Can I Insure a Car Not in My Name?

Usually, you cannot buy a standard car insurance policy on a car that is not in your name. Insurers require “insurable interest” – a real financial stake in the vehicle – so a normal policy needs you to own or co-own the car. But there are legitimate routes, and the right one depends on whose car it is. This guide gives you the exact path for a parent’s, spouse’s, partner’s, friend’s, or company car, plus the claim-time trap that can void your coverage if you do it the wrong way.

Quick answer: Usually, you cannot insure a car that is not in your name unless you have an insurable interest. The safest options are to be added to the owner’s policy, co-title the car, or buy non-owner car insurance if you only need liability coverage.

Key takeaways

- Insurable interest is the rule. You can normally only insure a car you own or co-own, because you must stand to lose money if it is damaged (NAIC).

- The owner’s policy usually comes first. For a car you borrow now and then, the owner’s insurance is primary and covers permissive drivers – so you often need no policy of your own (NAIC).

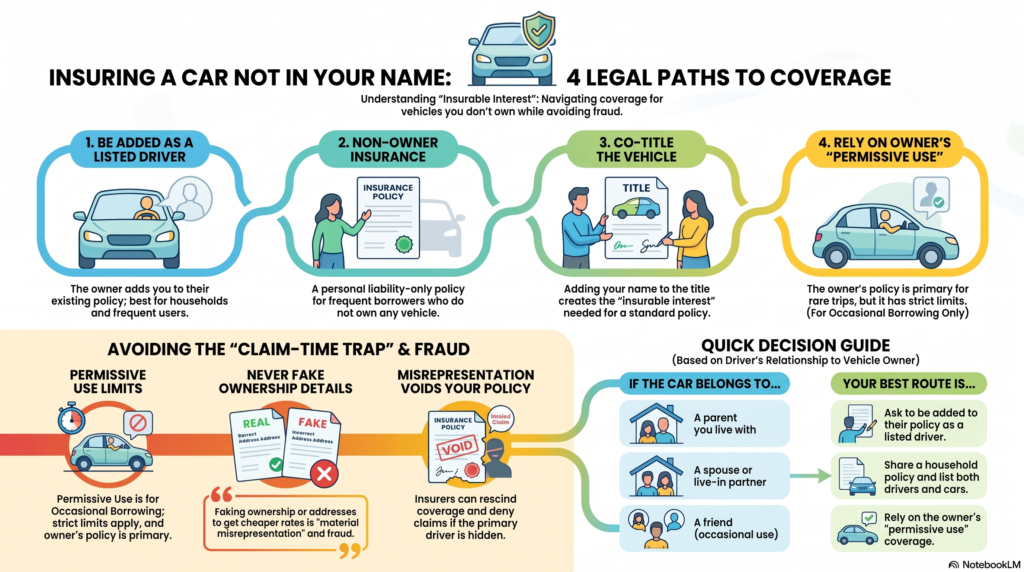

- You have four legit options: be added to the owner’s policy, buy non-owner car insurance, co-title the car, or rely on the owner’s permissive-use cover.

- Non-owner insurance is liability-only. It covers the damage you cause to others, not the car itself, and it will not satisfy a lender.

- Never fake who owns or mainly drives the car. That is a material misrepresentation that can void the policy and count as insurance fraud (NAIC).

Why insurable interest usually stops you

Insurable interest is a core insurance principle. The NAIC explains that the insured must suffer some loss or harm if the insured event happens – the rule exists to prevent gambling and to reduce the temptation to cause a loss. In plain terms: you cannot insure something you have no financial stake in.

For cars, that stake normally comes from being on the title. If you are not an owner, most insurers will not sell you a standard policy on the vehicle, because you would have nothing to lose if it were wrecked. That is why the fix is almost always about ownership (get on the title) or about the driver (get added to the owner’s policy) – not about buying your own policy on someone else’s car.

Quick decision guide

Use this quick rule to find your route:

- Do you own or co-own the car? Buy a standard policy in your name.

- Do you drive a family member’s car regularly? Ask to be added to their policy as a listed driver.

- Do you only borrow cars now and then? The owner’s policy usually covers you as a permissive driver.

- Do you drive but own no car of your own? Consider non-owner car insurance for your own liability.

Your four options (decision table)

There is more than one legitimate way to be covered when the car is not in your name. Here is how they compare.

| Option | What it is | Best when | Covers the car itself? | Rough cost |

| Get added to the owner’s policy | The owner lists you as a rated driver | You live with the owner or drive their car regularly | Yes – under the owner’s coverage | Often the cheapest route; may raise the owner’s premium |

| Non-owner car insurance | Your own liability-only policy for cars you do not own | You borrow or rent cars, have no car of your own, or need an SR-22 | No – liability only | Usually lower than a full policy (no physical-damage cover) |

| Co-title the car | Add your name to the title so you have insurable interest | You are the main driver but not currently an owner | Yes – you can then buy full coverage | A standard policy in your name |

| Rely on the owner’s permissive use | Borrow occasionally; the owner’s policy is primary | Rare, occasional borrowing | Yes – the owner’s policy pays | Free to you; the owner insures the car |

Non-owner car insurance is a real product: the III notes that people who do not own a car but drive borrowed or rented vehicles can buy a non-owner liability policy for the liability protection they need. Just remember it does not pay to repair the car you are driving – only the damage you cause to others.

The exact route for each situation

The best answer depends on whose car it is. Find your situation below.

| Whose car is it? | Can you put your own policy on it? | The right route |

| A parent’s car you live with | Not usually | Ask your parent to add you to their policy as a listed driver. If you are the main driver, you must be listed as the primary driver – do not hide it. |

| A parent’s car after you move out | Not usually | Either stay listed on their policy with your correct address and driver status, or transfer/co-title the car so you can insure it yourself. |

| A spouse’s car | Often yes | Most insurers let married couples share a household policy. Put both cars on one policy and list both drivers. |

| A partner’s or girlfriend’s/boyfriend’s car | Sometimes | If you live together, some insurers let you be added as a driver or co-insure. Otherwise, be added to the owner’s policy, co-title the car, or use non-owner insurance for occasional driving. |

| A friend’s car | Usually not needed | The friend’s policy is primary and covers you as a permissive driver for occasional use. For frequent driving, ask to be added as a listed driver, or get non-owner insurance for your own liability. |

| A company car | No (you are not the owner) | The employer’s commercial auto policy covers business use. For personal use or gaps, non-owner insurance can help – you cannot put a personal policy on a company-owned car. |

| A car you are buying but have not titled yet | Yes, once you are the buyer | You gain insurable interest as the buyer. Put the title/registration in your name and insure it before you drive it – if it is financed, the lender will require you (the owner) to carry coverage. |

Answers for common situations

Can I insure my girlfriend’s or boyfriend’s car?

Usually only if you live together or you are added to the owner’s policy. If you share a home, some insurers let you be listed as a driver or co-insure the car; otherwise use non-owner insurance for occasional driving, or co-title it. Example: You live with your partner and drive her car twice a week. The clean route is to be added to her policy as a listed driver.

Can I insure a car registered to my parents?

You normally insure it through your parents, not on a separate policy of your own. If you live with them or drive the car, ask to be added as a listed driver – as the primary driver if that is you. Example: You live at home and drive your parents’ car daily. The best route is to be added to their policy as the primary driver on that car.

Can I insure my friend’s car?

Usually, you do not need to. Your friend’s policy is primary and covers you as a permissive driver for the odd trip. For regular driving, ask to be added as a listed driver, or buy non-owner insurance. Example: You borrow a friend’s car about once a month. Their policy’s permissive-use cover normally protects you – no separate policy needed.

Can I insure a company car in my name?

No. You do not own a company car, so you cannot put a personal policy on it. The employer’s commercial auto policy covers business use; non-owner insurance can cover your own liability when you drive other cars.

What is non-owner car insurance?

Non-owner car insurance is a liability-only policy for people who drive but do not own a car – for example, frequent renters or borrowers. It pays for injury or damage you cause to others, but it does not repair the car you are driving and will not satisfy a lender.

Can I insure a car if I am not the registered owner?

Generally, not with a standard policy, because you lack insurable interest. Your realistic routes are to be added to the owner’s policy, to co-title the car so you become an owner, or to use non-owner insurance if you only need liability. Example: You bought a car but the title is still in your father’s name. Transfer or co-title the vehicle first, then buy your own standard policy. If you are financing it, compare your loan first – see dealer vs bank financing and how long a car loan should be.

The claim-time trap: never fake ownership or the main driver

This is the part the quote-and-sign websites skip. If you register or insure a car under someone else’s name just to get a cheaper rate, or you hide who the real main driver is (sometimes called “fronting”), you are making a material misrepresentation to the insurer.

The NAIC is blunt about the consequence: when an insurer discovers a material misrepresentation, it can rescind the policy – treat it as void from the start – so there is no claim to pay. That usually surfaces at the worst possible moment: after a crash, when the insurer investigates and finds the details do not match. On top of a denied claim, misstating facts to get insurance can count as insurance fraud, which is a crime in every state.

So, the rule is simple: whatever route you choose, keep the owner, the address where the car is kept, and the main driver accurate on the policy. A slightly higher honest premium is far cheaper than a denied claim.

Mistakes to avoid

- Do not hide the real main driver. Listing the wrong primary driver is a misrepresentation.

- Do not use someone else’s address to get a cheaper quote – insurers verify where the car is kept.

- Do not assume borrowed-car coverage is unlimited. Permissive use has limits, and some policies exclude regular drivers who are not listed.

- Do not buy non-owner insurance if you need to protect the car itself – it is liability only.

- Do not ignore a lender’s insurance rules. If the car is financed or leased, the lender requires full coverage in the owner’s name.

When should you call the insurance company?

Call the insurer (or the owner’s insurer) before you drive the car regularly if:

- the car is not registered in your name;

- you live with the owner;

- you are the main driver of the car;

- the car is financed or leased;

- you use the car for work;

- you have recently moved to a new address.

A quick call to confirm how you are covered is free – a denied claim is not.

How much does it cost?

Costs depend on the route. Being added to the owner’s policy as a driver is often the cheapest option, though it can raise the owner’s premium if you are a higher-risk driver. Non-owner car insurance is usually cheaper than a full policy because it is liability-only and does not cover any vehicle’s repair. Co-titling and taking your own full policy cost the most, because you are buying complete coverage.

Prices vary widely by state, your driving record, and your age, so get quotes for the specific route before you decide. We have avoided quoting a single national figure here because it would be misleading – your number will depend on your own profile.

How to insure a car that is not in your name, step by step

- Confirm who owns the car by checking the title and registration.

- Match the route to your situation using the tables above.

- If you drive it regularly, ask the owner to add you as a listed driver – as the primary driver if that is you.

- If you have no car of your own, price a non-owner policy for your personal liability.

- If you are really the owner-in-waiting, get on the title (or co-title), then buy your own policy.

- Keep every detail honest – owner, garaging address, and main driver.

- Get quotes for your exact route and confirm state rules with your insurer or DMV.

Frequently asked questions

Can I insure my girlfriend’s or boyfriend’s car?

Usually only if you have an insurable interest or are added to her or his policy. If you live together, some insurers let you be added as a driver or co-insure the car. Otherwise, ask to be listed on the owner’s policy, co-title the car, or use non-owner insurance for occasional driving.

Can I insure a car registered to my parents?

Generally, you insure it through your parents, not with your own separate policy. If you live with them or drive the car, ask to be added as a listed driver (as the primary driver if that is you). If you have moved out and it is really your car, transfer or co-title it so you can insure it yourself.

Can I insure a company car in my name?

No. You do not own a company car, so you cannot put a personal policy on it. The employer’s commercial auto policy covers business use. If you also drive it personally, or drive other cars, non-owner insurance can fill gaps in your own liability.

Can I insure a friend’s car?

Usually, you do not need to. Your friend’s policy is primary and covers you as a permissive driver for occasional use. If you drive it often, ask to be added as a listed driver, or buy non-owner insurance for your own liability.

How much does non-owner car insurance cost?

It varies by state, age, and driving record, but it is typically cheaper than a full policy because it only provides liability coverage and does not cover a vehicle’s repair. Get a quote for your own profile rather than relying on an average.

Is it illegal to insure a car that is not in your name?

Insuring a car you co-own or being added to the owner’s policy is fine. What is illegal is misrepresenting the facts – for example, registering or insuring a car under someone else’s name, or hiding the real main driver, to get a lower rate. That can void your policy and count as fraud.

Can two people insure the same car?

Two people who both have an ownership interest (co-owners on the title) can be on the same policy, and both can be listed drivers. Two separate policies on one car from different people is not standard and can cause claim disputes – insure it once, correctly.

Before you buy or finance a car

Insurance is one piece of buying a car. If you are also arranging the loan, read our guides on dealer vs bank financing, how long a car loan should be, and what APR really means before you choose your insurance route.

About the author

This article was written by Nimra Saleem for MoneyMentorDesk.com and reviewed against official consumer-insurance resources from the NAIC and the Insurance Information Institute (III) on July 8, 2026. It is intended for general education and should not replace advice from a licensed insurance agent or your state DMV. Insurance rules vary by state and change over time.

Educational only – not insurance or legal advice. Confirm your options with the vehicle owner, your insurer, and your state DMV before acting.

Final source audit

Status: Fully source-verified. Every insurance rule is drawn from the III or the NAIC and checked on July 8, 2026. No premiums, averages, or state-specific figures were invented; cost is described in relative terms only. The scenario routes apply the verified rules to common relationships and are framed as general guidance, not a guarantee for any state or insurer. The article carries an educational-only disclaimer, a named author, a reviewed-against-sources line, and a last-updated date.