Compare Cherry vs Care Credit for dental financing. Learn how they differ in credit checks, repayment style, provider use, and deferred-interest risk. If you need dental work and cannot pay the full cost upfront, Cherry and Care Credit are two common ways to spread out payments. The better choice depends on what matters most to you. Some people want a softer application process. Others want a reusable credit line they can use again later. These options may look similar at first, but they work in different ways.

The Short Answer

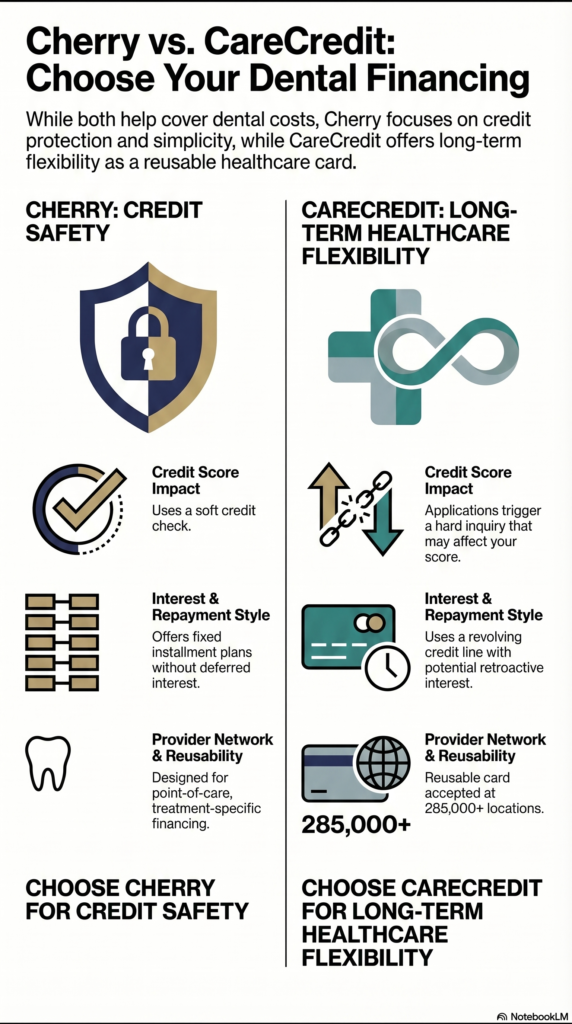

Cherry may be the better option if you want to avoid a hard credit inquiry during application and prefer a more installment-style setup. Cherry says its application uses a soft credit check, not a hard credit check, and says that applying does not impact your credit score. Cherry also says confirmed payment plans typically begin reporting to credit bureaus after 30 days.

Care Credit may be better if you want a reusable health and wellness credit card with a larger provider network. Care Credit says prequalification uses a soft inquiry that does not affect your credit score, but accepting a prequalified offer and applying triggers a hard inquiry that may affect your credit score. Care Credit also says the card has no annual fee and is accepted at more than 285,000 network locations.

How Cherry Works for Dental Financing

Cherry is built around point-of-care financing. Its biggest advantage is the application stage. According to Cherry, patients are prequalified through a soft credit check and not a hard credit check. That can matter if you want to review financing options without adding a hard inquiry to your credit file. The CFPB explains that soft inquiries generally do not affect your credit score, while hard inquiries can.

Cherry may also feel simpler for some borrowers. The company says it offers payment plans with options that can include true 0% APR for qualified applicants, and it says it does not use hidden deferred, retroactive, or compounding interest. That matters because confusing financing terms can turn a low-looking offer into a more expensive one later.

The trade off is flexibility. Cherry is better thought of as treatment-based financing rather than a general reusable card for a large healthcare network. For many readers, that is fine if the goal is to finance one dental bill with a clear repayment path.

How CareCredit Works for Dental Financing

CareCredit works more like a health and wellness credit card. That makes it more flexible if you want one account you may be able to use again for future dental or healthcare expenses. CareCredit says it is accepted at more than 285,000 locations and offers promotional financing options on qualifying purchases.

Its main caution point is the move from prequalification to full application. CareCredit says prequalification itself uses a soft inquiry, but the actual application can trigger a hard inquiry. The CFPB explains that hard inquiries can appear on your credit report and may affect your credit score.

You also need to read the promotional terms carefully. CareCredit says some offers are “no interest if paid in full” promotions. In those cases, interest accrues from the purchase date and can be charged if the promotional balance is not paid in full by the end of the promotion period. That can work for disciplined borrowers, but it is less forgiving if you miss the payoff target.

Cherry vs Care Credit: Key Differences

Credit check

Cherry says its application uses a soft credit check and not a hard credit check. CareCredit says prequalification is soft, but the full application can lead to a hard inquiry.

Repayment style

Cherry is closer to installment financing for a specific treatment. CareCredit is a reusable credit card for eligible health and wellness expenses.

Flexibility

CareCredit is stronger if you want a reusable account across a wider provider network. Cherry is stronger if you want a simpler point-of-care financing path.

Promotional risk

Cherry says it does not use deferred, retroactive, or compounding interest. CareCredit offers promotional financing, so readers need to check whether interest will be charged later if the balance is not paid in time.

Which Option Is Better for You?

Choose Cherry if your top priority is avoiding a hard inquiry at application, keeping the process simple, and reducing the risk of deferred-interest confusion.

Choose CareCredit if your top priority is flexibility, broader provider acceptance, and a reusable account for future care. Just make sure you understand when the process shifts from soft-check prequalification to hard-inquiry application, and read the promotional terms closely.

Frequently Asked Questions

Does Cherry do a hard credit check?

Cherry says its application and prequalification process uses a soft credit check, not a hard credit check.

Does Care Credit affect your credit score?

Checking whether you prequalify does not affect your score, according to CareCredit. But if you accept an offer and apply, CareCredit says a hard inquiry may affect your score.

Is Cherry safer than Care Credit?

Not always. Cherry may be simpler for readers who want clear installment-style financing. CareCredit may be better for readers who want reusable credit and broader provider access. The safer choice depends on the actual terms, fees, and repayment rules you are offered.

What should you compare before choosing?

Look at the credit-check type, APR or promotional terms, fees, credit reporting, and what happens if you miss a payment. The CFPB also explains that hard and soft inquiries are different, so that point matters if you are trying to protect your credit.