Learn how to calculate the total cost of a car loan, including APR, loan term, fees, and monthly payments, so you can confidently compare loan offers. Many car buyers focus on the monthly payment first. That is common, but it does not show the full cost of the loan. A lower monthly payment can still mean a more expensive deal if the APR is higher, the term is longer, or extra products are added to the financing.

If you want to compare loan offers properly, you need to calculate the total cost of a car loan, not just the monthly bill. The Consumer Financial Protection Bureau’s guidance on comparing auto loan offers explains that buyers should compare the APR, interest rate, loan term, and total amount financed rather than relying only on the payment. (Consumer Financial Protection Bureau)

What is the total cost of a car loan?

The total cost of a car loan is the full amount you pay over time for both the vehicle and the borrowing cost attached to it.

A practical way to think about it is:

Total purchase cost = down payment + total of monthly payments

Another useful formula is:

Total loan cost = amount financed + finance charge

These two formulas help answer different questions. The first shows what the car costs you overall. The second shows what the loan itself costs after borrowing. The CFPB’s Truth-in-Lending disclosure explainer for auto loans explains key terms such as APR, finance charge, amount financed, and total of payments.

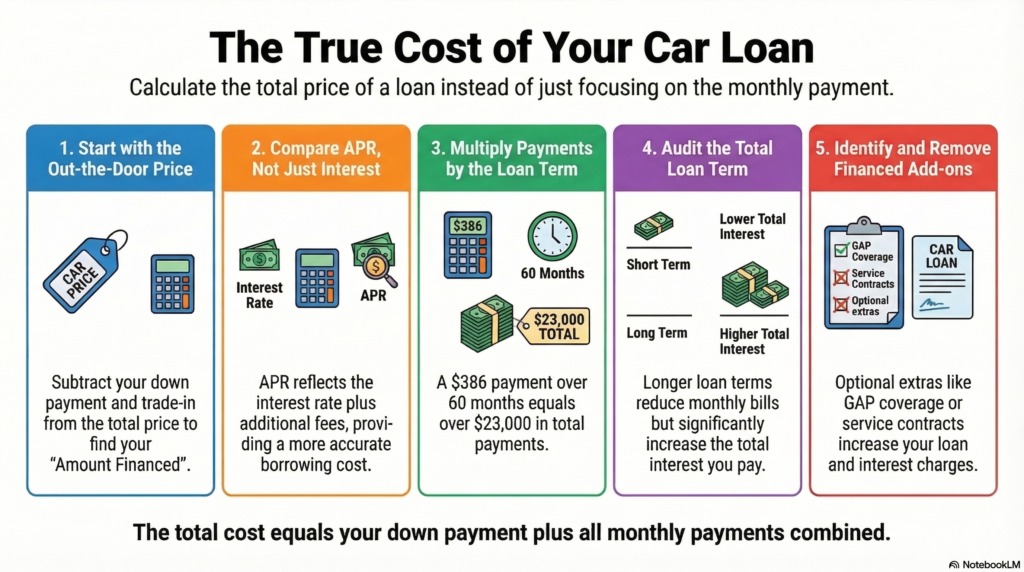

Step 1: Start with the out-the-door price

Do not begin with only the sticker price. Start with the out-the-door price, which may include the vehicle price, taxes, registration, dealer fees, and any products rolled into the deal.

Then subtract:

- your down payment

- your trade-in credit

What remains is usually the amount financed.

This step matters because many buyers underestimate how quickly extra costs raise the loan balance. Optional products such as GAP coverage, service contracts, and dealer add-ons can increase the financed amount and make the loan more expensive over time. The FTC’s guide to financing or leasing a car warns that add-ons are extra items you may finance with the car, and the FTC’s add-ons alert stresses that buyers should read the contract carefully and remove add-ons they do not want.

Step 2: Understand APR vs. interest rate

The interest rate is the base cost of borrowing. The APR is broader and is usually the better number for comparing loan offers because it can reflect the borrowing cost more fully. The CFPB’s explanation of APR vs. interest rate says the APR measures the interest rate plus additional fees charged with the loan.

That is why two loans with similar monthly payments may still have very different total costs. If one loan has a lower APR, it may cost less overall even if the monthly payment difference looks small. The CFPB auto loan key terms page also notes that lenders must disclose APR before you are legally obligated on the loan, which makes APR one of the best numbers for comparing offers.

Step 3: Calculate the total of payments

Once you know the amount financed, APR, and loan term, calculate the monthly payment and then multiply it by the number of months.

Example

- Car price: $25,000

- Down payment: $5,000

- Amount financed: $20,000

- APR: 6%

- Loan term: 60 months

If the monthly payment is about $386.66, then:

$386.66 × 60 = $23,199.60

That means the total of monthly payments is about $23,199.60.

Then add the down payment:

$23,199.60 + $5,000 = $28,199.60

So the total purchase cost is about $28,199.60.

This is much more useful than saying the car “costs $386 a month.”

Step 4: Compare how loan term changes the cost

Loan term has a major effect on the total amount paid. A longer loan term usually reduces the monthly payment, but it often increases the total interest paid. The CFPB’s comparing auto loans worksheet states that a longer loan term increases total cost, and the FTC’s financing guide warns that longer loans can make a deal more expensive overall.

Example: 60 months vs. 72 months

Suppose the amount financed stays at $20,000, but one offer is for 60 months and another is for 72 months.

The 72-month option may look easier each month, but the borrower often pays more over time because interest runs longer. This is one of the most common reasons a cheaper monthly payment becomes a more expensive loan overall.

Step 5: Watch for financed extras

Many buyers focus on the vehicle price and forget that extra products can also be financed. This can increase both the amount financed and the total amount paid.

Examples include:

- service contracts

- dealer add-ons

- GAP coverage

- optional protection packages

If these are added to the contract, you may pay interest on them too. That is why it is important to check what is included before signing. The FTC’s consumer tips on car add-ons explain that add-ons cost extra and can break your budget, while the FTC financing guide says buyers should know how much add-ons cost over the life of the loan.

How to compare two car loan offers properly

When you compare offers, do not compare the monthly payment alone. Compare these five things together:

- Amount financed

- APR

- Loan term

- Total of payments

- Down payment or trade-in contribution

This gives you a fair view of the true cost. If you only compare monthly payments, you can easily choose the worse deal without realizing it. The CFPB comparison worksheet is useful here because it is designed to compare total cost, interest, and upfront contributions across offers.

Common mistakes that increase car loan total cost

One common mistake is choosing the lowest monthly payment without checking the total amount paid. Another is financing optional extras without noticing how much they increase the loan. A third mistake is ignoring the effect of a longer term. Some buyers also overlook how negative equity can raise the amount financed when they trade in a car with a balance still owed. The FTC financing guide and the CFPB comparison guidance both reinforce that buyers should look beyond the monthly payment and review the full financing terms carefully.

Final takeaway

If you want to know how much a car loan really costs, look beyond the monthly payment. Start with the out-the-door price, subtract your down payment and trade-in credit to find the amount financed, then calculate the total of monthly payments and add your upfront contribution back in.

That is the clearest way to calculate the total cost of a car loan and compare offers more accurately before you sign.

Before agreeing to any loan, review the contract carefully, confirm what is included in the financing, and make sure you understand the APR, term, finance charge, amount financed, and total amount you will pay over time. The CFPB’s Truth-in-Lending disclosure page is the best official source to link here because it explains exactly what those disclosure terms mean.

Editorial note: This article is for educational purposes only and does not provide personal financial, legal, or tax advice. Loan terms and costs vary by lender, borrower profile, and vehicle type.

FAQs

Is the monthly payment the best way to compare car loans?

No. The monthly payment alone can be misleading. You should also compare the APR, loan term, amount financed, and total of payments. The CFPB auto loan comparison page supports this approach.

What is included in the total cost of a car loan?

The total cost usually includes your down payment, all monthly payments, and any financed charges built into the loan. The Truth-in-Lending disclosure explainer helps define those parts.

Does a longer car loan always cost more?

Not in every possible case, but a longer term often increases the total interest paid and raises the total cost of the loan. The CFPB comparison worksheet says longer terms increase total cost. (Consumer Financial Protection Bureau)

How do dealer add-ons affect total car loan cost?

If add-ons are financed, they increase the amount financed and can also increase the total interest paid over time. The FTC add-ons guidance and FTC add-ons tips are strong external sources for this point.

What is the difference between amount financed and total amount paid?

The amount financed is what you borrow. The total amount paid includes what you repay over time, including interest and other financed costs. The CFPB Truth-in-Lending explainer covers these definitions.

Can negative equity increase the total cost of a car loan?

Yes. If unpaid balance from the old vehicle is rolled into the new loan, the financed amount goes up, which can increase total borrowing cost. That follows directly from how amount financed works in the CFPB’s auto loan disclosure guidance.