Can You Get Car Insurance Without a License?

Yes, you can get car insurance without a driver’s license. Many insurers will cover a car if you list a licensed person as the main driver. This is common for people with a suspended license, a learner’s permit, a health condition, or a car that someone else drives. But you usually cannot legally drive the car yourself until you are licensed.

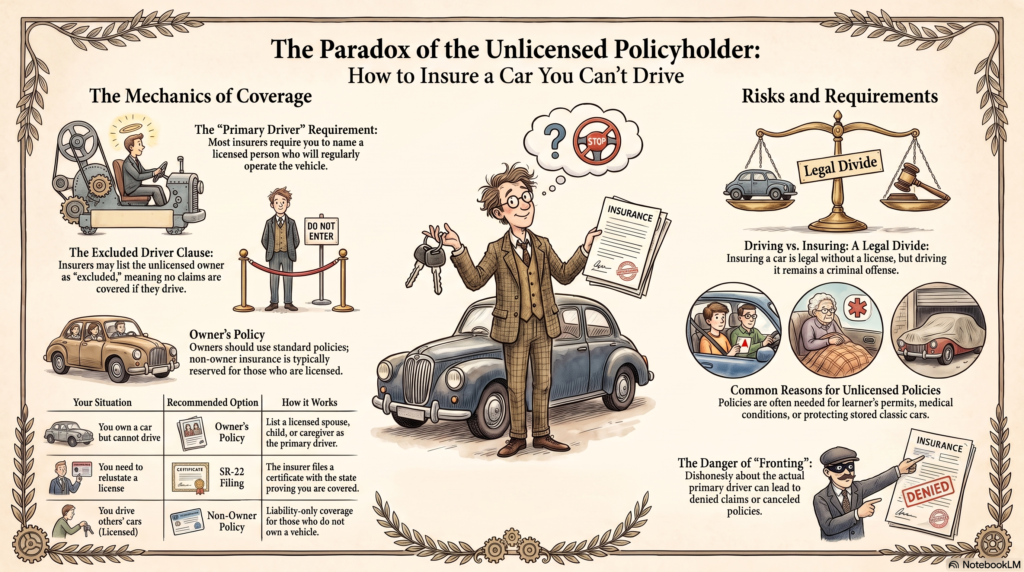

Quick answer: You can buy a policy without a license, but most insurers will ask you to name a licensed “primary driver,” and some states require at least one licensed driver on the policy. Insurance is about the car and who drives it, not just about you.

Last updated: 14 July 2026 Reviewed against sources: Insurance Information Institute (III), California DMV, and Progressive (official provider guidance). Author: Nimra Saleem. This guide is fact-checked against official sources. It is educational only and is not reviewed by a licensed insurance agent.

Key takeaways

- You can get car insurance without a license, but you may have to name a licensed main driver, and some states require one on the policy.

- Non-owner car insurance is a liability policy for people who drive but do not own a car. It is usually meant for licensed drivers.

- It is still illegal to drive without a valid license, even if the car is fully insured.

- If you drive unlicensed and cause a crash, your insurer may deny the claim, leaving you to pay out of pocket.

- Common reasons to insure a car without a license: a suspended license, a learner’s permit, a health condition, a teen under 18, or a car someone else drives.

How car insurance works when the owner is unlicensed

It is possible to buy car insurance without a driver’s license, and if someone other than you will drive the car, it is often necessary. Some insurers are cautious about covering a policyholder with no license, so you may need to shop around. Many will simply ask you to list a licensed person as the main driver on the policy.

Here is the key idea: coverage is generally attached to the insured vehicle, while the insurer also evaluates the people who regularly drive it. The exact coverage depends on the policy, driver status, and state rules. So, a car can be insured even if its owner does not drive. What an unlicensed vehicle owner generally cannot do is drive that car themselves without a valid license.

How do you buy car insurance without a driver’s license?

Most insurers ask for a driver’s license number so they can check driving history and set a price. If you do not have a license, the insurer will usually ask for the license number of the person who will actually drive the car the most. That person is the primary driver, and their record helps set your rate. Progressive’s guidance on buying car insurance without a license explains that some companies let you name a licensed primary driver, while others will not, so it pays to compare.

There are three common ways to get covered:

| Your situation | Best option | How it works |

| You own a car but do not drive it | Owner’s policy with a licensed main driver | You are the policyholder; a licensed spouse, child, or caregiver is listed as the primary driver. |

| You do not own a car but sometimes drive others’ cars | Non-owner car insurance | A liability-only policy in your name. Usually meant for licensed drivers. |

| You need to prove insurance to the state (for example, to reinstate a license) | Policy with an SR-22 filing | Your insurer files a form with the state showing you carry at least the minimum coverage. |

The insurer may also list you as an excluded driver. That means the company will not cover any claim if you drive the car. It is a way for the insurer to cover the vehicle while making clear you are not a rated driver on it.

Does non-owner car insurance work without a license?

Non-owner car insurance is a liability policy for people who do not own a car but sometimes drive one, such as a borrowed or rented vehicle. It pays for injury or damage you cause to others while driving a car you do not own. It does not cover the car itself, and it does not include comprehensive or collision cover.

The Insurance Information Institute notes that people who do not own a car but rent often can buy a non-owner liability policy for the extra protection they need. These policies are generally designed for licensed drivers who do not own a vehicle. They are also a common way to keep continuous coverage or to file an SR-22 while you do not own a car.

So, a non-owner policy is usually the wrong fit if you have no license at all. If you have no license and you own the car, the more usual route is an owner’s policy that names a licensed primary driver.

Why would someone need car insurance without a license?

There are several everyday reasons to insure a car when the owner is not a licensed driver. In each case, insurance protects the car and the licensed person who actually drives it.

- Your license is suspended. You may not be driving for a while, but keeping continuous coverage helps you avoid a price jump later. States usually want to see proof of insurance before they will reinstate your license.

- You have a learner’s permit. If you are learning to drive, you need insurance in place before you get behind the wheel.

- A health condition stops your driving. A caregiver or family member may drive you to appointments and run errands in your car.

- Your teen drives but is under 18. In most states you must be 18 to sign a contract, so a parent buys the policy and lists the licensed teen as a driver.

- Someone else drives your car. A spouse, adult child, or caregiver who does not own the car may be its main driver.

- You own a classic or stored car. You may still need comprehensive insurance to protect a stored vehicle against theft, fire, vandalism, or weather damage, even if no one is driving it right now.

Who should you list as the primary driver?

List the person who will actually drive the car the most. If you are married or have children, that may be your spouse or a licensed adult child. If a health condition keeps you from driving, it may be the caregiver who drives you around. The primary driver’s license and driving record are used to help price the policy.

If ownership and policyholder names are different, read our guide to insuring a car that is not in your name to see how the owner, the policyholder, and the listed driver can all be different people.

Be honest about who the main driver is. Naming a low-risk person to get a cheaper price when a higher-risk person really drives the car is sometimes called “fronting.” If the insurer finds out, it can deny a claim or cancel the policy. Getting the main driver right protects your coverage.

Can you insure a car and not drive it yourself?

Yes. Your car can be fully insured even if you never get behind the wheel. A standard auto policy covers you and family members on the policy, and it also covers other people who drive your car with your permission (this is called permissive use, as the Insurance Information Institute explains). So, a licensed friend or relative can be your main driver while you remain the vehicle owner and policyholder.

Remember that in nearly every US state, a registered car must be insured. In California, for example, the state DMV requires insurance on all vehicles operated or parked on public roads, and it can suspend the registration if proof of insurance is not on file. If the vehicle is financed, the lender may require full coverage on a financed car, even when the owner does not drive it. Auto insurance is mandatory in every state except New Hampshire, so always check your own state’s rule.

What is an SR-22 and do you need one?

An SR-22 is not a type of insurance. It is a form your insurer files with the state to prove you carry at least the minimum required coverage. California, for example, calls it the California Proof of Insurance Certificate (SR 22). States often ask for one after events such as a DUI, driving while uninsured, or to reinstate a suspended license.

A few things to know:

- You do not buy an SR-22 by itself. You ask an insurer to add it to a policy, and the insurer files it with your state.

- If you do not own a car, you can often file an SR-22 on a non-owner policy.

- How long you must keep the SR-22 on file varies by state (a period of a few years is common). Check your own state’s DMV for the exact rule.

The risks of driving without a license

Insuring a car without a license is legal. Driving one without a valid license is not. This is the part that trips people up, so it is worth being clear.

Driving without a valid license can lead to fines, penalties, and in some places even jail time. Police may impound the vehicle, and repeat offenses can bring longer suspensions and steeper penalties. A conviction can also make it harder to get or regain your license later, and can push your insurance rates up.

There is a coverage risk too. If you cause an accident while driving unlicensed, your insurer may deny the claim. That could leave you personally responsible for repair costs, medical bills, and any liability claims from the other party. In short: insure the car, but do not drive it until you are properly licensed.

How much does car insurance without a license cost?

There is no single price, and no honest guide can quote you an exact number, because rates depend on your state, the car, and the main driver’s record. As a general rule, expect to pay based on the licensed primary driver you list. If that driver has a clean record, the price is usually lower. If they have tickets or at-fault crashes, you will likely pay more.

If cost is a worry, some states run low-cost programs. California, for example, has a state Low Cost Automobile Insurance Program for drivers who meet the rules. Check whether your own state offers something similar, and always compare quotes from more than one insurer, since some are far more willing than others to cover a policy with no licensed policyholder.

Frequently asked questions

Can I get car insurance without a license?

Yes, though it depends on the insurer and your state. You can buy a policy without a driver’s license, but most insurers will ask you to name a licensed main driver, and some states require at least one licensed driver on the policy. Some companies will not write a policy unless the policyholder is licensed, so you may need to shop around. Either way, you can insure the car; you just cannot legally drive it yourself until you are licensed.

Can I insure a car that is only driven by someone else?

Yes. Your car can be insured with a licensed relative, spouse, or caregiver as the main driver. A standard policy generally covers drivers listed on the policy and may cover occasional permissive drivers, subject to its terms. Household members who regularly drive the car should be disclosed to the insurer and normally listed on the policy.

Do I need a license to buy non-owner car insurance?

Non-owner car insurance is generally designed for licensed drivers who do not own a car. If you have no license and you own the vehicle, an owner’s policy with a licensed primary driver is usually the better fit.

Will I pay more for car insurance without a license?

Possibly. Your rate is based mainly on the licensed primary driver you list and their record, plus your state and vehicle. A clean-record driver usually means a lower price.

Can I drive my own insured car without a license?

No. Even if the car is fully insured, driving without a valid license is illegal and can bring fines, impound, or worse. If you crash while unlicensed, the insurer may also deny the claim.

Do I need insurance to get my license back after a suspension?

Usually yes. States generally want proof of insurance, and sometimes an SR-22 filing, before they reinstate a suspended license. Keeping continuous coverage can also help you avoid a big price jump.

Educational disclaimer

This article is for general education only. It is not financial, legal, or insurance advice, and it is not reviewed by a licensed insurance agent. Insurance rules, minimum coverage, financial responsibility laws, and SR-22 requirements vary by state and by insurer. The California examples above are examples only and are not nationwide rules. Before you buy or cancel a policy, confirm the details with a licensed insurer or your own state insurance department. You can find yours through the NAIC state insurance department directory.

Sources

- Insurance Information Institute – What is auto insurance? (coverage basics, permissive use, mandatory in all states except New Hampshire)

- California DMV – Insurance Requirements (insurance required on vehicles operated or parked, minimum limits, SR-22 as proof of insurance, Low Cost Automobile Program)

- Progressive – Can you get car insurance without a license? (naming a primary driver, excluded driver, reasons to insure, risks of driving unlicensed)

- NAIC – State Insurance Department directory (find your state regulator to confirm local rules)

Source-verified status

FULLY SOURCE-VERIFIED. Every factual claim is tied to III, California DMV, or Progressive (official provider). No rate, APR, or price is stated as fact; cost is framed as general guidance. California statements are labeled as examples, not nationwide rules.