Motorcycle breakdown insurance helps when your bike won’t start or fails on the road—punctures, battery issues, electrical faults, misfuelling, and long-trip breakdowns. This quick guide compares the best options, from local motorcycle recovery near me and SOS Motorcycle Recovery to personal and standard motorcycle breakdown service. We also explain European breakdown cover and RAC breakdown cover so you can choose with confidence.

What Is Motorcycle Breakdown Insurance?

Motorcycle breakdown insurance is a roadside assistance plan for bikes that sends a mechanic to fix you at the kerb and includes towing if repair isn’t possible. Many policies add optional home start, onward travel (taxi/hire car/hotel), and European cover for trips abroad.

Pros and Cons of Motorcycle Breakdown Insurance

Pros

- Gives fast roadside help if your bike stops working

- Can include towing to a garage or home

- Useful for punctures, battery issues, and electrical faults

- Optional extras like home start, onward travel, and European cover add peace of mind

- Can save money compared with paying a one-off recovery fee

Cons

- Annual cover adds an extra running cost

- Some plans have call-out limits, tow caps, or labour limits

- Accident damage and routine maintenance are usually excluded

- The cheapest plans may not include home start or onward travel

- Extra services often cost more

What it usually doesn’t cover

- Accident damage or crash repairs (that’s motor insurance).

- Routine maintenance or wear-and-tear fixes (e.g., scheduled servicing).

- Pre-existing or recurring faults noted before purchase.

- Track days, racing, or off-road use (often excluded).

- Parts costs beyond stated limits unless specified.

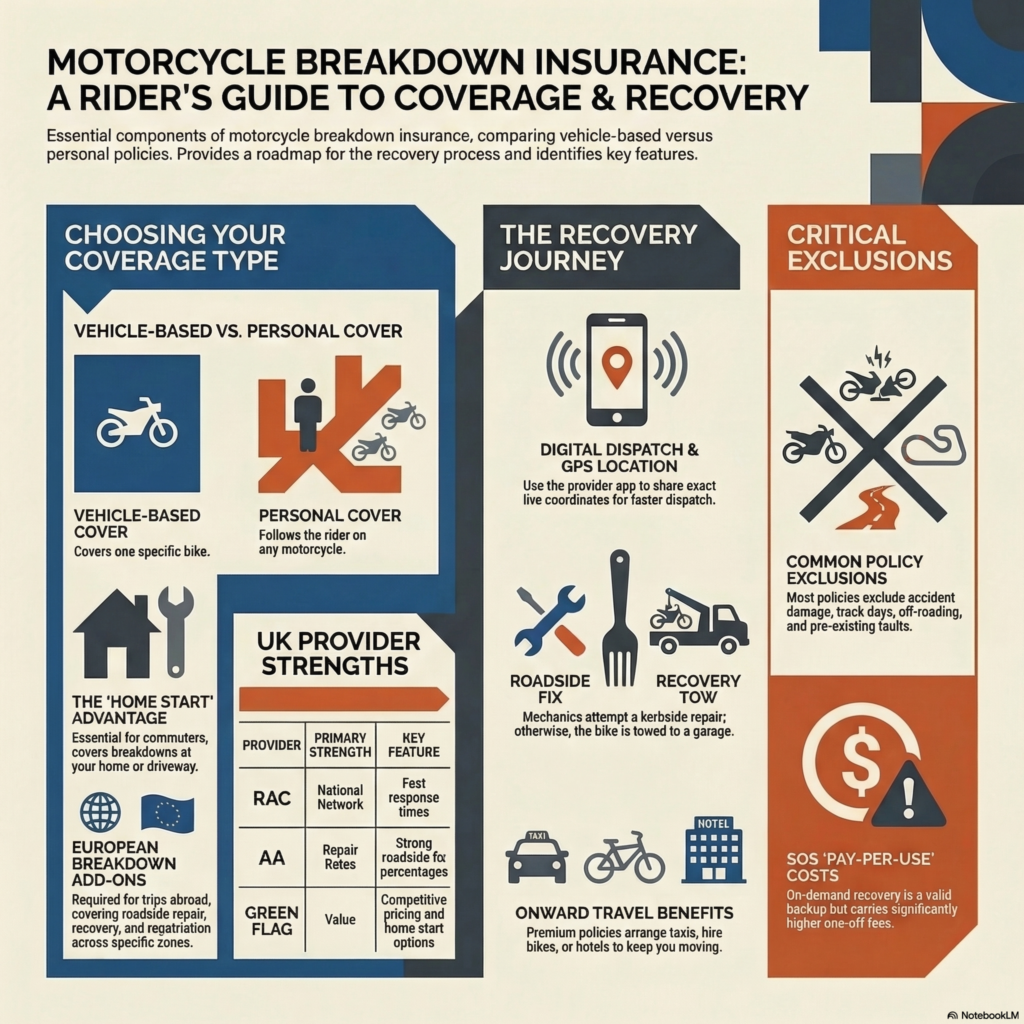

Vehicle-based vs Personal breakdown cover

- Vehicle-based: Covers one named bike, whoever rides it. Best if you own and use a single motorcycle.

- Personal: Covers you on any bike you ride (often even as a passenger). Ideal for multi-bike owners, pillion riders, or those who borrow/ride different motorcycles.

How It Works (Step-by-Step)

- Breakdown → call via app/phone

Move to a safe spot, switch hazards on, and share your live location. Give your policy number, bike reg, and a short description of the fault (e.g., flat battery, puncture).

- Service dispatch (ETA & safety)

Your provider confirms cover, assigns the nearest patrol, and gives an ETA. Follow any safety advice while you wait; you may get SMS/app tracking updates.

- Roadside fix or recovery

The mechanic tries a kerbside repair. If it can’t be fixed quickly, you get motorcycle recovery (towing) to a suitable garage or your home—within the tow limits in your policy.

- Onward travel (if included)

If you have this benefit, the provider arranges a taxi, hire bike/car, train tickets, or a hotel. Keep all receipts; daily caps and time limits usually apply.

- Excess & claim notes

You may pay an excess or parts/labour not covered. Note the job number, patrol report, and any costs for reimbursement. Check call-out limits and exclusions (e.g., accidents or track use).

Best Motorcycle Breakdown Insurance — How to Choose

Must-Have Features

- Large national network & fast ETAs: More patrols usually means quicker help. Check average response times and 24/7 availability.

- Strong roadside repair rate: Higher “fixed at the kerb” rates reduce towing and downtime.

- Clear tow mileage: Know the included recovery distance (e.g., to nearest suitable garage or home).

- Labour limits stated: How many minutes/hours of roadside labour are covered?

- Fuel misfill help: Drain/refuel support and any capped costs.

- Puncture/tyre assistance: Mobile plug/repair or transport to a tyre shop.

- Battery support: Jump-start plus an option/pathway for replacement if needed.

- Multi-bike/family options: Discounts or bundles if you own more than one bike or want to cover riders.

Nice-to-Have Extras

- Keys lost/broken: Call-out for lockouts or snapped keys.

- Trip continuation: Taxi, hire bike/car, or rail tickets to keep you moving.

- Hotel allowance: Overnight stay limits for longer delays.

- App tracking: Live ETA, location share, and status updates.

- Seasonal/winter add-ons: Extra cover or checks for cold-weather riding.

Pricing Factors

- Bike age/CC: Older or higher-capacity bikes can cost more to cover.

- Rider age & postcode: Risk and distance to patrols can affect price.

- Pay yearly vs monthly: Annual often costs less overall.

- Add-on bundles: Home start, European cover, and onward travel increase price but may save money when needed.

Typical Price Examples

Prices vary by provider, bike type, location, and add-ons, but basic motorcycle breakdown cover is often cheaper than fully comprehensive plans. A basic vehicle-based plan may cost less per year than a personal plan, while adding home start, onward travel, or European cover usually increases the price. Monthly payments can look cheaper upfront, but annual payment is often better value overall. Always compare the total yearly cost, not just the monthly amount.

Quick Comparison Checklist (fill in before you buy)

| Provider | Vehicle/Personal | Home Start | Onward Travel | EU Option | Max Tow/Recovery | App Tracking | Price Band |

| Provider A | Vehicle | Yes/No | Yes/No (limits) | Yes/No | e.g., to nearest suitable / 50–100 km | Yes/No | Low / Med / High |

| Provider B | Personal | Yes/No | Yes/No (limits) | Yes/No | e.g., home or chosen garage within X km | Yes/No | Low / Med / High |

Tip: If you ride multiple bikes or sometimes as a passenger, consider personal breakdown cover. If you mostly ride one bike, vehicle-based cover may be cheaper.

Best Motorcycle Breakdown Insurance Providers

| Provider | Best For | Cover Type | Key Features | Best Fit |

| RAC | Large national network | Vehicle / Personal | Fast response times, roadside assistance, recovery, optional home start, optional EU cover | Riders who want a well-known national provider |

| AA | Strong roadside fix rates | Vehicle / Personal | Wide patrol coverage, roadside repair, towing, optional onward travel | Riders who value fast roadside support |

| Green Flag | Competitive pricing | Vehicle / Personal | Home start options, recovery support, flexible plans | Riders looking for lower-cost cover |

| Local SOS Recovery | Emergency one-off help | Pay-per-use | Quick local dispatch, tow service, no membership needed | Riders without active cover or outside policy area |

Motorcycle Recovery Near Me

Use “near me” the smart way

- First choice: open your insurer’s/policy app or call their number—most apps auto-share your GPS so help finds you faster and it stays within your cover.

- If you don’t have cover or you’re out of area: search “motorcycle recovery near me” in Google/Maps. Turn on Location Services, read recent reviews, and pick operators that show 24/7 and clear ETA/pricing.

Call your insurer vs a standalone operator

- Call your insurer/policy app when: you have active motorcycle breakdown insurance, want cashless service, and need extras like onward travel or home start.

- Use a standalone recovery (SOS/pay-per-use) when: you have no policy, your cover excludes the situation (e.g., outside territory), or you need faster local help than your provider can supply right now.

Info to share for quick dispatch

Have this ready (or upload in the app):

- Exact location: pinned GPS link or nearest landmark/road number; direction of travel.

- Safety notes: on hard shoulder/lay-by, blind bend, fuel leak, debris.

- Bike details: make/model/plate, fault description (puncture, dead battery, electrical).

- People & preferences: riders/passengers present, preferred garage or home recovery (if policy allows).

- Policy basics: policy number and name (if using insurance).

Safety checklist while you wait

- Get to a safe place: move off the live lane if possible; stand well away from traffic (behind a barrier if there is one).

- Be seen: switch on hazards/parking lights; wear hi-viz/reflective if you have it; at night, keep lights/torch visible.

- Triangle substitute: many bikes don’t carry one; only place a warning device if it’s safe and legal (never on fast roads where it puts you at risk).

- Stay alert: keep your helmet/gloves on near traffic; don’t smoke around fuel smells; keep your phone charged and location on.

- Share status: send your live location to a friend/family member until recovery arrives.

SOS Motorcycle Recovery — When to Use It

What it is:

On-demand recovery you book by phone/app. No membership needed. A local operator is dispatched quickly; you pay a one-off fee for the call-out, roadside fix (if possible), or tow.

Pros

- Immediate help without a full policy or sign-up.

- Good when your policy has lapsed, you’re out of area, or your bike isn’t eligible under your cover.

- Simple pricing: pay-per-use with an upfront quote and ETA.

Cons

- Higher one-off cost than an insured call-out (especially nights/weekends).

- Often limited to tow-only and basic fixes; little or no onward travel (taxi/hotel/hire) included.

- Usually, no reimbursement unless your insurer explicitly allows out-of-network claims.

How it fits with motorcycle breakdown insurance

- Treat SOS as a backup: use it if insurer wait times are long, you’re outside your policy territory, you’ve hit call-out limits, or your cover excludes the situation.

- Keep receipts—some policies may consider partial reimbursement for emergency out-of-network recovery (check your terms).

- Quick rule: Have cover? Call your insurer first. No cover or out of area? SOS pay-per-use is the fastest path.

Personal Breakdown Cover vs Vehicle-Based Cover

Personal breakdown cover

- Covers you on any bike you ride (and often when you’re a passenger).

- Great if you switch bikes, borrow/rent, or share rides.

- Usually costs more than a single vehicle policy, but replaces multiple policies.

Vehicle-based cover

- Covers one named motorcycle, whoever rides it (within policy rules).

- Often cheaper if you mainly use a single bike.

- Some providers let you add named riders for a fee.

Which one fits your riding?

- Commuters: If you ride the same bike daily, go vehicle-based. If you occasionally use different bikes, choose personal.

- Tourers: If you might rent or ride a friend’s bike on trips, pick personal (add European breakdown cover if travelling abroad).

- Multi-bike owners: Personal is usually simpler and better value than insuring each bike separately (unless your provider offers a strong multi-bike bundle).

- Pillion riders: If you’re often a passenger on different bikes, personal gives consistent cover regardless of the vehicle.

European Breakdown Cover (For Tours & Track Days)

What it is: Add-on cover that helps you abroad—roadside repair, recovery, and onward travel in named European countries.

Where it applies & trip length caps

- Policies list eligible countries (often “zones” like EU/EEA/Schengen/others). Only those listed are covered.

- Each policy sets trip limits (e.g., max 30–90 days per trip, plus an annual cap). Check both the single-trip and total days allowed.

Documents & support abroad

- Carry: policy number, 24/7 assist number, passport/ID, bike registration/title, and your motor insurance papers.

- Many providers offer language support/translation on the hotline. Ask if they can speak to a local garage on your behalf.

- Repatriation: If the bike can’t be fixed locally within a set time or before your return date, they may ship it home—subject to cost vs bike value and distance rules.

- Parts delays: Policies may cover accommodation/hire car while you wait, up to daily limits. Shipping parts is not always guaranteed.

Ferries, tunnels & multi-country rides

- You’re typically covered at ports/terminals; repairs on a ferry/train aren’t possible, but assistance starts once disembarked.

- If you ride through several countries, confirm your policy covers every country on your route and allows cross-border recovery (some tow only to the nearest suitable garage in the current country).

- Night/weekends/public holidays: Garages may be closed; expect tow to secure storage until the next working day.

Seasonal surcharges & exclusions

- Prices/response times can vary in peak summer or harsh winter periods.

- Common exclusions: off-road/unmade tracks, commercial use, and track days/racing. For circuits, you usually need specialist track-day recovery (standard European breakdown cover won’t apply).

Quick prep checklist: Confirm country list, trip length, tow/repat limits, onward-travel caps, and exclusions (especially off-road and track days). Keep all receipts for any claim.

Cost & Value — Cheap vs Comprehensive

When a budget plan works

- You ride short commutes on familiar routes.

- Your bike is newer and well-maintained (lower fault risk).

- You mostly need roadside fixes + short tows to the nearest garage.

- You don’t travel far from home and rarely ride in winter.

When to upgrade

- Older bike, high mileage, or known electrical/starting issues.

- Touring or long trips (consider European breakdown cover).

- Winter riders or rural areas with longer patrol ETAs.

- You want home start and strong onward travel (taxi/hotel/hire).

Hidden costs to watch

- Tow overage: per-mile charges beyond the included recovery distance.

- Second recovery on the same incident (often not covered).

- Diagnostic limits: labour beyond the roadside cap.

- “No-fault found” fees or out-of-hours storage at garages.

- Parts/fluids (tubes, batteries) and misfuel drains.

- Key/lock assistance caps and admin/excess fees.

Buying Checklist (Copy-Paste)

- Coverage type: Vehicle-based or personal breakdown cover.

- Who’s covered: You, named riders, pillion? Age/ID rules.

- Territory: UK/national area; add European breakdown cover if needed.

- Recovery rules: Tow distance included; nearest suitable vs chosen garage.

- Home start: Call-outs from home/driveway included? Any radius limits?

- Onward travel: Taxi/hire car or bike/train/hotel; daily caps and claim process.

- Call-out cap: Number of call-outs per year; fair-use rules.

- Labour limits: Minutes/hours covered at roadside; what happens after.

- Tyre/puncture help: Plug/repair or transport only; tube/spoke exclusions.

- Battery help: Jump-start only or replacement pathway/costs.

- Fuel/misfuel: Drain/refuel covered? Caps and conditions.

- Keys/locks: Lost/snapped key assistance; cost limits.

- Vehicle eligibility: CC/weight/sidecar/modified bikes allowed?

- Exclusions: Accidents, track days/off-road, commercial use, pre-existing faults.

- App & tracking: Live ETA, location share, digital documents.

- Multi-bike/family: Discounts, add-a-bike/rider pricing.

- Waiting period: Any “no immediate call-out” rule after joining.

- Costs & fees: Excess, admin, tow overage, storage.

- Payments: Annual vs monthly; cancellation and refunds.

- Renewal terms: Auto-renew? Loyalty offers? Price-rise policy.

- Support quality: 24/7 lines, language help abroad, review scores.

FAQs (People Also Ask)

What does motorcycle breakdown insurance cover and not cover?

It usually covers roadside help, towing/recovery, optional home start, onward travel, and (with an add-on) European assistance. It normally doesn’t cover accident damage, routine servicing/wear-and-tear, track use, or pre-existing faults—check your policy wording.

Is personal breakdown cover worth it if I ride more than one bike?

Often yes. Personal cover protects you on any bike (and sometimes as a passenger), which can be better value than insuring multiple bikes separately. Compare prices and call-out limits before you choose.

How fast is motorcycle recovery near me on average?

ETAs vary by provider, traffic, time of day, and your location. Use your insurer’s app/phone line for a live ETA; urban areas tend to be quicker than rural routes.

Can I use SOS Motorcycle Recovery if I already have insurance?

Yes—treat it as a backup if you’re out of area, your policy excludes the situation, or the wait is too long. Keep receipts; some insurers may reimburse part of an out-of-network recovery if your terms allow.

Do I need European breakdown cover for a weekend trip?

If you’re crossing into listed EU/EEA countries—even for a short weekend—you typically need European breakdown cover. Domestic weekends don’t require it.

What’s included in RAC breakdown cover for motorcycles?

Typically: roadside assistance, recovery, optional home start and onward travel, plus a European add-on. Exact tow mileage, call-out limits, and eligibility vary by plan—check the RAC terms you’re buying.

Will breakdown cover take me to my chosen garage?

Many policies recover to the nearest suitable garage. Some tiers allow a preferred destination within a mileage cap; beyond that, per-mile charges usually apply.

Does home start cover a dead battery after storage?

Usually yes, if you have home start. Jump-starts are common; replacement batteries and parts are often extra unless stated.

Are punctures and inner tubes covered at the roadside?

Most providers can plug tubeless tyres. Bikes with inner tubes/spoked wheels may need towing to a workshop. Parts and new tyres are typically not included.

Can I add pillion or family members to my plan?

Options vary. Personal cover often protects you on any bike; some vehicle-based plans let you add named riders. Check age/residency rules and any ID requirements.

Disclaimer

This content is general information for riders and not financial or insurance advice. Coverage, limits, eligibility, pricing, and provider features vary by policy and country. Always read the policy documents and terms from your chosen provider before purchasing.