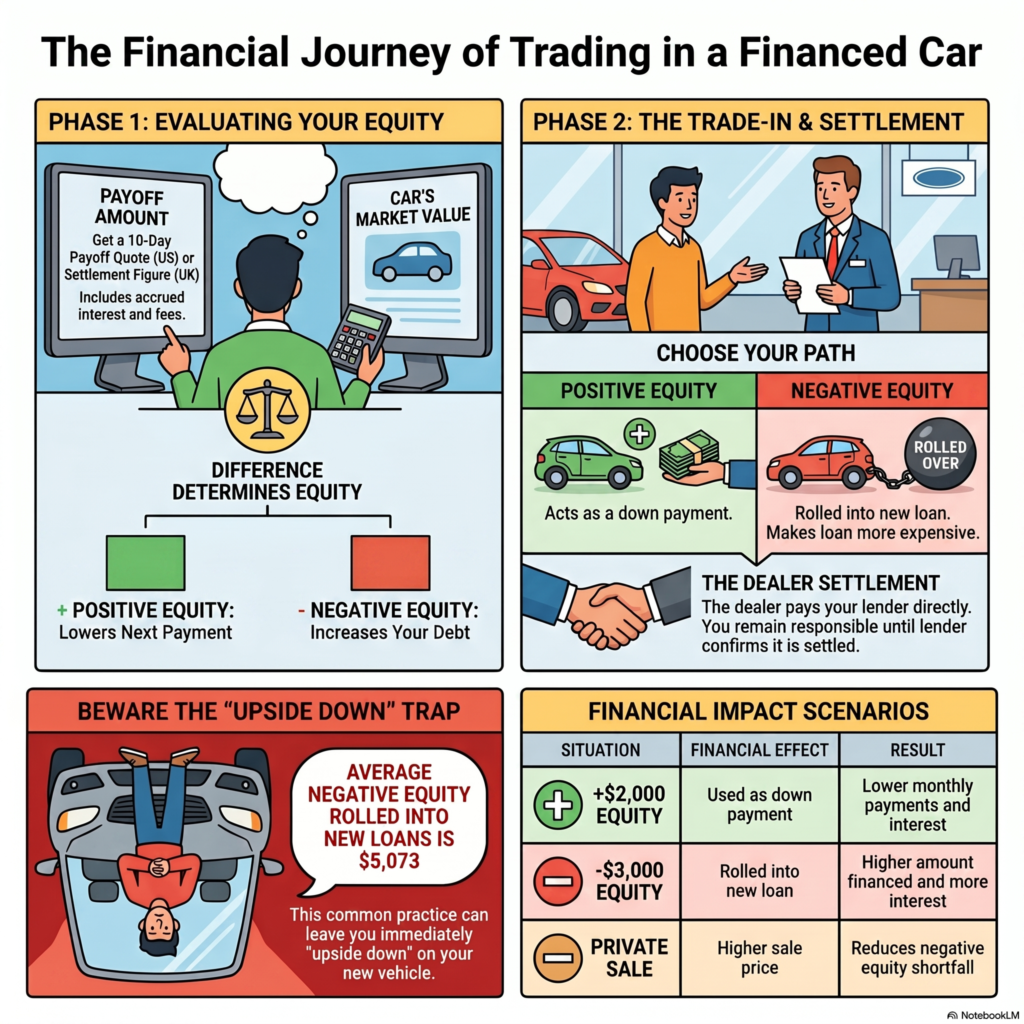

- Always get a written 10-day payoff quote (US) or settlement figure (UK) before you agree to anything.

- Rolling negative equity into a long, high-APR loan is usually the most expensive outcome.

Can You Trade in a Car That’s Still on Finance?

Yes. You can trade in a car that’s still on finance, whether you have a US auto loan or a UK HP or PCP agreement. The dealer does not erase your loan — they pay off your lender on your behalf and then take ownership of the car. Your only job is to know your numbers before you walk in.

Many people feel stuck here. Trading in is possible, but possible doesn’t always mean wise. The right choice depends on your equity, your interest rate, how much time is left on the loan, and your future plans. Knowing this before you visit a dealer protects you from agreeing to terms that quietly add long-term debt.

Payoff Amount vs Car Value: Why It Decides Everything

The single most important comparison is your payoff amount versus your car’s market value. The difference between these two numbers is your equity, and equity decides whether a trade-in saves you money or costs you more. Get both numbers in writing before you negotiate.

A real-life dilemma: You want a safer, more reliable car for your family, but you still owe $14,500 on your current car. A dealer offers $12,000 for it. You can trade today, but doing so leaves $2,500 that must be paid in cash or added to a new loan. (Figures are simplified examples, not real offers.)

How to Get the Right Payoff Amount (10-Day Payoff Quote)

Your payoff is not the balance on your last statement. Because interest can build up daily, the real figure to settle your loan is usually a little higher. Always ask your lender for it in writing.

A safe payoff request includes:

- Request a written 10-day payoff quote from your lender.

- Ask whether there are any prepayment penalties or early-payoff fees.

- Confirm whether your GAP coverage will be cancelled after payoff, and whether you are owed a refund.

Double-check the account number and payoff figure for accuracy. If the quote expires before the dealer sends payment, accrued daily interest can leave a small residual balance on your old account that you are still responsible for.

US “Payoff Quote” vs UK “Settlement Figure”

The idea is the same in both countries, but the wording differs. In the US you request a payoff amount or 10-day payoff quote. In the UK you request a settlement figure from your finance company — the amount needed to clear a Hire Purchase (HP) or Personal Contract Purchase (PCP) agreement early.

| Term | United States | United Kingdom |

| What you ask for | Payoff amount / 10-day payoff quote | Settlement figure |

| Common finance types | Auto loan | HP, PCP |

| Who owns the car during finance | You (lender holds a lien) | Finance company, until the agreement is settled |

| What the figure includes | Remaining balance + accrued interest + any fees | Remaining balance + interest to the settlement date + any fees; for PCP, also the final balloon payment |

In the UK, a settlement figure is the total amount needed to repay your car finance early and close the agreement. With HP and PCP, the finance company is the legal owner of the car, so you cannot legally sell, part-exchange, or trade in the vehicle until the agreement is settled (MoneyHelper; UK industry guidance). For PCP, the settlement figure usually includes the final “balloon” payment if you want to own the car. Lenders must provide a settlement figure on request, and the quote is commonly valid for a set period (often around 28 days), after which a fresh figure is needed. [VERIFY SOURCE: confirm exact validity window with your lender, as it varies]

Positive Equity vs Negative Equity (With Real Math)

Whether trading a financed car helps or hurts you depends almost entirely on equity. Equity is simply the gap between what your car is worth and what you still owe. The formula is the same everywhere:

Car’s Market Value − Payoff Amount = Equity

- Positive equity (+): the trade can lower the cost of your next car.

- Negative equity (−): you still owe money after the trade, and that amount must be paid in cash or added to the new loan.

The examples below are simplified for learning and do not represent real loan offers.

Scenario A — Positive Equity

- Payoff amount: $13,000

- Trade value: $15,000

- Equity: +$2,000

Result: the $2,000 can act as a down payment on the next car, often lowering both the monthly payment and total interest.

Scenario B — Negative Equity Rolled Into a New Loan

- Payoff amount: $18,000

- Trade value: $15,000

- Equity: −$3,000

If that $3,000 is added to a new loan, you pay interest on it for the full term. The Consumer Financial Protection Bureau warns that rolling a negative balance into a new auto loan makes that new loan more expensive, and you can immediately be “upside down” again. The “convenience” of trading can make the next car noticeably more expensive over time. The exact added interest and payment increase depend on your APR and term.

For context on how common and costly this is: the CFPB found that for vehicle loans originated between 2018 and 2022, about 11.6% included financed negative equity, and the average negative equity rolled into new-vehicle loans was about $5,073 (about $3,284 for used vehicles) (CFPB, “Negative Equity in Auto Lending,” June 2024).

Scenario C — Private Sale Option

- Private sale price: $16,500

- Payoff amount: $18,000

- Gap: −$1,500 instead of −$3,000

A private sale takes more effort, but it often reduces negative equity compared with a dealer trade-in.

| Situation | Financial effect |

| +$2,000 equity | Lower payment and less interest |

| −$3,000 rolled into a new loan | Higher amount financed and more total interest |

| Private sale | May reduce the shortfall (here, by about $1,500) |

Can You Trade in a Financed Car with Negative Equity?

Yes, you can trade in a financed car with negative equity, but it is the situation that needs the most caution. With negative equity you owe more than the car is worth, so the shortfall must be paid in cash or rolled into your next loan. Rolling it over increases the amount you finance and usually raises your total interest.

The Federal Trade Commission warns that some dealers advertise they will “pay off your loan no matter how much you owe,” but may simply roll the negative equity into your new loan or take it from your down payment — so you still end up paying it. If a dealer says they will absorb the negative equity themselves but actually rolls it into your financing, that is illegal and can be reported to the FTC.

Be especially careful when:

- You plan to roll negative equity into a new loan with a long term (such as 72–84 months).

- You would move from a lower APR to a higher APR.

- You would lose existing GAP coverage.

- The decision is based only on a “lower monthly payment” rather than the total cost.

Combining a high APR with rolled-over negative equity is generally the most expensive scenario of all.

How the Dealer Payoff Process Works (Step by Step)

When you trade in a financed car, the dealer pays your lender on your behalf and then takes ownership of the vehicle. The dealer does not cancel your debt — they settle it with your lender, and any positive or negative equity is applied to your new deal.

The dealer payoff process usually works like this:

- The dealer requests your payoff amount from your lender using the VIN and your authorization.

- The lender issues a written payoff quote.

- The dealer sends payment directly to the lender.

- The lender releases the lien and sends the title to the dealer or the state. (In the UK, the finance company confirms the agreement is settled and ownership transfers.)

- Any positive or negative equity is applied to your new purchase.

Title/Lien Release & Timing Risks

Payoff processing and title release can take time, and timelines vary by lender and location. If the payoff figure changes because of daily interest, you may owe a small balance after the trade. Keep making your normal payments until the lender confirms the loan is fully closed, so you avoid a late mark on your credit. A few weeks after the deal, check that the old loan shows as paid and that you have written confirmation it is settled.

If you make reasonable efforts and your old loan still has not been paid off, the CFPB notes you can contact your new lender, submit a complaint to the CFPB or the FTC, and contact your state attorney general.

CarMax & Carvana vs Traditional Dealerships

| Feature | CarMax / Carvana | Local dealership |

| Payoff handling | Standardized, online verification | Varies by dealer |

| Offer transparency | Fixed offers | Often negotiable |

| Timing | Usually, faster | Depends on lender |

| Trade with purchase | Optional | Often bundled |

Both pay your lender directly, but large national buyers often use more automated processes. (CarMax and Carvana operate in the US; UK readers should compare equivalent online buyers and dealers.) [VERIFY SOURCE: confirm current operating details before relying on them]

When Trading in a Financed Car Makes Sense

Trading in a financed car can be a smart move when the numbers and your needs line up. The clearest sign is positive equity, but safety and reliability also matter. A trade tends to make sense when:

- You have positive equity that reduces the cost of the next car.

- Your current car has high repair costs or real safety concerns.

- You can move to a loan with an equal or lower APR and an affordable payment.

- You understand the total cost, not just the monthly payment.

When Trading in Is a Bad Idea (Warning Signs)

Trading in can feel convenient, but convenience becomes expensive when the numbers work against you. Slow down and compare alternatives if you see several of these warning signs:

- High-APR rollover — financing old negative equity into a more expensive loan raises both payment and total interest. The CFPB found consumers who financed negative equity had average monthly payments noticeably higher than those with no trade-in.

- The 84-month trap — a very long term lowers the payment but usually means far more interest and longer time in negative equity.

- Losing GAP coverage — trading can end existing GAP coverage. The CFPB notes you may be entitled to a refund if you sell, refinance, or prepay your loan, but refunds are not always automatic, so confirm it.

- Early payoff penalties — some loans or agreements include fees or early-settlement charges that reduce the benefit of trading early.

- Taxes and registration costs — title, registration, and documentation fees can erase a thin equity advantage. [VERIFY SOURCE: tax treatment varies by US state and by UK rules]

- Manufacturer incentive traps — a rebate may come with a higher APR, a reduced trade value, or offers that can’t be combined. [VERIFY SOURCE: terms vary by offer]

If several of these appear in the same deal, a private sale, refinancing, or keeping the car longer may be the lower-risk choice.

Trade In vs Refinance vs Private Sale

Choosing the right path can save you a lot of money. Compare them on total cost and risk, not just on how quick or easy each one feels.

| Option | Best when | Main risks |

| Trade-in | You have positive equity or need a safer car quickly | Dealer may undervalue the car; negative-equity rollover |

| Refinance | You can lower your APR without extending the term | Fees may offset the savings |

| Private sale | Market value is higher than the dealer’s offer | More time and paperwork; you must coordinate payoff with the lender |

Refinancing is often the better move if your credit score has improved, current rates are lower than your loan APR, or you want to keep the car but reduce the payment. [VERIFY SOURCE: confirm current rates and fees for your situation]

Fees, Taxes & GAP Insurance to Check First

Before you sign, look past the trade value and monthly payment. Several costs can quietly reduce or erase your equity, so confirm each one in writing.

- GAP coverage: the CFPB defines GAP as an optional product intended to cover the difference between what you owe on your auto loan and what your insurance pays if the car is stolen or totaled. Trading usually ends existing GAP, refunds are not always automatic, and a new loan may need new GAP at a different price. GAP is optional and you can decline it.

- Payoff and prepayment charges: daily interest adjustments, lien-release fees, or prepayment/early-settlement charges can reduce thin positive equity.

- Taxes and registration: sales tax on the replacement vehicle, documentation fees, and title or registration costs vary by US state and by UK rules. [VERIFY SOURCE]

- Dealer markup: trade value can be lowered to fund a “discount,” and add-ons can inflate the loan balance. Read the contract and disclosures carefully before signing (CFPB).

How a Trade-In Affects Your Credit Score

Trading in a financed car can affect your credit, but the impact is usually manageable when it’s handled well. A new loan typically triggers a hard inquiry, and closing the old loan slightly changes your credit mix. On-time payments are generally neutral to positive over time. [VERIFY SOURCE: exact scoring effects vary by model]

Helpful habits:

- Complete the trade and new financing within a short shopping window. Many credit-scoring models may treat several auto-loan inquiries in a short period as one event, though timing rules vary.

- Avoid opening other new credit accounts at the same time.

- Check your report to confirm the old loan shows as paid or closed.

Frequently Asked Questions

Can you trade in a financed car?

Yes. An active loan does not prevent a trade-in. The dealer requests your payoff amount, pays your lender directly, takes ownership of the car, and applies any positive or negative equity to your next deal.

Can you trade in a car that’s still on finance in the UK?

Yes, but request a settlement figure from your finance company first. With HP or PCP, the finance company is the legal owner of the car until the agreement is settled, so you cannot legally sell or part-exchange it until then (MoneyHelper).

What is a 10-day payoff quote?

A 10-day payoff quote is a written figure from your lender showing the exact amount to fully close your loan, typically valid for a short window. Because it includes interest accrued up to the payoff date, it is often slightly higher than your statement balance.

What happens if I have negative equity?

If your payoff amount is higher than your trade value, the difference must be paid in cash or added to the new loan. The CFPB warns that rolling it into a new loan makes that loan more expensive and can leave you upside down again.

Can I trade in a car with positive equity?

Yes, and it usually helps. Positive equity can be used as a down payment on your next car, which lowers the amount you finance, your monthly payment, and the total interest you pay.

How does the dealer payoff process work?

The dealer requests your payoff using the VIN and your authorization, pays the lender directly, and the lender releases the lien and title. Any positive or negative equity is then applied to your new purchase.

Can I sell a financed car privately instead of trading it in?

Yes. You coordinate with your lender so the title or finance is released after payoff. A private sale can reduce negative equity because buyers often pay more than dealers, but it takes more time and paperwork. In the UK, you must pay the settlement figure first because you are not the legal owner until then.

Will trading in a financed car hurt my credit?

There may be a small, temporary dip from a hard inquiry and the change in your loan accounts. Credit usually recovers when you keep payments on the new loan on time and the old loan is properly closed. [VERIFY SOURCE: exact effects vary by scoring model]

About the Author & Sources

Author: Nimra Saleem, founder of MoneyMentorDesk, an educational website that simplifies personal finance using independent research and publicly available information.

Sources used (verified, official where possible):

- US — Consumer Financial Protection Bureau (CFPB), Should I trade in my car if it’s not paid off?

- US — Consumer Financial Protection Bureau (CFPB), What is Guaranteed Asset Protection (GAP) insurance?

- US — Consumer Financial Protection Bureau (CFPB), Negative Equity in Auto Lending” report, June 2024 — files.

- US — Federal Trade Commission (FTC), Auto Trade-Ins and Negative Equity

- UK — MoneyHelper, Ending a car finance deal early

—Note: The CFPB negative-equity averages ($5,073 new / $3,284 used) and the 11.6% figure come from the CFPB’s 2018–2022 dataset. Confirm these are still the latest figures before publishing, and link directly to the official pages above.

Educational notice: This article is for educational and informational purposes only and is based on independent research and publicly available information, including guidance from the CFPB, FTC, and MoneyHelper. MoneyMentorDesk does not provide financial, legal, or investment advice. Financing terms, interest rates, taxes, and regulations vary by lender, location, and individual circumstances. Always verify details directly with your lender or a qualified professional before making financial decisions.