can I trade in a financed car even if I still owe money on it?

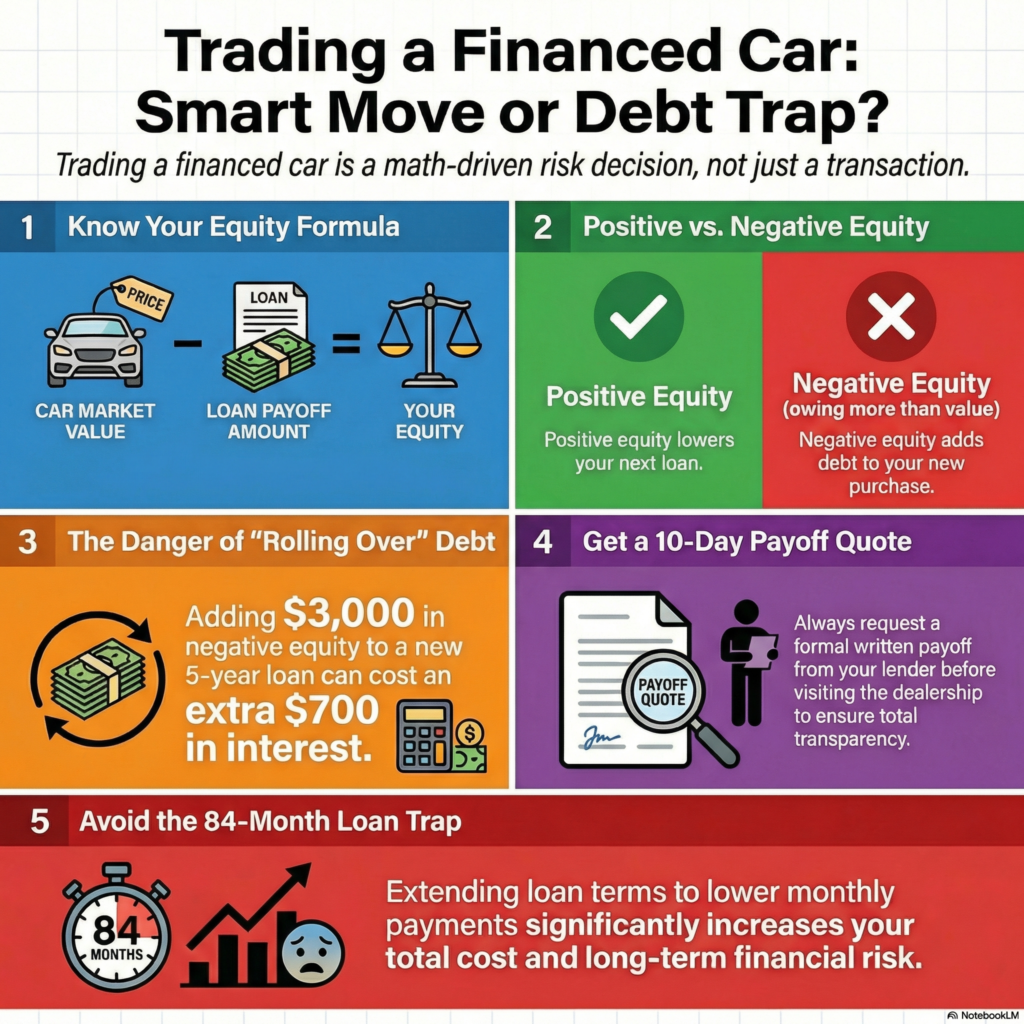

Having an active auto loan does not prevent a trade-in. What matters is the relationship between two numbers:

- Your loan payoff amount – the total needed today to fully settle your loan

- Your car’s current market value – what a dealer or buyer is willing to pay for it

The difference between these numbers determines whether trading in your car will help you financially or create additional debt.

Payoff vs. Value — Why This Matters

- If your car is worth more than the payoff → you have positive equity

- If your car is worth less than the payoff → you have negative equity

Dealerships typically handle the loan payoff directly with your lender, but any shortfall or surplus becomes part of your next financial decision. Understanding this before visiting a dealer protects you from agreeing to terms that may not be in your best interest.

A Real-Life Dilemma

Imagine this situation:

You want a safer, more reliable vehicle for your family, but you still owe $14,500 on your current car. A dealer offers $12,000 for it. You can trade today — but doing so would leave $2,500 of debt that must be paid or added to a new loan.

This is where many people feel stuck. Trading in is possible, but possible doesn’t always mean wise. The right choice depends on your budget, interest rate, remaining loan term, and future plans.

When Trading a Financed Car Can Make Sense

Trading may be reasonable when:

- You have positive equity that can reduce the cost of the next vehicle

- Your current car has high repair costs or safety concerns

- You can move to a loan with a lower interest rate and affordable payment

- You understand the total cost, not just the monthly payment

When Caution Is Needed

Be careful if:

- You have negative equity and plan to roll it into a new loan

- The new loan term becomes very long (72–84 months)

- You would lose existing GAP insurance protection

- The decision is based only on “lower monthly payment” rather than total cost

Educational Decision Framework: Understanding Trade-In Risks

Trading a financed car is not automatically good or bad — it’s a math and risk decision. Before stepping into a dealership, answer these five questions. These questions are designed to help readers better understand potential financial outcomes or quietly adds long-term debt.

Do You Have Positive or Negative Equity?

Equity Formula

Car’s Market Value – Loan Payoff = Equity

- Positive equity (+): The trade can lower the cost of your next car.

- Negative equity (–): You still owe money after the trade. That amount must be paid in cash or added to the new loan.

How Does Your APR Compare?

Compare:

- Current loan interest rate

- Interest rate you qualify for today

- Length of the new loan

Red flags

- Moving from a low APR to a higher APR

- Extending the term to 72–84 months

- Lower payment but higher total cost

How Much Time Is Left on Your Loan?

- Near the end of the loan → most payments now reduce principal

- Early in the loan → payments are mostly interest

Do You Have GAP Insurance?

- GAP insurance covers the difference between loan balance and car value if the car is totaled.

- Trading in can cancel existing GAP coverage.

- Rolling negative equity without GAP can leave you exposed if an accident happens.

Are There Prepayment or Exit Costs?

Some loans include:

- Prepayment penalties

- Deferred interest charges

- Fees for early payoff

Simple Decision Flow

Use this path before agreeing to any deal:

1) Do you have positive equity?

→ YES: Trading can be reasonable → compare offers

→ NO: Go to step 2

2) Can refinancing lower your APR without extending term?

→ YES: Refinancing is one option some consumers compare, but outcomes vary based on rates, fees, and loan terms.

→ NO: Go to step 3

3) Would a private sale cover the payoff?

→ YES: Consider private sale first

→ NO: Go to step 4

4) Is the trade for safety/repair necessity?

→ YES: Trade with strict budget limits

→ NO: In many situations, keeping the current vehicle can be the lower-cost option, depending on interest rates, fees, and personal financial circumstances.

Lower-Risk vs Higher-Risk Trade-In Scenarios

Trading is often SMART when:

- You have positive equity

- New APR is equal or lower

- Term is not extended dramatically

- Vehicle has high repair or safety concerns

- You can keep or replace GAP protection

Trading may involve higher financial risk when:

- Negative equity is rolled into a long loan

- Payment drops but total cost rises

- GAP coverage is lost

- Decision is based on pressure or “today only” offers

Consumer-First Reminder

A dealership can legally process a trade even if it harms your finances. Their approval is not the same as financial suitability. Take time to:

- Request the written payoff

- Compare at least two offers

- Review total loan cost

- Consider refinance or private sale

The goal is not just to change cars — it’s to improve your financial position, not trap you in more debt.

Positive vs Negative Equity — With Real Math

Whether trading a financed car helps or hurts you depends almost entirely on equity. Equity is simply the gap between what your car is worth and what you still owe.

How to Get the RIGHT Payoff Amount

Your payoff is not the same as the balance shown on your last statement. It should include:

- Remaining principal

- Accrued interest up to today

- Possible lender fees

Safe steps

- Request a written “10-day payoff quote” from your lender

- Ask if there are prepayment penalties

- Confirm whether GAP insurance will be cancelled after payoff

Real-World Scenarios (Educational Examples)

These examples show how equity affects the next loan. Actual payments vary by credit profile and lender.

Scenario A – Positive Equity

- Loan payoff: $13,000

- Trade value: $15,000

- Equity: +$2,000

Result:

The $2,000 can reduce the new car price or act as a down payment, often lowering monthly payments and total interest.

These numbers are simplified educational examples and do not represent real loan offers.

Scenario B – Negative Equity Rolled into New Loan

- Loan payoff: $18,000

- Trade value: $15,000

- Equity: –$3,000

If that $3,000 is added to a new 60-month loan at 8% APR:

- Added interest ≈ $650–$700

- Payment increase ≈ $55–$65/month

What this means:

The “convenience” of trading can make the next car significantly more expensive over time.

These numbers are simplified educational examples and do not represent real loan offers.

Scenario C – Private Sale Option

- Private sale price: $16,500

- Payoff: $18,000

Gap: –$1,500 instead of –$3,000

→ Potential savings compared with dealer trade

Private sales take more effort, but they often reduce negative equity.

These numbers are simplified educational examples and do not represent real loan offers.

Quick Comparison

| Situation | Financial Effect |

| +$2,000 equity | Lower payment & less interest |

| –$3,000 rolled | Payment ↑ about $60/month + extra interest |

| Private sale | May reduce debt by ~$1,500 |

Why APR Changes Matter

Equity isn’t the only factor. The interest rate on the new loan can magnify costs.

- Moving from 4% → 9% APR can add thousands in interest

- Extending from 60 → 84 months lowers payments but increases total cost

- Combining high APR + negative equity is the most expensive scenario

Consumer tip: Always compare:

- New APR

- Total interest over the full term

- Total amount financed not just the monthly payment.

Common Misunderstandings

- “The dealer will pay off my loan, so I’m free.”

The loan is paid, but negative equity can reappear inside the new loan. - “Lower payment = better deal.”

Longer terms often hide higher total costs. - “My statement balance is the payoff.”

Payoff usually differs due to daily interest.

How Dealers ACTUALLY Pay Off Your Loan

When you trade in a financed car, the dealer does not erase your loan — they pay your lender on your behalf and then take ownership of the vehicle. Here’s how it works in practice.

Dealer Payoff Process (Step by Step)

- Dealer requests payoff from your lender using the VIN and your authorization.

- Written payoff quote is issued (usually valid 7–10 days).

- Dealer sends payment directly to the lender.

- Lender releases the lien and sends the title to the dealer or state.

- Any positive or negative equity is applied to your new deal.

Title Release & Timing Risks

- Payoff processing and title release timelines vary widely by lender and state, ranging from several days to a few weeks.

- If the payoff amount changes due to daily interest, you may owe a small balance after the trade.

- Keep making payments until the lender confirms the loan is fully closed to avoid late marks.

CarMax/Carvana vs Traditional Dealerships

| Feature | CarMax/Carvana | Local Dealership |

| Payoff handling | Standardized, online verification | Varies by dealer |

| Offer transparency | Fixed offers | Often negotiable |

| Timing | Usually, faster | Depends on lender |

| Trade with purchase | Optional | Typically bundled |

Both methods pay the lender directly, but large buyers often have more automated processes.

State & Lender Differences to Know

- Some states require in-person title notarization.

- Credit unions may need member authorization forms.

- Certain lenders charge prepayment or processing fees.

- GAP insurance may cancel automatically after payoff.

When Trading Is a BAD Idea

Trading in a financed car may feel convenient, but convenience can become expensive when the numbers are working against you. In some situations, a trade-in solves a short-term problem while creating a much larger long-term cost. The following warning signs usually mean you should slow down, compare alternatives, and review the full deal carefully before signing.

1) High APR Rollover

If you already have negative equity and the new loan comes with a high APR, the cost of trading can rise quickly. You are not only financing the next vehicle, but also carrying old debt into a more expensive loan. This often increases both the monthly payment and the total interest paid over time. A trade in this situation may only make sense if the current vehicle has serious repair, reliability, or safety problems that justify the higher cost.

2) The 84-Month Trap

A very long loan term can make a deal look affordable because the monthly payment appears lower. However, stretching a loan to 72 or 84 months usually means paying much more interest overall. It can also keep you in negative equity for longer because the car may depreciate faster than the loan balance falls. If a trade only works because the term becomes extremely long, that is a major warning sign.

3) Losing GAP Insurance

GAP insurance can protect you if your car is totaled while the loan balance is higher than the vehicle’s value. When you trade in a car, existing GAP coverage may end, and any refund or cancellation process can vary. If negative equity is being rolled into the next loan and new GAP coverage is not added, you may be exposed to a larger financial loss after an accident. This risk should be reviewed before finalizing the deal.

4) Early Payoff Penalties

Some loans include fees, deferred charges, or payoff-related costs that reduce the benefit of trading in early. Even a small penalty can weaken positive equity or make negative equity worse. Before moving forward, it is important to request a written payoff quote and confirm whether any penalties or fees apply.

5) Taxes & Registration Costs

Many buyers focus only on trade value and monthly payment, but the full transaction cost can be higher once taxes, title charges, registration fees, and dealer documentation fees are added. In some cases, these extra costs reduce the financial benefit of changing vehicles. A trade should be evaluated using the total out-of-pocket and financed cost, not just the advertised deal terms.

6) Manufacturer Incentive Traps

Promotional rebates and special offers can make a trade-in look attractive, but the real value may not always be as strong as it seems. A dealer may reduce the trade-in value, increase the APR, or limit which incentives can be combined. As a result, a discount on paper may not actually improve the full deal. Always separate the new car price, trade value, loan terms, and add-ons before deciding.

If several of these warning signs appear in the same deal, trading in the car may not be the best financial move right now. In that case, comparing a private sale, refinancing, or simply keeping the current car longer may be the lower-risk option.

Trade vs Refinance vs Private Sale

Choosing the right path can save thousands. Here’s a clear comparison based on total cost and risk.

Side-by-Side Comparison

| Option | Best When | Main Risks |

| Trade-In | You have positive equity or need a safer car quickly | Dealer may undervalue trade; negative equity rollover |

| Refinance | APR can be lowered without extending term | Fees may offset savings |

| Private Sale | Market value is higher than dealer offer | More time and paperwork |

When Refinance Usually Wins

Refinancing is often the better move if:

- Your credit score has improved

- Current rates are lower than your loan APR

- You want to keep the car but reduce payments

- You have negative equity and want to avoid rollover

Rolling Equity into a Lease

- Positive equity can lower lease payments

- Negative equity added to a lease often creates very expensive monthly costs

- If the leased car is totaled, you may still owe the rolled amount

Manufacturer Incentives – Read the Fine Print

- Rebates may require financing at a higher APR

- Trade value can be quietly reduced to fund the discount

- Cash incentives and low-APR offers are often not combinable

GAP Insurance, Fees & Hidden Costs

GAP After Trade

- Trading usually cancels existing GAP

- Refunds are not automatic with every lender

- A new loan may require new GAP at a different price

Prepayment & Payoff Charges

Possible costs include:

- Prepayment penalties

- Daily interest adjustments

- Lien release or processing fees

These can erase small amounts of positive equity.

Taxes You May Not Expect

- Sales tax on the replacement vehicle

- Reduced tax credit if trade value is low

- Documentation and title fees

Dealer Markup Realities

- Trade value may be lowered to offset discounts

- Financing APR can include dealer reserve

- Add-ons (warranty, protection plans) inflate loan balance

Registration Transfer

- New plates vs transfer fees

- Inspection requirements

- State-specific title timelines that can delay payoff

Common Sales Practices to Understand

5 Common Tactics to Watch For

- Payment Focus – showing only monthly payment, not total cost

- Bundling – mixing trade value with new car price

- Rebate Swap – lowering trade to fund a “discount”

- Rate Bump – higher APR to compensate the dealer

- Urgency Pressure – “today only” approval

Step-by-Step Checklist

Use this checklist before and after visiting any dealer to protect your finances.

Before You Agree to a Trade

- Get a written payoff letter (10-day payoff quote) from your lender

- Check GAP insurance status – refund, transfer, or new policy needed

- Compare at least 3 offers (dealer, CarMax/Carvana, private estimate)

- Know your car’s fair value using multiple sources

- Confirm prepayment penalties or fees

During the Deal

- Ask for an itemized breakdown (price, trade value, taxes, APR, add-ons)

- Keep trade value, vehicle price, and financing separate

- Avoid loans that require 84-month terms to be affordable

- Request proof of the exact payoff amount applied

After Signing

- Verify lender release and loan closure within 2–3 weeks

- Continue making payments until payoff is confirmed

- Keep copies of payoff receipt and title transfer

- Confirm any GAP refund was processed

Credit Score Impact

Trading a financed car can affect credit, but the impact is usually manageable when handled correctly.

Hard Inquiry

- A new auto loan typically triggers a hard credit inquiry

- Many credit scoring models may treat multiple auto-loan inquiries made within a short shopping period as a single event, but exact timing varies by scoring system.

Loan Closure

- Paying off the old loan may slightly change your credit mix

- On-time payoff is generally neutral to positive over time

Best Timing Window

- Complete the trade and new financing within a short period

- Avoid opening other credit accounts at the same time

- Monitor your report to confirm the old loan shows paid/closed

This guide was created using independent research from publicly available financial education sources, lender documentation, and general industry practices. Information may change over time, so readers should confirm details directly with lenders or official institutions.

Educational Notice

This article is for educational and informational purposes only and is based on independent research and publicly available information. MoneyMentorDesk does not provide financial, legal, or investment advice. Financing terms, interest rates, and regulations vary by lender, location, and individual circumstances. Always verify details directly with your lender or a qualified professional before making financial decisions.

About Author

Written by Nimra Saleem, founder of MoneyMentorDesk, an educational website that simplifies personal finance topics using independent research and publicly available information.

FAQs

Q1: What happens if I have negative equity?

If your loan payoff is higher than the trade value, the difference must be paid in cash or added to the new loan. Rolling it over increases the amount financed and usually raises total interest.

Q2: Will trading in a financed car hurt my credit?

There may be a small, temporary dip due to a hard inquiry and loan change. Credit often recovers when payments on the new loan remain on time and the old loan is properly closed.

Q3: Can I sell the car privately if I still owe money?

Yes. You must coordinate with the lender to receive the title release after payoff. Private sales can reduce negative equity but require more paperwork and time.

Pingback: What Is a 10-Day Payoff Quote? - moneymentordesk.com

Pingback: Cars With 0% Financing: How It Works and Smarter Alternatives - moneymentordesk.com