Is GAP Insurance Worth It?

Last updated: July 12, 2026 – fact-checked against official sources from the CFPB and the Texas Department of Insurance.

GAP insurance is worth it when you owe more on your car loan than the car is worth – which is common if you put down less than 20%, financed for 60 months or more, bought new, or rolled old debt into the loan. If your car is totaled or stolen, standard insurance only pays the car’s current value, and GAP is designed to cover the eligible difference on your loan. If you already have equity, it is not worth it. This guide shows two numerical examples, who needs it, where it is cheapest, and how to cancel and check for a refund.

Quick answer: GAP insurance is worth it if you could end up “upside down” – owing more than the car is worth – so a total loss would leave you paying off a car you no longer have. Skip it, or cancel it, once you owe less than the car’s value.

Key takeaways

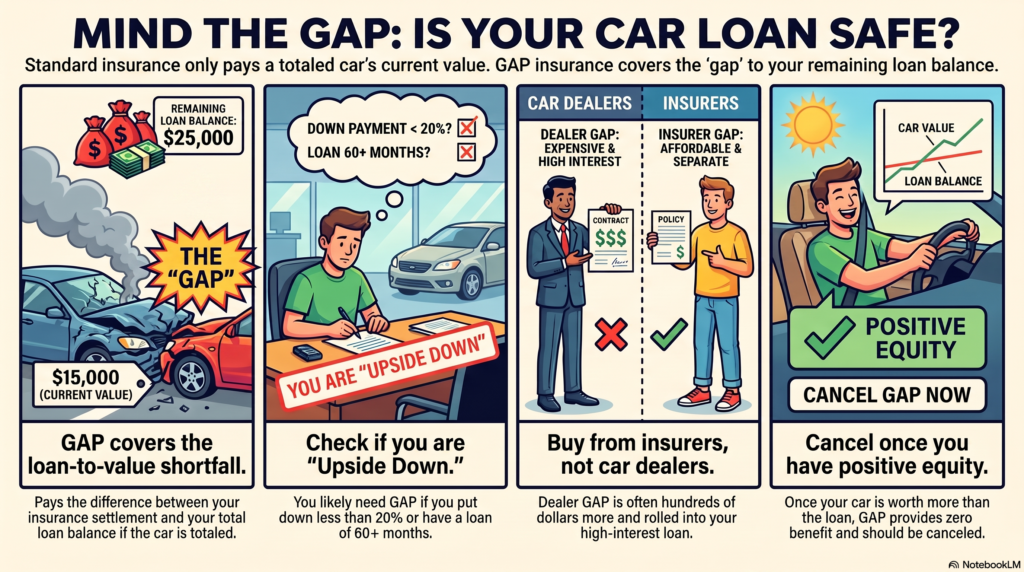

- GAP covers the “gap” between your loan balance and what your insurer pays if the car is totaled or stolen, subject to the contract’s limits and exclusions (CFPB).

- You likely need it if your down payment was under 20% or your loan runs 60 months or more – that is when the gap gets large (Texas TDI).

- Where you buy it changes the price. Your own insurer usually adds a small amount to your premium; a dealer usually charges a larger one-time fee rolled into your loan, so you pay interest on it too.

- Dealer or bank GAP may not be regulated insurance – it is often a “GAP waiver,” which changes who can help if there is a problem (Texas TDI).

- You can cancel any time and may qualify for a refund of the unused portion if you sell, refinance, or prepay the loan (CFPB).

What is GAP insurance?

GAP insurance is an optional product that pays the difference between what you owe on your auto loan and what your insurer pays if the car is stolen or totaled. Standard auto insurance only pays up to the car’s current value (its “actual cash value”). If your loan balance is higher, GAP is meant to cover the eligible shortfall – within the contract’s limits and exclusions (CFPB).

GAP is one of several add-on products – like extended warranties or credit insurance – that a dealer offers when you buy or lease. Its cost is usually rolled into the loan, so you also pay interest on it, and the CFPB notes it may not provide value for every buyer. “GAP” stands for Guaranteed Asset Protection.

Educational only: This is general information, not insurance or financial advice. Rules and prices vary by state and provider. Confirm the details with your insurer, lender, or state insurance department before you buy or cancel.

Example: how a GAP claim could work

Numbers make it click. Illustration only – your figures will differ.

You buy a new car for $32,000 with a small down payment. A year later, it is totaled in a crash. New cars lose value fast, so your auto insurer pays its current value – say $24,000. But you still owe $27,000 on the loan.

- Without GAP: you must pay the $3,000 difference out of pocket, for a car you no longer have.

- With GAP: the policy is designed to cover that $3,000 eligible gap (minus any deductible or excluded amounts – see below).

Example: when GAP pays nothing

Now flip it. Illustration only. Two years into the loan you owe $21,000, and your insurer would settle a total loss at $23,000. Your eligible gap is $0 – the insurer’s payment already covers the loan, so GAP pays nothing. Once you have positive equity like this, GAP no longer helps, which is your signal to cancel it.

Do you need GAP insurance? A quick self-check

GAP is most worth considering if one or more of these is true (the Texas Department of Insurance flags the first two as the classic warning signs):

- You put down less than 20%.

- You financed for 60 months or more.

- You bought a new car (it loses value fastest in the first years).

- You rolled negative equity from an old car into this loan. (Not sure? See what negative equity is and how to trade in a financed car.)

- You are leasing – many leases require GAP; check your contract.

You probably do not need it if you made a large down payment, took a short loan, or already owe less than the car is worth. A longer loan is the most common reason people stay upside down – see how long a car loan should be.

Do I need GAP if I already have full coverage?

This is a common mix-up. Full coverage usually means you carry collision and comprehensive insurance – but those pay only the car’s current insured value, not necessarily your full loan balance. If your payoff is higher than that settlement, full coverage still leaves a gap. GAP sits on top of your collision and comprehensive cover to pay the eligible difference. So they do different jobs: full coverage protects the car’s value; GAP protects the extra you still owe. For what a lender may require, see our guide on full coverage on a financed car.

Is GAP insurance worth it on a used car?

A used car does not automatically mean you can skip GAP. It can still be worth it when:

- your down payment was small;

- your loan-to-value ratio is high;

- you rolled negative equity into the loan;

- the loan term is long; or

- you paid above the car’s market value.

The test is the same as for a new car: do you owe – or will you soon owe – more than the car is worth?

Where to buy GAP, and what it costs

Price varies a lot, and the CFPB’s advice is simple: compare prices and coverage before you buy. Here is how the three main sources compare.

| Where you buy it | How it is priced | What to expect | Watch-outs |

| Your own auto insurer | A small add-on to your premium | Often only tens of dollars a year – one 2026 cost analysis estimated an average near $88, though it varies by driver, state, insurer, and vehicle | Only if your insurer offers it; usually needs comprehensive and collision cover |

| Car dealer or bank | A one-time fee rolled into your loan | Usually several hundred dollars, plus interest because it is financed | May not be regulated insurance (TDI); it is optional, so you can decline it or ask about the price |

| Credit union or direct lender | One-time or added to the loan | Sometimes lower than the dealer – compare | Still compare against your insurer |

Cost figures are estimates that vary by driver, state, insurer, and vehicle – not a quote. The insurer average is from a 2026 GAP cost analysis, and the CFPB stresses that prices vary greatly, so get your own quotes.

Watch the interest on financed GAP. Illustration only. Say a dealer charges $600 for GAP and you roll it into a 6-year loan at a 7% APR. Because you pay interest on the add-on too, that $600 ends up costing about $735 over the loan – roughly $135 more than paying for GAP separately. See our guide to the total cost of a car loan for how that adds up.

One more rule from the CFPB: if you are told you must buy GAP to get financing, ask to see where the contract says that. If it truly is required, its cost must be included in the finance charge and your disclosed APR. If it is optional, you can decline it.

GAP insurance vs a GAP waiver

Not all “GAP” is the same. A true GAP insurance policy is regulated insurance. But GAP sold by a dealer or lender is often a GAP waiver – a debt-cancellation agreement added to your loan, not an insurance policy. The Texas Department of Insurance warns that dealer or bank GAP products might not technically be insurance, which changes who handles a complaint: your state insurance department may not be able to help with a waiver. Read the paperwork to see which one you have and who to contact if there is a dispute.

What GAP insurance does not cover

GAP is narrower than people expect. The Texas Department of Insurance warns that most contracts have exclusions that can reduce your payout. Common ones:

- Overdue payments you had missed before the loss.

- Unpaid finance charges, extended-warranty costs, or balloon payments.

- Your auto insurance deductible. Some GAP contracts exclude the primary insurance deductible, while others may cover all or part of it – check your agreement.

- Damage from a previous accident that was not repaired.

Read your contract so you know your exclusions before you rely on GAP. And remember: GAP only helps if the car is totaled or stolen – it does nothing for repairs, breakdowns, or everyday claims.

How to cancel GAP insurance and check for a refund

You do not have to keep GAP for the life of the loan.

- You can cancel any time. The CFPB says you have the right to cancel these optional add-on products at any time to reduce your costs.

- Check for a refund. Depending on your contract and state rules, you may qualify for a refund of an unused portion after you sell, refinance, or pay off the loan early (CFPB). Contact your lender, the provider, or the dealer you bought from.

- Know when to cancel. The Texas Department of Insurance says you can usually cancel once you owe less than the car is worth – it notes this often takes around two years, but the right point depends on your vehicle’s value and current loan payoff. Get your exact figure with a 10-day payoff quote.

- If they resist, you can submit a complaint to the CFPB.

To cancel, ask the dealer, lender, or provider for their cancellation form, put the request in writing, and keep a copy.

Quick decision guide

- Do you owe more than the car is worth, or will you soon? GAP is worth considering.

- Small down payment, 60+ month loan, or a new car? Lean toward getting it – but price it at your insurer first.

- Leasing? Check the contract; GAP is often required.

- Already have equity, or paid off / sold the car? Cancel GAP and check for a refund.

Mistakes to avoid

- Buying GAP from the dealer without comparing. Your own insurer is often far cheaper.

- Financing GAP into the loan and forgetting it. You pay interest on it for years, and you may qualify for a refund once you have equity.

- Assuming GAP covers everything. It does not pay for repairs, overdue payments, and may not pay your deductible.

- Keeping GAP too long. Cancel it once you owe less than the car is worth.

- Taking “you must buy GAP to get the loan” at face value. Ask to see it in the contract; if it is required, it must be in your APR (CFPB).

Frequently asked questions

Is GAP insurance worth it on a lease?

Often yes – many leases require GAP, and lease payments can keep you upside down. Check your lease, since the cost may already be built in. If it is not, price it before you sign.

How much does GAP insurance cost?

It varies by driver, state, insurer, and vehicle. From your auto insurer it is usually a small add-on to your premium – one 2026 analysis estimated an average near $88 a year. From a dealer it is usually a one-time fee of several hundred dollars rolled into the loan, so you also pay interest on it. The CFPB says prices vary greatly, so get quotes.

How do I cancel GAP insurance and check for a refund?

Ask the dealer, lender, or provider for their cancellation form and submit it in writing. The CFPB says you can cancel any time and may qualify for a refund of the unused portion if you sell, refinance, or prepay the loan. If they refuse, submit a complaint to the CFPB.

Does GAP insurance cover my deductible?

It depends on the contract. Some GAP agreements exclude your primary insurance deductible, while others may cover all or part of it. The Texas Department of Insurance lists the deductible as a possible exclusion, so read your agreement to be sure.

Is dealer GAP insurance a rip-off?

Not exactly, but it is usually the most expensive place to buy it, and dealer GAP may be a debt-cancellation waiver rather than regulated insurance. Compare your own insurer’s price first, and check the paperwork for who handles complaints.

When should I cancel GAP insurance?

Cancel once you owe less than the car is worth – the Texas Department of Insurance says this often takes around two years, but the right point depends on your car’s value and loan payoff. Cancel right away if you pay off or sell the car.

Before you buy or finance a car

GAP is one small decision inside a bigger one. If you are still arranging the loan, read our guides on dealer vs bank financing, what APR really means, and the total cost of a car loan so you know what you are really paying before you add any extras.

Sources

- CFPB – What is Guaranteed Asset Protection (GAP) insurance?

- CFPB – What can I negotiate when shopping for a car or auto loan?

- Texas Department of Insurance – Gap insurance

- Insure.com – 2026 GAP insurance cost analysis (used only for the average insurer cost estimate)

About the author

Written by Nimra Saleem, who writes plain-English money guides for MoneyMentorDesk.com. This article was fact-checked against official sources from the Consumer Financial Protection Bureau (CFPB) and the Texas Department of Insurance (TDI) on July 12, 2026. It was not reviewed by a licensed insurance professional and is general education only. It should not replace advice from a licensed insurance agent, your lender, or your state insurance department. Rules and prices vary by state and change over time.

Educational only – not insurance or financial advice.