Prequalified vs Preapproved Car Loan: What’s the Difference?

Key takeaways

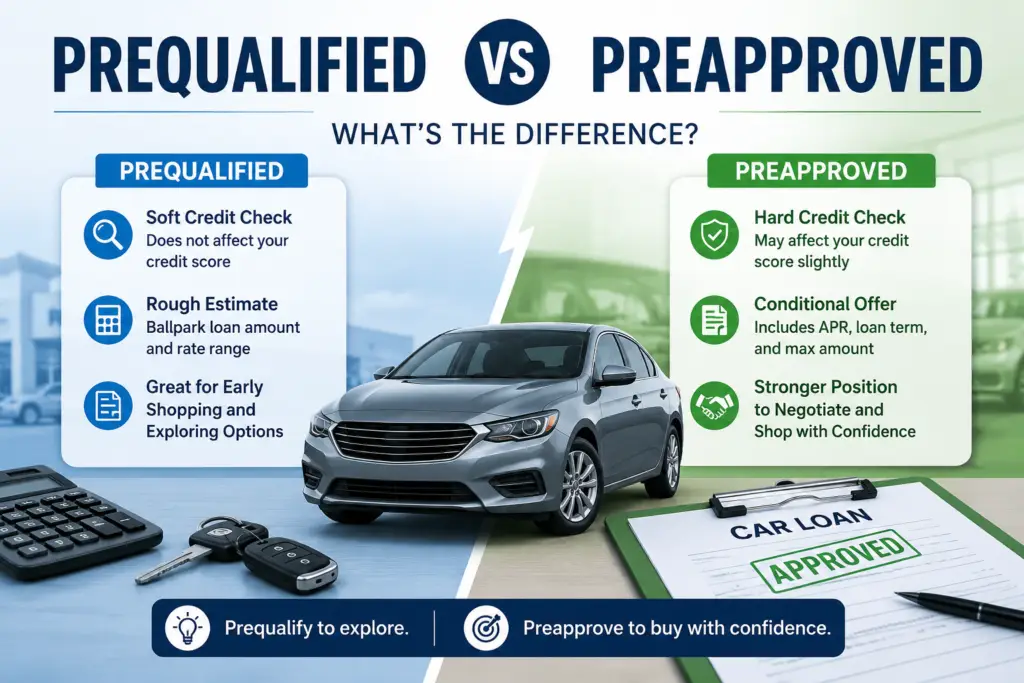

- Prequalified means a lender gives you a rough estimate of what you might borrow. It uses basic info and a soft credit check. A soft check does not affect your score. It is not a promise to lend.

- Preapproved is stronger. The lender reviews your credit, often with a hard credit check. Then it makes a conditional offer with an APR, loan term, and maximum amount. You can use that offer to negotiate.

- A soft check doesn’t hurt your credit. A hard check can lower your score a little. The CFPB says auto-loan checks made within 14 to 45 days usually count as one inquiry. So you can shop several lenders safely.

- Neither one guarantees the final loan. The lender still has to verify your details and the car before the deal is final.

- Lenders use these words differently. So ask one thing: is it a soft or hard credit check? Also ask if the offer shows your real APR, term, and amount.

Prequalified vs preapproved car loan: what’s the difference?

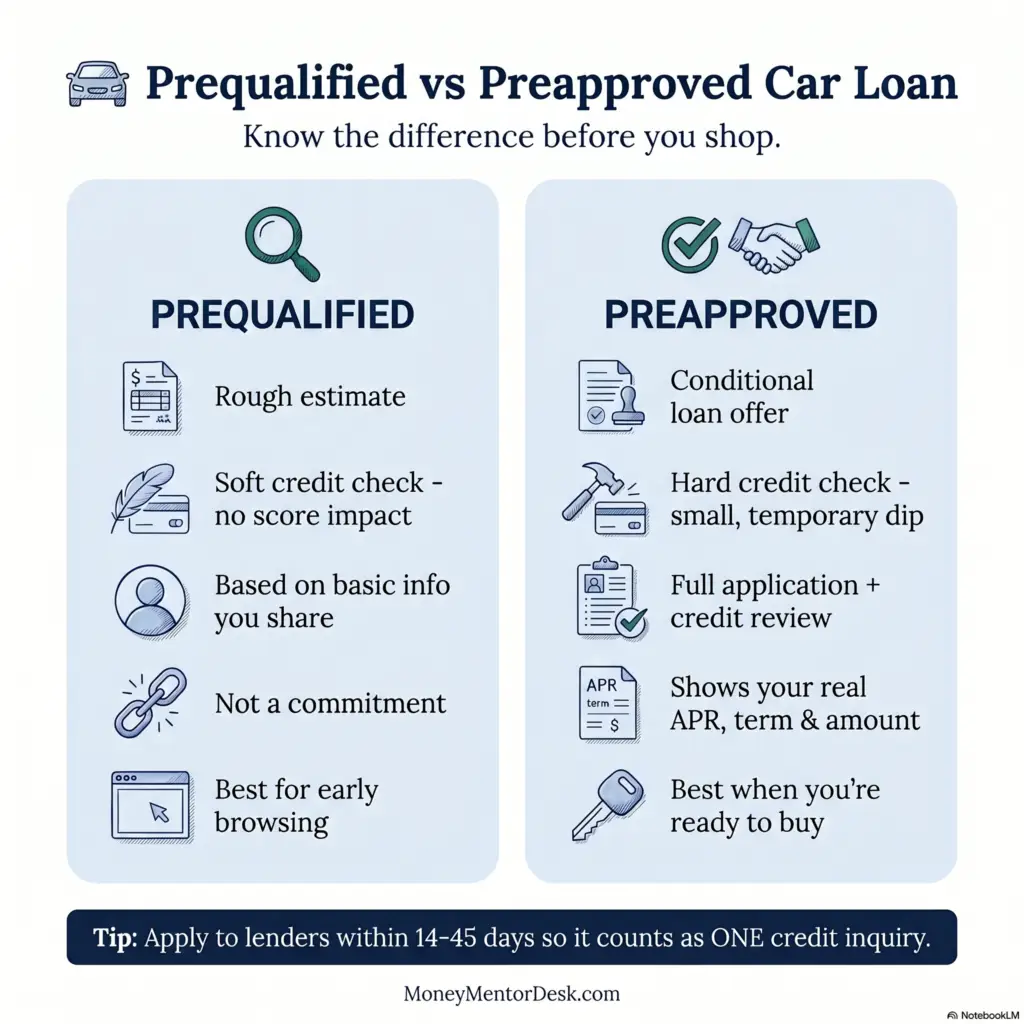

A car loan prequalification is an early estimate of what you might borrow. It uses the info you share and a soft credit check, so it doesn’t affect your score. A preapproval is stronger. The lender reviews your credit, often with a hard check, and makes a conditional offer. That offer shows your likely APR, term, and loan amount.

In short: prequalification helps you explore, and preapproval helps you buy. Here is how they compare.

| Feature | Prequalified | Preapproved |

| What it is | A rough estimate | A conditional loan offer |

| Credit check | Usually a soft inquiry | Often a hard inquiry |

| Effect on credit score | None (soft check) | Small, usually temporary |

| Info the lender uses | Basic, often self-reported | A full application and credit review |

| What you get | A ballpark amount and rate range | Your likely APR, term, and max amount |

| How firm is it | Not a commitment | Conditional commitment |

| Best for | Early browsing | When you’re ready to buy and negotiate |

What does it mean to be prequalified for a car loan?

Being prequalified means a lender has given you an early estimate. It shows how much you might borrow and at roughly what rate. It is based mostly on info you provide. It usually uses a soft credit inquiry. The CFPB says a soft inquiry is a preliminary review that does not affect your credit score. Prequalification is a starting point, not a promise to lend.

Because it’s only an estimate, the numbers can change once you apply. Prequalification is most useful early on. It gives you a sense of your budget with no impact on your credit. The CFPB notes that soft inquiries, including prescreening by lenders, will not affect your credit scores.

What does it mean to be preapproved for a car loan?

Being preapproved means a lender checked your credit and finances. It then made a conditional offer to lend a set amount at a set rate. The FTC explains that by getting preapproved before you shop, you know the terms, including the APR, the length of the loan, and the maximum amount you can borrow. This usually involves a hard credit inquiry.

A preapproval lets you shop like a cash buyer. The FTC says you can use it to comparison shop among dealers and negotiate, because you already have financing in hand. You can still take the dealer’s financing if it beats your offer. Dealers may also push special deals like 0% APR or a cash rebate, so compare those against your preapproval too.

Does getting prequalified or preapproved hurt your credit score?

Prequalification usually uses a soft credit check, which does not affect your score. Preapproval usually uses a hard credit check. The CFPB says a hard check can lower your score, because scoring models look at how recently and often you apply for credit. The effect of one hard inquiry is usually small and temporary.

You can shop without fear of stacking up damage. According to the CFPB, auto-loan inquiries made within 14 to 45 days for the same loan type usually count as one inquiry. And auto-loan inquiries from the 30 days before scoring have no effect on your score. The CFPB’s advice: limit your loan shopping to 14 to 45 days.

Which is better for buying a car: prequalification or preapproval?

Preapproval is usually better when you’re ready to buy. It gives you a real APR, term, and amount to negotiate with. Prequalification is better when you’re just exploring and don’t want any credit-score impact yet. Many buyers prequalify first to compare options. Then they get preapproved when they’re close to buying.

Use this quick guide to decide which one fits your situation:

| Your situation | Better choice |

| You’re months away from buying | Prequalification |

| You want a budget estimate with no credit-score impact | Prequalification |

| You’re worried about a hard credit check right now | Prequalification |

| You’ll buy within the next few weeks | Preapproval |

| You want a real APR, term, and amount to negotiate | Preapproval |

| You want the strongest hand at the dealership | Preapproval |

| You have thin or rebuilding credit | Prequalify first, then get preapproved |

There is no single best choice. It depends on where you are in the process. If you’re weeks away from buying, a preapproval from a bank or credit union gives you the most power to negotiate. If you’re months out, prequalification keeps your options open with no score impact.

Does being prequalified or preapproved guarantee you’ll get the loan?

No. Neither prequalification nor preapproval is a guaranteed loan. Both are conditional. The lender can still change or cancel the offer if your credit, income, or the vehicle don’t check out when you finish the loan. The FTC warns that a deal isn’t final until the financing is fully approved, so confirm the terms before you sign.

Treat a preapproval as a strong starting offer, not a done deal. Final approval depends on checking your details, like income and job. It also depends on the car’s price, age, and mileage. Always read the final contract and make sure it matches the offer you were given.

How to get preapproved for a car loan

To get preapproved, check your credit first, then apply with a few lenders before you visit a dealer, keeping your applications inside the 14-to-45-day window. The CFPB recommends getting preapprovals with different lenders before going to a dealer so you can compare offers and save hundreds or even thousands of dollars over the life of your loan.

- Check your credit reports and scores first. Fix any errors before lenders look. You can get free reports at AnnualCreditReport.com. A higher score usually means a lower rate, so it helps to know what credit score you need for 0% car financing.

- Apply to a few lenders – banks, credit unions, and online lenders – to compare offers.

- Keep applications within 14 to 45 days so the hard checks count as one inquiry (CFPB).

- Compare the full offer, not just the monthly payment: APR, loan term, and amount. See what APR on a car loan means and how to calculate the total cost of a car loan.

- Take your best preapproval to the dealer and let them try to beat it. If they can, great; if not, use your own financing.

If you plan to trade in your current car, check whether you can trade in a financed car and what negative equity means. Both change how much you need to borrow, so your preapproval should leave room for them.

Frequently asked questions

Is auto loan preapproval a hard or soft credit inquiry?

Auto loan preapproval usually involves a hard credit inquiry, because you complete a fuller application and the lender reviews your credit to make a conditional offer. The CFPB says hard inquiries can lower your score slightly. Prequalification, by contrast, usually uses a soft inquiry that does not affect your score.

How long does a car loan preapproval last?

A car loan preapproval lasts for a set window and then expires. The exact length is set by the lender and printed on your offer letter. Common windows run from about 30 to 60 days, but always check your own paperwork. If it lapses before you buy, the lender usually re-checks your credit and may change the rate, so try to choose your car while the offer is still active.

Does prequalification guarantee I’ll be approved for the loan?

No. Prequalification is only an estimate based on limited information, so it does not guarantee approval. When you formally apply, the lender verifies your details and may offer different terms or decline. Treat prequalification as a helpful preview of your options, not a commitment to lend.

Can I still negotiate after I’m preapproved?

Yes. A preapproval actually strengthens your negotiating position. The FTC suggests using your preapproved terms to comparison shop and to ask dealers for a written out-the-door price. You can still accept the dealer’s financing if it beats your preapproval, so it pays to compare both.

How many lenders should I apply to for a car loan?

Applying to several lenders helps you compare offers and find the lowest rate. Keep the applications within 14 to 45 days so they count as one credit inquiry. The CFPB notes that if you finance through a dealer, they may send your information to about five lenders, so keep the process to a few weeks.

Should I get preapproved before going to the dealership?

Yes, getting preapproved before you shop is a smart move. The CFPB recommends getting preapprovals from different lenders before visiting a dealer so you can compare offers. It also lets you focus on the car’s price at the dealership instead of being steered toward a monthly payment.

Will applying for financing at the dealer hurt my credit more?

Not necessarily. Even if a dealer sends your application to several lenders, those auto-loan inquiries generally count as one inquiry if they happen within the 14-to-45-day window. The bigger risk is dragging the process out over many weeks or mixing in other loan types, which can count as separate inquiries.

Related guides on MoneyMentorDesk.com

- What is APR in a car loan?

- How to calculate the total cost of a car loan

- What credit score do you need for 0% car financing?

- What is negative equity?

- Can I trade in a financed car?

- 0% APR vs cash rebate: which is better for car buyers?

About the author

Nimra Saleem is a personal-finance writer at MoneyMentorDesk.com. She turns car-buying, borrowing, and credit topics into plain-English guides that help everyday readers compare their options before they sign. She writes each guide directly from primary sources, including federal regulators like the CFPB and FTC.

Disclosure

This guide is educational only and is not financial advice. Lender rules and credit-scoring practices can change, so confirm details with the official sources below and with any lender before you apply.

Sources

FTC – Financing or Leasing a Car

CFPB – What is a credit inquiry?

CFPB – How will shopping for an auto loan affect my credit?

CFPB – What kind of credit inquiry has no effect on my credit score?

CFPB – What should I know before I shop for a car or auto loan?