Cars with 0% financing allow buyers to purchase a vehicle through monthly payments without paying interest on the loan. These promotions are usually limited to selected models and buyers with strong credit profiles. While 0% APR can reduce total costs, comparing rebates and alternative financing options is important before deciding.

Many buyers search for cars with 0% financing because these promotions can lower total loan costs — but understanding how they work is essential before deciding.

What Does 0% Car Financing Mean?

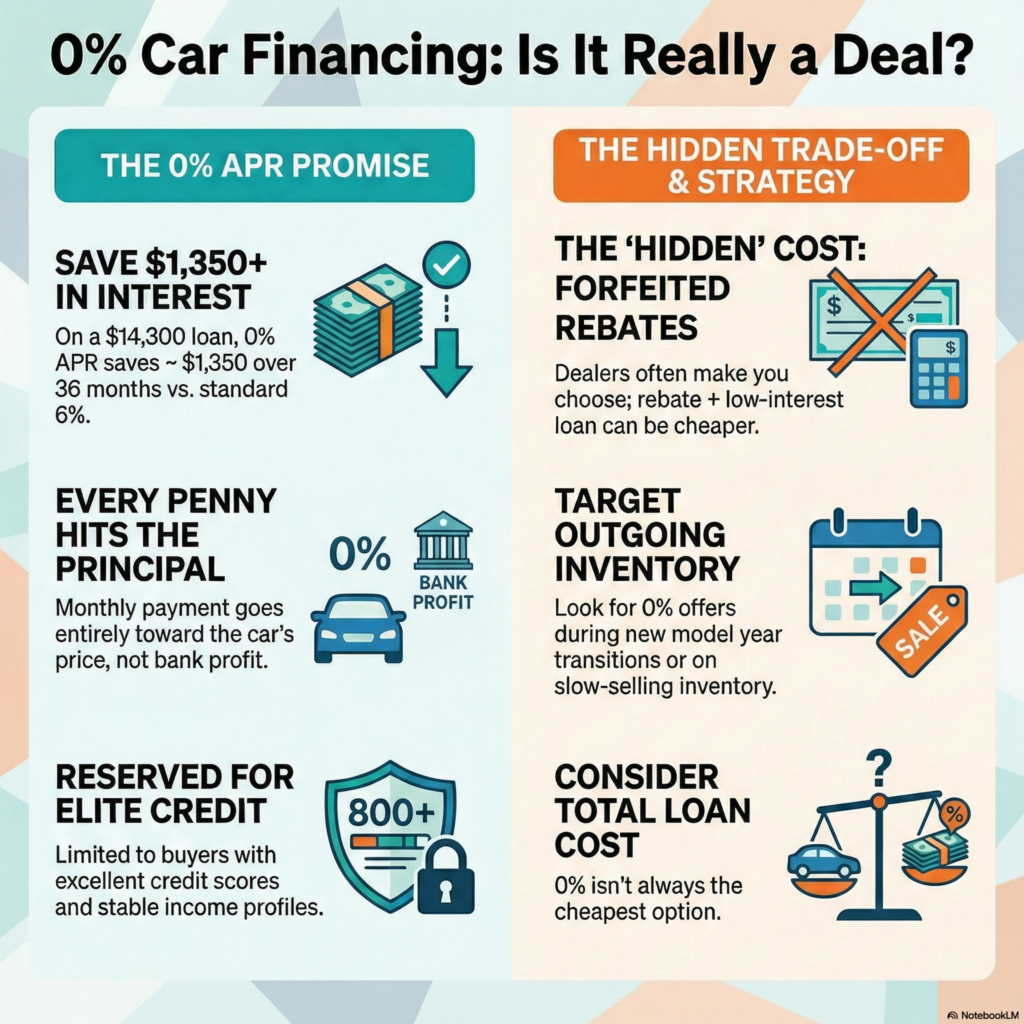

0% car financing is a promotional auto loan where the borrower repays only the vehicle’s price without interest charges. At its core, 0% financing is a type of car loan where the lender, usually the car manufacturer’s financing arm or a partner bank, charges no interest on the borrowed amount.

In a regular car loan, you pay:

- Principal: the actual price of the car.

- Interest: the extra cost of borrowing money, calculated as a percentage rate (for example, 6 percent).

With 0% financing, you still repay the principal over time, but there is no interest at all. Every payment you make goes directly toward the cost of the car.

Example:

• Car price: about $14,300

• Loan term: 36 months

• With 6% interest: Total cost around $15,650

• With 0% interest: Total cost exactly $14,300

How 0% Financing Works

0% financing is often offered as a special promotion by car manufacturers to encourage buyers to purchase certain models. Instead of charging you interest on your loan, the manufacturer covers the cost, making it possible for you to repay only the original price of the car over time.

Here is how it usually works step-by-step:

- You choose a qualifying car

- You apply for financing

- Loan terms are set

- Monthly payments begin

- You complete the payments and own the car

While this sounds straightforward, dealerships may require you to give up certain perks, like cash rebates, in exchange for the 0% rate. This is why comparing the total cost of different financing options is essential before committing.

Which Cars Usually Offer 0% Financing? (UK & US Buyers Guide)

Cars with 0% financing are not available on every model at all times. In both the UK and US markets, manufacturers typically attach 0% APR promotions to specific vehicles based on inventory levels, sales targets, and seasonal campaigns. Instead of looking for a fixed list of cars, it is more helpful to understand which types of vehicles and situations are most likely to include interest-free offers.

New Model Year Transitions

Manufacturers often introduce 0% financing when a newer version of a vehicle is about to launch. Dealers may use promotional APR offers to move remaining stock of the outgoing model year. In the US, this commonly happens toward the end of summer or during year-end sales events, while UK promotions may appear around registration plate change periods.

High-Inventory or Slow-Selling Models

Vehicles that have higher dealership inventory or slower demand are more likely to qualify for promotional financing. This does not mean the car is poor quality — it simply reflects sales strategy. Mid-size sedans, certain compact SUVs, or specific trims sometimes receive 0% offers when manufacturers want to balance stock levels.

Manufacturer-Backed Financing Programs

Most 0% APR deals come through a brand’s captive finance company rather than a traditional bank. In the US, brands such as Ford Credit, Toyota Financial Services, or GM Financial may run promotional financing during clearance periods. In the UK, similar offers can appear through manufacturer finance arms tied to authorised dealerships.

Selected Trims and Limited Eligibility

Even when a manufacturer advertises 0% financing, it may apply only to:

- specific trims or engine options

- shorter loan terms (for example 24–48 months)

- buyers with strong credit profiles

Because of this, two buyers looking at the same car may see different eligibility results depending on credit history and promotion timing.

Regional Availability and Timing

Promotional APR offers change frequently and vary by country, lender, and campaign. Instead of relying on static lists of “current deals,” many buyers in the UK and US check:

- official manufacturer finance pages

- authorised dealership promotions

- trusted automotive marketplaces that show dated offers

Key takeaway: There is no permanent list of cars with 0% financing. Promotions usually rotate between selected models based on inventory, seasonal campaigns, and manufacturer strategy — which is why comparing total costs and reading the full terms is essential before deciding.

Top Categories of Cars That Often Get 0% APR

Manufacturers commonly attach 0% APR financing to outgoing model-year vehicles, selected sedans, compact SUVs, and sometimes electric or hybrid models during promotional campaigns. These offers are usually limited to specific trims or shorter loan terms and vary by region, inventory levels, and buyer eligibility.

Pros and Cons of 0% Financing

| Pros | Cons / Hidden Drawbacks |

| Save money on interest. All payments go toward the car’s price, with no extra interest costs | Strict eligibility requirements. Usually approved only for buyers with excellent credit scores |

| Predictable monthly payments. Easy to budget since the payment amount is fixed and interest free | Limited car selection. Often available only on certain models or trims |

| Faster equity in your car. You own more of your car sooner because you are paying off the principal faster | Higher monthly payments. Shorter loan terms can make payments larger each month |

| Great for short-term loans. Pay off your car quickly without extra costs | Loss of other incentives. You may have to give up cash rebates or discounts |

| Attractive for high-value cars. The bigger the price, the more you save in avoided interest costs | Possible price inflation. Some dealers may factor the free financing into the car’s price, reducing the real benefit |

What Lenders May Consider for 0% Financing

Instead of thinking of 0% financing as something you “apply tricks” to get, it helps to understand the common factors lenders may review when evaluating applications. Requirements vary by country, bank, and promotion, but the following elements are frequently part of the decision process:

- Credit Profile

- Income Stability

- Existing Financial Commitments

- Eligible Vehicles or Promotions

- Timing and Availability

Tip: Applicants are often asked to provide documents such as identity verification or financial records.

How to Calculate Total Car Loan Cost

Total Loan Cost ($) = Monthly Payment × Number of Months + Fees/Add-ons

Example:

$450 × 60 months = $27,000 total paid

If the car price was $24,000 → $3,000 is the borrowing cost

Real-Life Scenarios

To understand how 0% financing works in practice, let’s look at two real-world examples — one where it was the perfect choice and another where a different option worked out better.

Scenario 1: 0% financing saves money

Ahmed wanted to buy a sedan priced at about $14,280 USD. The dealership offered him 0% financing over 36 months with no loss of additional incentives. His credit score was excellent, and he could comfortably afford the higher monthly payments. Since there was no interest, his total cost remained exactly $14,280 USD. Compared to a regular loan at 6 percent interest, he saved about $1,350 USD over three years. For Ahmed, 0% financing resulted in the lower total cost in this example.

Scenario 2: Rebate plus low-interest loan works better

Sara was looking at an SUV priced at about $17,850 USD. She qualified for 0% financing, but this meant she had to give up a cash rebate of about $1,070 USD. Her bank instead offered her a three-year loan at 3 percent interest while still allowing her to take the rebate. Even with the small interest charges, her total cost came to about $17,560 USD — lower than the full price she would have paid with 0% financing. For Sara, the rebate plus low-interest loan was the lower-cost outcome in this scenario.

Lesson learned: Many buyers compare total costs before deciding. 0% financing works best when there is no significant trade-off, but in some cases, alternative financing can leave more money in your pocket. Dollar figures are simplified examples; actual financing terms vary by lender, credit profile, and country.

Situations Where 0% Financing May or May Not Fit

| When 0% Financing Makes Sense | When to Avoid 0% Financing |

| You have excellent credit and a strong repayment history | Your credit score is average or poor, making approval unlikely |

| The exact car model and trim you want are included in the offer | The car you want is not part of the 0% financing promotion |

| You do not lose valuable incentives like cash rebates or big discounts | Choosing 0% financing requires you to give up large rebates or bonuses |

| You can comfortably afford the higher monthly payments of a shorter loan term | Monthly payments would strain your budget due to short loan terms |

| You plan to keep the car for several years | You plan to sell or trade in the car quickly, making the interest savings less impactful |

| The total cost is lower than alternative financing options | A rebate plus low-interest loan results in a lower total cost than 0% financing |

Comparing 0% Financing vs. Other Deals

Before deciding on 0% financing, it is important to compare it with other common offers, such as a low-interest loan combined with a cash rebate, or paying the full amount upfront. The table below shows an example based on a car priced at $14,280 USD

| Option | Details | Total Cost Over Loan Term | Monthly Payment (36 Months) | Savings Compared to Regular Loan |

| 0% Financing | No interest, 36-month term | $14,300 | $397 | About $1,350 saved in interest |

| Low-Interest Loan + Rebate | 3% interest, $714 rebate, 36-month term | $14,630 | $404 | About $1,020 saved vs 6% loan |

| Regular Loan | 6% interest, no rebate, 36-month term | $15,650 | $432 | No savings (base case) |

| Cash Purchase | Full payment upfront | $14,300 | N/A | About $1,350 saved in interest (same as 0%) |

Key takeaway:

0% financing offers the biggest savings compared to a standard loan, but a low-interest loan with a rebate can sometimes come close or even beat it, depending on the rebate size and interest rate. Reviewing total costs can help readers understand different outcomes.

How to Check Live 0% Financing Offers Safely (Instead of Relying on Static Lists)

Because promotional financing changes frequently, fixed lists of “current offers” can become outdated quickly. Rather than relying on static examples, it is safer to understand how to verify real offers directly from reliable sources.

Where to Look for Verified Offers

When researching 0% financing, many buyers review:

- Official manufacturer websites or financing portals

- Authorized dealership announcements

- Bank or Islamic financing provider websites

- Verified auto marketplaces with dated promotions

Availability can vary by region, credit profile, and specific vehicle models.

What to Confirm Before Assuming an Offer Is Real

Instead of focusing only on the headline “0%,” readers may want to check:

- The exact loan term (shorter terms are common with promotional rates)

- Whether rebates or discounts are excluded

- Any processing fees, insurance requirements, or administrative charges

- Eligibility criteria such as income verification or credit history

- Whether the promotion applies to all trims or only selected inventory

Common Pitfalls Buyers Sometimes Experience

- Ignoring the total cost of the deal

- Skipping the credit score check

- Choosing a car just because it qualifies

- Not negotiating the price

- Overstretching your budget with short loan terms

Author: MoneyMentorDesk Editorial Team

This content is for educational purposes only and does not replace professional financial advice.

FAQ Section

Is 0% financing really free?

It is free from interest charges, meaning you do not pay extra money on top of the car’s price for borrowing. However, there may still be other costs such as processing fees, registration charges, or insurance. Reviewing the full cost details can help clarify the agreement.

Can I get 0% financing with bad credit?

It is very unlikely. Most lenders require an excellent credit score and a strong repayment history for approval. If your credit is low, you may need to explore alternative financing options.

What happens if I miss a payment?

Missing a payment can lead to penalties, late fees, and a negative mark on your credit report. In some cases, the lender may cancel your 0% rate and switch you to a standard interest rate for the remaining balance.

Can I negotiate the price of a car with 0% financing?

Yes, Price negotiation may still be part of the buying process. Dealers sometimes use the appeal of 0% financing to avoid discounting the vehicle. Some buyers discuss vehicle pricing before reviewing financing options.

Do all brands offer 0% financing?

No, not all manufacturers provide this option, and even those that do may offer it only on certain models or during special promotions. Availability changes regularly.

Does 0% financing remove cash rebates or discounts?

Some promotions require buyers to choose between a zero-interest loan and a cash rebate. Comparing the total repayment amount can help determine which option provides better overall value.

Is the APR available on all trims and configurations?

Manufacturers often limit 0% financing to selected models, engine options, or loan terms. Confirming eligibility before negotiating the vehicle price can prevent misunderstandings later in the process.

Are there mandatory add-ons or extra fees?

Dealerships may include processing fees, insurance packages, or extended warranties alongside promotional financing. Reviewing the full breakdown of charges helps buyers understand the true cost of the agreement.

Pingback: What Is APR in a Car Loan? - moneymentordesk.com