How Long Should a Car Loan Be?

Key takeaways

- A car loan should usually be no longer than 60 months (5 years) for a new car, and 36–48 months for a used car, so you pay less interest and lower your risk of owing more than the car is worth. This is general guidance, not a rule.

- A longer loan lowers your monthly payment but raises the total interest you pay — and the loan may carry a higher rate. The U.S. Federal Trade Commission warns that “the longer the length of the loan, the more expensive the deal will be overall.”

- The average new-car loan now runs close to six years. Experian reported an average new-vehicle term of 69.48 months in Q1 2026, and more than a third of new loans now stretch past six years.

- Long loans are tied to negative equity (owing more than the car is worth). A CFPB study found borrowers who rolled negative equity into a new loan had an average term of 73 months and were more than twice as likely to face repossession within two years.

- Pick the shortest term whose monthly payment you can comfortably afford — not the longest term that makes the payment look small.

How long should a car loan be?

A car loan should be as short as you can comfortably afford, because a shorter term means less interest paid and less time owing more than the car is worth. A common guideline is to keep a new-car loan at 60 months (5 years) or less and a used-car loan at 36–48 months. Longer terms lower the monthly payment but cost more overall.

The “right” length is the one where the monthly payment fits your budget and the total cost stays reasonable. Below, we show real numbers on how the term changes what you pay, using current data from the Federal Reserve, the FTC, the CFPB, and Experian.

Educational only: This article is general information, not financial advice. Your best loan length depends on your budget, credit, and the car you buy.

What are the most common car loan terms?

Car loans are usually sold in 12-month steps, from about 24 months up to 84 months (2 to 7 years). The most common choices are 48, 60, and 72 months. Some lenders now offer 84-month loans or longer. A shorter term raises your monthly payment but cuts total interest; a longer term does the opposite.

| Loan term | Length | What it usually means for you |

| 24–36 months | 2–3 years | Highest monthly payment, lowest total interest |

| 48 months | 4 years | Higher payment, strong interest savings |

| 60 months | 5 years | Balanced payment and interest — a common cap for new cars |

| 72 months | 6 years | Lower payment, more interest, higher negative-equity risk |

| 84+ months | 7+ years | Lowest payment, most interest, highest risk of being “underwater” |

The Federal Trade Commission (FTC) notes that “many creditors offer longer-term loans, like 72 or 84 months,” and warns that while these lower your monthly payment, “they may have high rates.” Before you sign, compare the total cost of each loan over its full term, not just the monthly payment.

What is the average car loan length right now?

The average car loan is now close to six years. According to Experian’s State of the Automotive Finance Market Report for Q1 2026, the average loan term was 69.48 months for a new vehicle and 67.73 months for a used vehicle. Separately, the Federal Reserve reports an average maturity of about 66 months for new-car loans at finance companies.

Longer loans are also becoming more common. Experian found that 35.55% of new-vehicle loans in Q1 2026 had terms longer than six years, up from 30.83% a year earlier. Loans longer than 85 months rose to 3.33% of new loans. For context, Experian put the average new-vehicle loan amount at $43,925 and the average new-vehicle monthly payment at $770.

How does loan length affect your monthly payment and total interest?

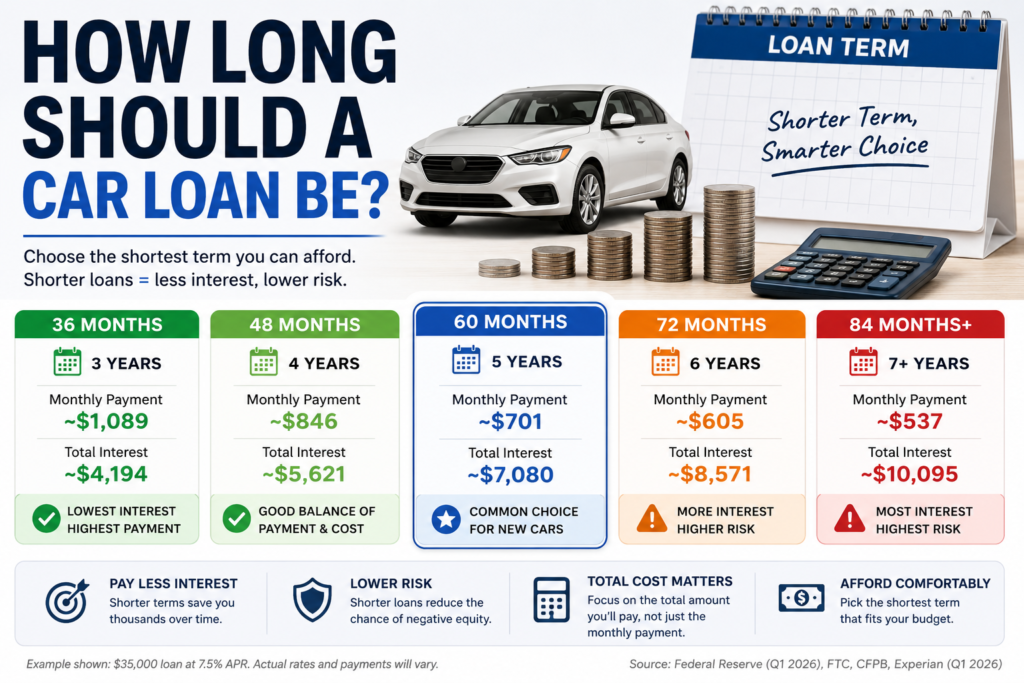

A longer loan lowers your monthly payment but increases the total interest you pay, because you borrow for more months. The table below shows the same $35,000 loan at the same 7.5% APR across different terms. Only the term changes — yet the total interest more than doubles from 36 to 84 months.

| Term | Monthly payment | Total interest paid |

| 36 months | ~$1,089 | ~$4,194 |

| 48 months | ~$846 | ~$5,621 |

| 60 months | ~$701 | ~$7,080 |

| 72 months | ~$605 | ~$8,571 |

| 84 months | ~$537 | ~$10,095 |

Illustration only. Figures are calculated with a standard loan formula using a $35,000 balance and a 7.5% APR; your real numbers will differ. APR examples below use current Federal Reserve data.

Notice the trade-off. Stretching from 60 to 72 months drops the payment about $96 a month but adds roughly $1,500 in interest. Going to 84 months saves more each month but costs about $3,000 more than the 60-month loan. The FTC sums it up: focus on “your total cost, not just the monthly payment.”

Try it with your own numbers. Use the car loan term calculator below to compare the monthly payment and total interest for any loan amount, APR, and term.

Car Loan Term Calculator

See how the loan term changes your monthly payment and the total interest you pay. Shorter terms cost less overall.

| Term | Monthly payment | Total interest | Total cost |

|---|

Estimates use a standard fixed-rate amortization formula and assume the same APR across terms. Your real rate may rise with a longer term, which would make long loans cost even more. This tool is educational only and is not financial advice. Source for current average rates: U.S. Federal Reserve, Consumer Credit (G.19).

Do longer car loans have higher interest rates?

Often, yes. Lenders take on more risk over a longer payback period, so longer terms can carry the same or higher rates than shorter ones. In the first quarter of 2026, the Federal Reserve reported an average commercial-bank APR of 7.52% on a 60-month new-car loan and 7.55% on a 72-month new-car loan. The FTC also warns that longer loans “may have high rates.”

A higher rate on a longer term is a double cost: you pay interest for more months and at a higher percentage. When you compare offers, compare the APR and the term together, not just the monthly payment. The CFPB notes that loan terms are negotiable, and shopping around “can save you hundreds or even thousands of dollars over the life of your loan.” Our guide to what APR on a car loan means explains how your credit score shapes the rate you’re offered. And if a dealer offers 0% APR or a cash rebate, weigh them carefully — that choice is separate from your loan length.

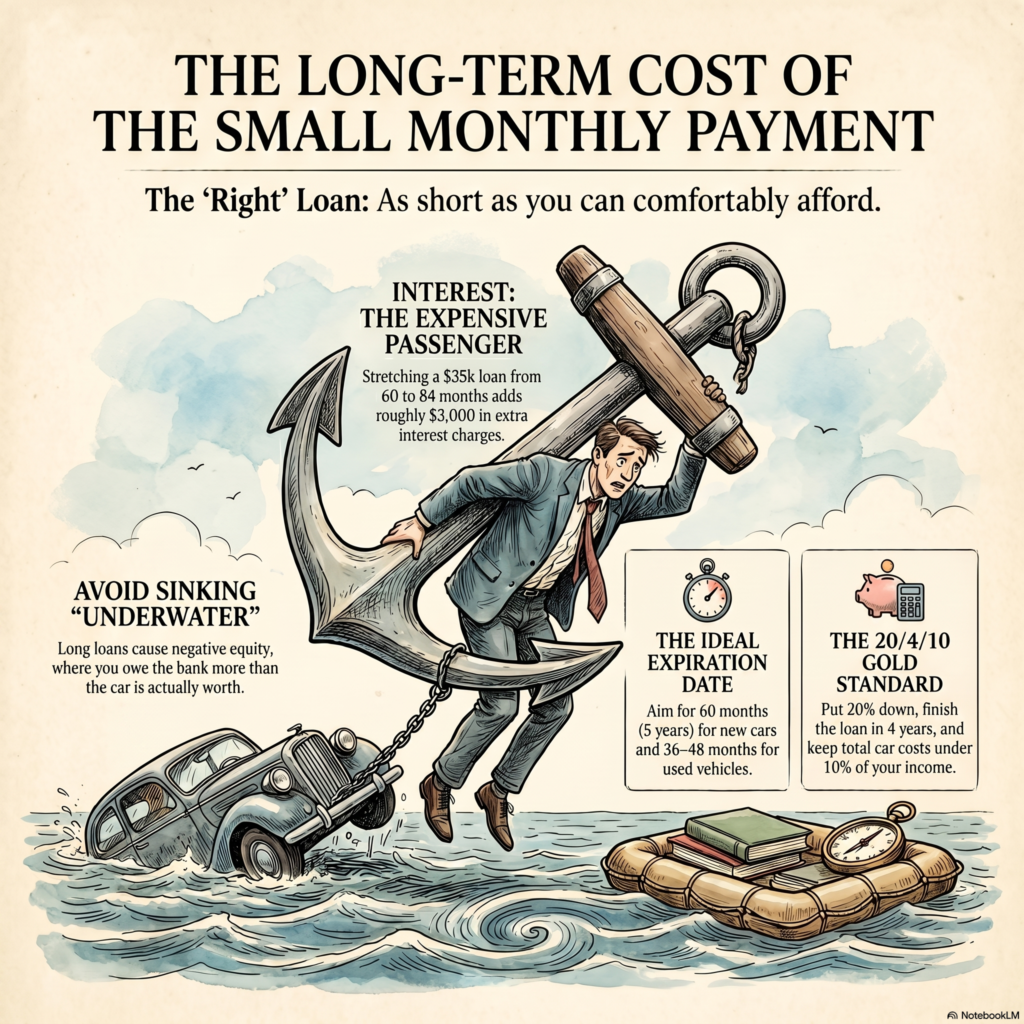

What is negative equity, and how do long loans cause it?

Negative equity means you owe more on your car loan than the car is worth — also called being “underwater” or “upside down.” Long loans cause it because you pay down the balance slowly while the car loses value quickly. The FTC notes that “cars quickly lose value once you drive off the lot, so with longer-term financing, you could end up owing more than the car is worth.”

The risk is real and measurable. A CFPB study of 2018–2022 auto loans found that borrowers who rolled negative equity into a new loan had an average term of 73 months, compared with 67–68 months for other borrowers. Those borrowers also had a higher average loan-to-value ratio (119.3%) and were more than twice as likely to have their car assigned for repossession within two years. As the CFPB puts it, higher loan-to-value ratios “generally lead to consumers being underwater for longer.” If you’re trading in a car, you still owe money on, ask the dealer how that negative equity will be added to your new loan before you sign.

How long should you finance a new vs. used car?

Finance a new car for no more than 60 months and a used car for 36–48 months where your budget allows. Used cars are older and may need repairs sooner, so a shorter term helps you avoid still paying for a car after its value — and reliability — have dropped. Matching the loan length to how long you’ll keep the car lowers your risk of going underwater.

This is general guidance, not a fixed rule. If a slightly longer term is the only way to keep the payment affordable and safe for your budget, that can be reasonable — but try to add a larger down payment and pay extra when you can. The goal is to own real value in the car, not to owe more than it’s worth.

Signs a car loan is too long for you

A loan term is probably too long if it creates these warning signs. Each one points to paying too much or staying underwater for years.

- You can only afford the car by stretching to 72 or 84 months.

- The total interest (not the monthly payment) feels shocking when you add it up.

- You expect to trade or sell the car before the loan is even half paid off.

- You’re rolling old debt (negative equity) from a previous car into the new loan.

- The longer term comes with a higher APR than the shorter option.

If two or more of these apply, consider a cheaper car, a bigger down payment, or a shorter term.

How to choose the right car loan length

Choose your loan length by working backward from total cost and your budget, not from the lowest possible monthly payment. These steps follow guidance from the FTC and CFPB.

- Set a budget first. A popular guideline is the 20/4/10 rule: put about 20% down, keep the loan to 4 years (48 months), and keep total transportation costs under 10% of your monthly income. Treat it as a target, not a law.

- Get pre-approved. The FTC suggests getting your APR, term, and maximum amount from a bank or credit union before you visit the dealer, so you can compare offers.

- Compare APR and term together. A low payment on a long term can hide a high total cost. Use the CFPB’s free Auto Loan Shopping Sheet to compare offers side by side.

- Add a down payment. The FTC notes a down payment “reduces the amount you need to finance” and lowers your total cost — and your negative-equity risk.

- Pick the shortest term you can comfortably afford. If money gets tight later, you can look at refinancing the loan. Experian reported that drivers who refinanced in Q1 2026 cut their rate by an average of 2.2% and saved about $81 a month.

Frequently asked questions

Is a 72-month car loan a bad idea?

A 72-month car loan isn’t always bad, but it carries more risk. It lowers your monthly payment, yet you pay more total interest and stay underwater longer. The FTC warns that longer loans “may have high rates” and cost more overall. It can work with a strong down payment and a car you’ll keep for years.

Is it better to have a longer or shorter car loan?

A shorter car loan is usually better for your wallet. You pay less total interest and build equity faster, which lowers the chance of owing more than the car is worth. A longer loan only wins on the monthly payment. Pick the shortest term whose payment fits your budget comfortably.

What is the 20/4/10 rule for car buying?

The 20/4/10 rule is a popular budgeting guideline: put at least 20% down, finance the car for no more than 4 years (48 months), and keep your total monthly transportation costs under 10% of your gross income. It’s a rule of thumb to keep car costs affordable, not an official regulation.

Can I pay off a car loan early to save interest?

Usually yes. Paying extra toward the principal reduces the interest you owe over time. Most auto loans don’t charge prepayment penalties, but the FTC and CFPB recommend checking your contract first. Even small extra payments on a long loan can shorten the term and cut total interest.

Does a longer car loan hurt my credit score?

The loan term itself doesn’t directly lower your credit score. What matters is making payments on time. But longer loans keep you in debt longer and raise the risk of missed payments if money gets tight, and late payments do hurt your credit. The CFPB notes late or missed payments can lead to repossession and credit damage.

What is the longest car loan term I can get?

Many lenders offer terms up to 84 months (7 years), and a small but growing share run even longer. Experian reported that 3.33% of new-vehicle loans in Q1 2026 had terms over 85 months. Longer terms lower the payment but carry the most interest and the highest risk of negative equity.

Should I refinance my car loan to a shorter term?

Refinancing to a shorter term can save interest if you can afford the higher payment and qualify for a similar or lower rate. Experian found Q1 2026 refinancers cut their rate by about 2.2% on average. Compare the new APR, term, and any fees before you switch.

About the author

Nimra Saleem is a personal-finance writer at MoneyMentorDesk.com. She turns car-buying, borrowing, and budgeting topics into plain-English guides that help everyday readers compare their options before they sign. She writes each guide directly from primary sources, including federal regulators, the Federal Reserve, and official lender data.

Disclosure

This guide was written by Nimra Saleem for MoneyMentorDesk.com and reviewed against the Federal Reserve (Consumer Credit – G.19), the Federal Trade Commission, the Consumer Financial Protection Bureau, and Experian auto-finance data. It is educational only and is not financial advice. Rates, averages, and loan terms change over time — confirm current figures with the official sources linked in this article and with any lender before you borrow.