How long can you finance a boat depends on the loan amount, the lender, the boat’s age, and where you live. In the United States, boat loans typically run from 2 to 20 years. In the United Kingdom, boat finance usually runs from 1 to 15 years, depending on the product and provider. This guide explains the typical terms, what affects them, the rates you may see, and what to check before you sign.

Quick Answer

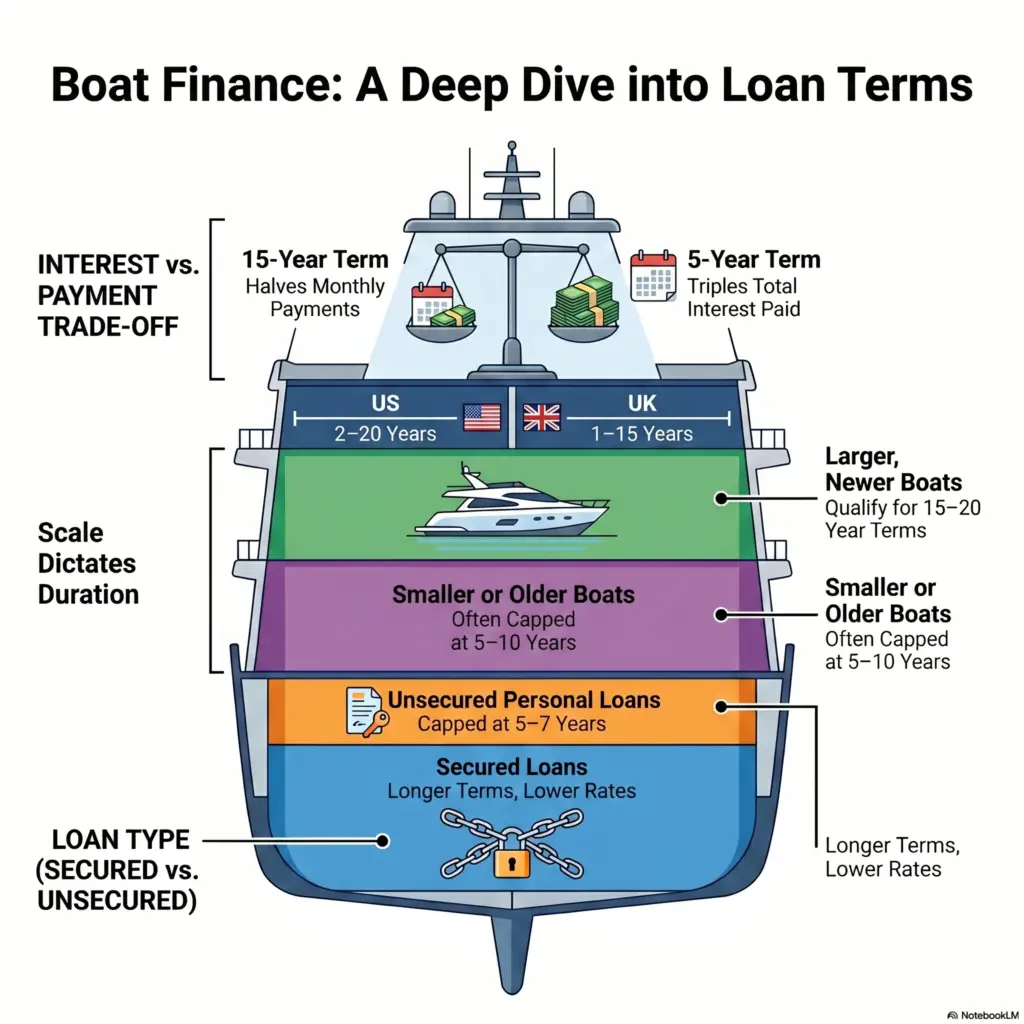

In the US, boat loans usually range from 2 to 20 years, with 10 years being one of the most common terms. Larger, newer boats can qualify for 15–20 year terms; smaller or older boats often max out sooner.

In the UK, boat finance usually runs from 1 to 15 years. Smaller personal loans are often capped at around 5 years (60 months), while larger marine loans or marine mortgages can stretch to 10–15 years.

A longer term lowers your monthly payment but usually increases the total interest you pay. Always compare the total amount payable, not just the monthly figure.

Key Takeaways

- US boat loan terms typically range from 2 to 20 years; 10 years is one of the most common, according to lenders and finance comparison sites.

- UK boat finance usually runs 1 to 15 years, depending on whether you use a personal loan, hire purchase, or a marine mortgage.

- Bigger and newer boats often qualify for longer terms. Smaller or older boats are usually capped at shorter terms.

- Secured boat loans (where the boat is collateral) often allow longer terms and lower rates than an unsecured personal loan.

- A longer term means a lower monthly payment but more total interest. A shorter term costs more each month but less overall.

- The right term depends on your budget, the boat, your credit profile, and how long you plan to keep it. There is no single “best” answer.

Boat Finance Term Lengths at a Glance (US & UK)

| Situation | United States (typical term) | United Kingdom (typical term) |

| Small / used boat (lower value) | 2–10 years | 1–5 years (often a personal loan) |

| Mid-range boat | 10–15 years | 5–10 years |

| Large / new / luxury boat | 15–20 years (sometimes up to 21) | 10–15 years (marine mortgage) |

| Unsecured personal loan route | Usually up to ~7 years | Usually up to ~5 years |

| Most common single term | ~10 years | Varies by lender |

Figures are typical industry ranges and can vary by lender, boat age, deposit, and credit profile. Always confirm the exact term with your finance provider.

How Long Can You Finance a Boat?

In short: most boat loans run between 2 and 20 years. The exact term you are offered depends on the amount you borrow, the boat’s age and type, your credit profile, and the lender’s rules.

In the United States, boat loans are often secured against the boat itself. According to finance comparison sites such as LendingTree and Bankrate, terms commonly range from 2 to 20 years, and a 10-year term is one of the most popular choices. A small number of lenders advertise terms as long as 21 years (252 months) on high-value boats. Because a boat is a large purchase that holds value over time, lenders may offer longer terms than they would for a car.

In the United Kingdom, there is no single standard term. Buyers usually choose between a personal loan, hire purchase (HP), or a marine mortgage. According to UK marine finance providers and guides such as boats.com, smaller loans (often up to around £25,000) are commonly fixed over up to 5 years (60 months), while larger marine loans and marine mortgages above that level can run for 5 to 15 years.

Featured-snippet answer: Boat loans in the US typically range from 2 to 20 years, depending on the loan amount, lender, and boat type. In the UK, boat finance usually runs from 1 to 15 years, depending on the product. Longer terms lower the monthly payment but increase the total interest paid.

What Affects Boat Loan Term Length?

The term you qualify for is shaped by a few clear factors. Lenders look at the loan size, the boat, and you as the borrower before setting a maximum term.

- Loan amount. Larger loans usually allow longer terms. In the US, boats under about $50,000 often come with terms of 5–10 years, mid-range boats with 10–15 years, and high-value boats over $200,000 with terms up to 20 years, according to lender guidance summarised by Boat Trader.

- Boat age and condition. Newer boats often qualify for the longest terms (15–20 years in the US). Older boats — for example, those already 10–15 years old — are frequently capped at shorter terms such as 10–12 years, because lenders consider their future value.

- New vs used. A used boat can usually still be financed, but the maximum term may be shorter than for a new boat of the same value.

- Secured vs unsecured. A secured boat loan (with the boat as collateral) tends to allow longer terms. An unsecured personal loan is usually capped at around 5–7 years.

- Your credit profile. A stronger credit history can widen your options. A weaker profile may mean a shorter term, a higher rate, or a larger deposit.

- Lender policy. Each lender sets its own maximum term, so two lenders may offer different terms for the same boat.

What Are Typical Boat Loan Interest Rates?

Boat loan rates depend mostly on your credit profile, the boat, the term, and the wider interest-rate environment. They are not fixed by any regulator, so they move over time and vary between lenders.

In the United States in 2026, rates generally fall between about 6% and 12% APR, according to Bankrate and LendingTree. As a rough guide:

| Borrower profile | Typical US rate range (2026) |

| Excellent credit (720+), newer boat over $50,000 | ~6–8% APR |

| Good credit | ~8–10% APR |

| Fair/weaker credit, older or smaller boat | ~9–12%+ APR |

Rates are examples only and change with the wider economy. Your actual rate depends on the lender and your circumstances.

In the United Kingdom, marine finance rates vary by lender and by product (personal loan, hire purchase, or marine mortgage), your deposit, and your credit profile. Because UK rates are not published as a single standard figure, the best approach is to compare the APR and the total amount payable across providers, and to check the provider is authorised by the Financial Conduct Authority (FCA).

Worked example: how the term changes the cost

Imagine a $30,000 boat financed at an example rate of 8% APR. This simplified illustration (excluding fees and insurance) shows how the term length changes both the monthly payment and the total interest:

| Term | Approx. monthly payment | Approx. total interest |

| 5 years | ~$608 | ~$6,500 |

| 10 years | ~$364 | ~$13,700 |

| 15 years | ~$287 | ~$21,600 |

The longer term cuts the monthly payment by roughly half but more than triples the total interest. This is why the total amount payable matters more than the monthly figure alone.

Can You Get 0% Boat Finance?

Yes, 0% boat finance exists, but it is limited and conditional. It is usually a short-term promotional offer from a boat or engine manufacturer, not a standard rate from a bank.

For example, in early 2026 several US manufacturers ran 0% promotions: Honda Marine advertised 0% APR for up to 24 months on new outboard engines, and brands sold through Bass Pro Shops and Cabela’s Boating Centers offered 0% for 12 months on qualifying purchases. These deals usually require strong credit, apply only to specific new models, and last for a short promotional period.

For most buyers, and especially for used boats, a standard secured boat loan or personal loan is more realistic than a 0% deal. Always read the offer terms, because a 0% headline can come with conditions such as a minimum spend, a large deposit, or a short repayment window.

Boat Loan vs Personal Loan: Which Is Better?

A boat loan is usually secured against the boat; a personal loan is usually unsecured. That single difference drives the rates, terms, and risks.

| Feature | Secured boat loan | Unsecured personal loan |

| Collateral | The boat secures the loan | None |

| Typical term | Up to 20 years (US) | Usually up to 5–7 years |

| Interest rate | Often lower | Often higher |

| Approval speed | Can be slower (boat valued) | Often faster |

| Risk if you default | Lender may repossess the boat | No boat repossession, but credit damage and collection action |

| Best for | Larger or newer boats | Smaller boats, or keeping the boat lien-free |

According to the US Consumer Financial Protection Bureau (CFPB), unsecured loans put lenders at higher risk, so they often carry higher interest rates than secured loans. A secured boat loan can therefore be cheaper and longer, but you could lose the boat if you cannot keep up payments. An unsecured personal loan keeps the boat free of any lien and can be faster to arrange, but it usually costs more and runs for a shorter term.

How Does Boat Finance Work in the UK?

UK buyers usually choose between three main routes, all of which should be provided by a firm authorised and regulated by the Financial Conduct Authority (FCA).

- Personal loan. An unsecured loan from a bank or lender, often repaid over 1–5 years. The boat is not used as security.

- Hire purchase (HP). You pay a deposit, then fixed monthly instalments over an agreed term. You usually own the boat after the final payment.

- Marine mortgage. A secured loan designed for boats, where the boat is the collateral. These often allow the longest terms (up to around 15 years) and larger amounts, according to UK marine finance guides such as boats.com.

If something goes wrong with a UK finance agreement, free and impartial guidance is available from MoneyHelper and Citizens Advice. If you cannot resolve a complaint with the lender directly, you can escalate it to the Financial Ombudsman Service after you receive the lender’s final response.

What Should You Check Before You Finance a Boat?

Before you sign any boat finance agreement, work through this checklist. A few minutes of checking can prevent an expensive mistake.

- Compare the total amount payable, not just the monthly payment.

- Check the APR and whether the rate is fixed or variable.

- Confirm the term length and whether it suits how long you plan to keep the boat.

- Ask about the deposit required and how it affects the rate.

- Check for fees — arrangement fees, early settlement charges, and late-payment fees.

- Ask if you can settle early and what it would cost.

- Confirm the lender is authorised — FCA in the UK; a reputable, licensed lender in the US.

- Consider insurance, including whether you need extra cover while finance is outstanding.

- Read the full agreement before signing, and keep a copy.

Where Can You Get Help and Know Your Rights?

Free, official guidance is available in both countries. Use it before you borrow and if a problem arises later.

In the United States, the Consumer Financial Protection Bureau (CFPB) publishes plain-English consumer guidance and lets you submit a complaint about a financial company. Industry context on boat sales and ownership is published by the National Marine Manufacturers Association (NMMA); according to the NMMA, pre-owned boats make up roughly 80% of annual unit sales in the US, which is why used-boat finance is so common.

In the United Kingdom, finance providers are regulated by the FCA. For free guidance, use MoneyHelper or Citizens Advice. To escalate an unresolved complaint, contact the Financial Ombudsman Service.

Frequently Asked Questions

How long can you finance a boat in the US?

In the United States, boat loans typically run from 2 to 20 years, with 10 years among the most common terms. Larger, newer boats can qualify for 15–20 year terms, while smaller or older boats are usually capped sooner. The exact term depends on the loan amount, the boat’s age, your credit, and the lender’s rules.

How long can you finance a boat in the UK?

In the United Kingdom, boat finance usually runs from 1 to 15 years. Smaller personal loans are often capped at around 5 years, while larger marine loans and marine mortgages can stretch to 10–15 years. The term depends on the product, the amount borrowed, and the FCA-authorised lender you choose.

Is a longer boat loan term better?

Not always. A longer term lowers your monthly payment, which can help your budget, but it usually increases the total interest you pay over the life of the loan. A shorter term costs more each month but less overall. The right choice depends on your budget and how long you plan to keep the boat.

Can you finance a used boat?

Yes, used boats can usually be financed, though the maximum term may be shorter than for a new boat. According to the NMMA, pre-owned boats make up around 80% of US boat sales, so used-boat finance is widely available. Older boats may have stricter terms because lenders consider the boat’s future value.

What credit score do you need to finance a boat?

There is no single required score, and rules vary by lender and country. In the US, stronger credit (often 700+) usually unlocks the lowest rates and longest terms, while weaker credit may mean a higher rate, a larger deposit, or a shorter term. Always check the lender’s criteria before applying.

Is 0% boat finance real?

Yes, but it is limited. It is usually a short-term promotion from a boat or engine manufacturer on specific new models, and it often requires strong credit. For most buyers, especially for used boats, a standard secured boat loan or personal loan is more realistic than a 0% offer.

What happens if I can’t keep up with boat loan payments?

If your loan is secured against the boat, the lender may repossess it to recover what is owed. Missed payments can also harm your credit. If you are struggling, contact your lender early. In the UK, free help is available from MoneyHelper and Citizens Advice, and unresolved complaints can go to the Financial Ombudsman Service.

The Verdict: Which Boat Finance Term Is Right for You?

There is no single best term — it depends on your goals. Use these simple rules of thumb:

- Choose a shorter term if you want to pay less interest overall, you can afford higher monthly payments, or you plan to keep the boat only a few years.

- Choose a longer term if you need a lower monthly payment to fit your budget and you are comfortable paying more interest over time.

- Consider a secured boat loan or marine mortgage for larger or newer boats, where longer terms and lower rates are usually available.

- Consider an unsecured personal loan for a smaller or older boat, or if you want to keep the boat free of any lien.

Whatever you choose, compare the total amount payable, not just the monthly payment, and confirm the lender is properly authorised before you sign.

Author Note

This article was prepared by the MoneyMentorDesk editorial team for general finance education. It explains common boat finance terms in the US and UK, including typical loan lengths, repayment options, and key checks before borrowing. Because loan rates and lender rules change regularly, readers should confirm current terms directly with a lender or finance provider before making a decision. This content is not personal financial advice and should not replace guidance from a qualified financial professional.

Editorial Note

This article is for general education only. Loan terms, rates, and promotional offers change frequently and vary by lender and country. Always confirm current details directly with your finance provider.

Financial Disclaimer

MoneyMentorDesk.com is a finance education website. We are not a lender, broker, or financial advisor, and this article is not personal financial advice. Figures are examples and may not reflect the offer available to you. Your eligibility, rate, and term depend on the lender and your individual circumstances. For advice on your situation, speak to a qualified, regulated professional or use a free service such as MoneyHelper (UK).

Sources

- Consumer Financial Protection Bureau (CFPB)

- Consumer Financial Protection Bureau (CFPB)

- National Marine Manufacturers Association (NMMA)

- Bankrate — Boat loans and rates (May 2026)

- Boat Trader — How long can you finance a boat:

- Financial Conduct Authority (FCA)

- MoneyHelper (UK)

- Citizens Advice (UK)

- Financial Ombudsman Service (UK)