When to Refinance a Car Loan (and When to Wait)

Key takeaways

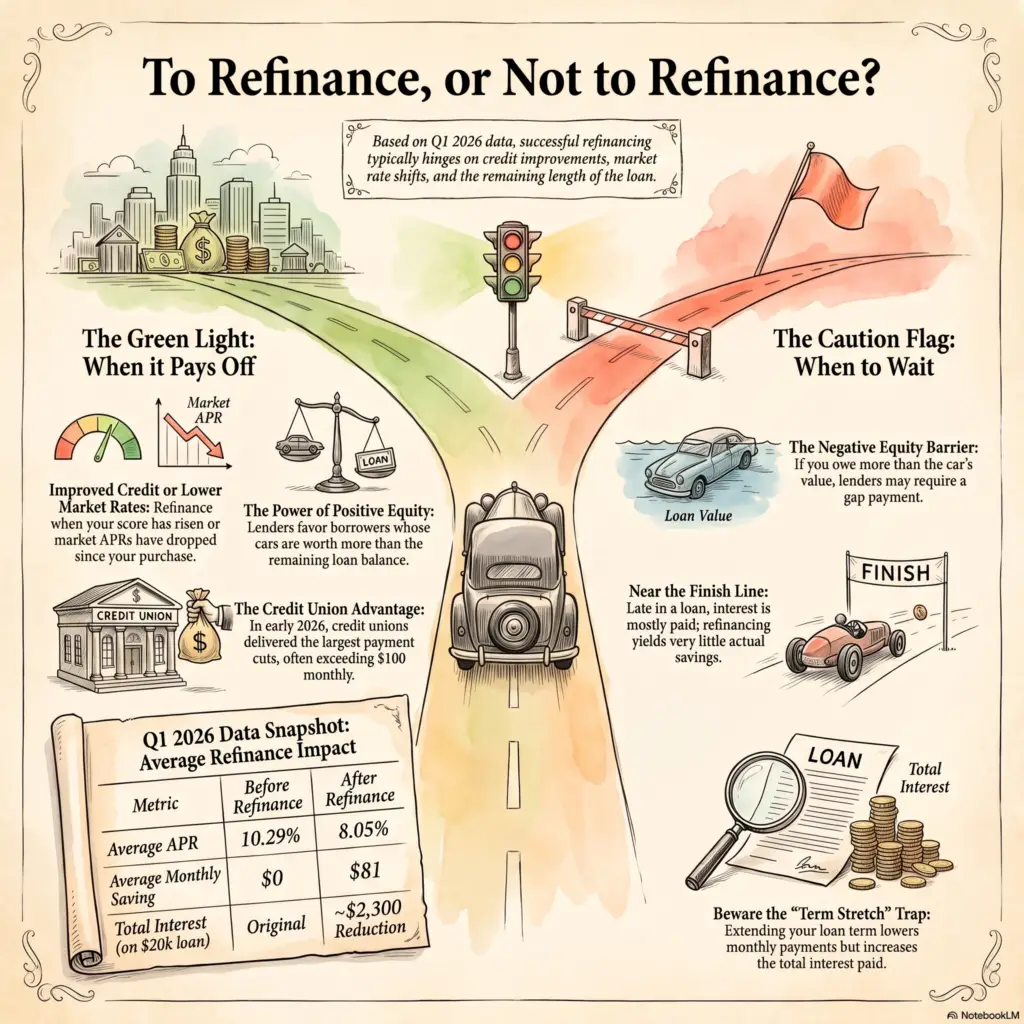

- Refinance when you can lower your APR – usually because rates have dropped or your credit improved – and you still have enough loan left for the savings to beat any fees.

- It’s working for people right now: Experian reports that drivers who refinanced in Q1 2026 cut their rate by about 2.2% (to an average of 8.05%, down from 10.29%) and saved about $81 a month.

- Wait if you’re near the end of the loan, you owe more than the car is worth, or fees and prepayment penalties would eat the savings.

- Lowering your payment by stretching the term can cost more interest overall, even at a lower rate. Compare the total cost, not just the monthly payment.

- Credit unions led auto refinancing in Q1 2026 and gave the biggest payment cut, so they’re a smart first stop.

When should you refinance a car loan?

You should refinance a car loan when you can get a lower APR than you have now, and the savings outweigh any fees. That usually happens when interest rates have fallen since you bought, or when your credit score has improved enough to qualify for a better rate. Refinancing replaces your current loan with a new one, ideally at a lower rate.

The win is real. According to Experian’s State of the Automotive Finance Market (Q1 2026), people who refinanced trimmed about 2.2% off their rate and lowered their payment by roughly $81 a month. But timing matters: refinancing only pays off if you still owe enough, for long enough, that a lower rate saves more than it costs.

Educational only: This is general information, not financial advice. Compare offers and confirms fees with any lender before you refinance.

5 signs it’s a good time to refinance

These are the situations where refinancing usually makes sense. If two or more apply to you, it’s worth getting a quote.

| Sign | Why it helps |

| Rates have dropped since you bought | A lower market rate means a lower APR offer |

| Your credit score went up | A better score moves you into a lower rate tier |

| You got a high rate at the dealer | Banks and credit unions may beat a marked-up dealer rate |

| You have positive equity | The car is worth more than you owe, which lenders like |

| You need a lower monthly payment | A lower rate (or longer term) can cut the payment |

A quick note on that last one: stretching the term lowers the payment but can raise your total interest. Only extend the term if you truly need the breathing room. See how long a car loan should be before you do.

When NOT to refinance your car loan

Refinancing isn’t always smart. Skip it, or wait, in these cases.

- You’re near the end of the loan. Late in a loan, most of your payment already goes to principal, so a lower rate saves little. The interest is mostly behind you.

- You have negative equity. If you owe more than the car is worth, many lenders won’t refinance, or you’d have to pay the difference first. Check what negative equity is.

- Fees or prepayment penalties eat the savings. Some loans charge a penalty for paying off early. The FTC says to check your contract for prepayment terms. If the penalty plus refinance fees wipe out your savings, don’t bother.

- Your credit got worse. A lower score usually means a higher rate, not a lower one.

- You only want a smaller payment. If you’d get that only by stretching the term, you may pay more interest overall, even at a lower rate.

How much can refinancing save you?

Refinancing saves you money in two ways: a lower monthly payment and less total interest. The bigger your rate drop and the more you still owe, the bigger the savings. Experian’s Q1 2026 data put the average refinance saving at about $81 a month.

Here’s an illustration. Say you owe $20,000 with 60 months left and you cut your rate from 11% to 7% APR:

- Monthly payment drops from about $435 to about $396 – roughly $39 a month.

- Total interest falls by roughly $2,300 over the life of the loan.

Illustration only, calculated with a standard loan formula; your numbers will differ. To run your own totals, see how to calculate the total cost of a car loan and what APR on a car loan means.

How soon can you refinance a car loan after buying?

There’s usually no hard rule, but most drivers wait a few months. Your new lender needs your loan’s title and payoff details, which can take several weeks to process after you buy. Many lenders also like to see a few on-time payments first, so waiting around 6 months often makes refinancing smoother and your credit a little stronger.

There’s no benefit to rushing. Rates and your credit are what move the savings – not how fast you refinance. Get your 10-day payoff quote from your current lender when you’re ready to compare offers.

Where to refinance a car loan

You can refinance with a bank, a credit union, or an online lender – not just your current lender. It pays to shop around. In Q1 2026, Experian found that credit unions handled the largest share of auto refinancing and delivered the biggest payment cut, over $100 a month on average for those who used them.

Apply to two or three lenders and compare. The CFPB notes that auto-loan rate shopping within a 14-to-45-day window counts as a single credit inquiry, so comparing offers quickly protects your score. To understand the lender types, see dealer vs bank financing.

How to refinance a car loan, step by step

Refinancing is faster than buying a car, but the order matters. Follow these steps.

- Check your credit and your current rate. Know your score and the APR you’re paying now, so you can tell if an offer is actually better.

- Get your payoff amount from your current lender (a written 10-day payoff quote).

- Shop two or three lenders – include a credit union – within a 14-to-45-day window so the inquiries count as one (CFPB).

- Compare the full offer, not just the payment: APR, term, fees, and total amount you’ll repay.

- Apply, then close. The new lender pays off your old loan, and you start paying the new one. Confirm the old loan shows as closed.

Want to know your odds before a hard pull? Many lenders let you check a rate with a soft check first – see prequalified vs preapproved.

Frequently asked questions

When should you refinance a car loan?

Refinance when you can lower your APR and the savings beat any fees. The most common triggers are interest rates falling since you bought or your credit score improving enough to qualify for a better rate. It works best when you still owe a meaningful balance with at least a couple of years left.

How soon can you refinance a car loan after buying it?

There’s usually no fixed waiting period, but the title and payoff details can take several weeks to process, and many lenders prefer a few on-time payments first. Waiting about six months often makes the process smoother and gives your credit time to strengthen.

Does refinancing a car loan hurt your credit?

There’s a small, temporary dip from the hard inquiry and the new account. But if you shop several lenders within a 14-to-45-day window, the CFPB says those inquiries count as one. On-time payments on the new loan rebuild any small dip over time.

Can you refinance a car with negative equity?

It’s hard. If you owe more than the car is worth, many lenders won’t approve a refinance, or they’ll ask you to pay down the difference first. You may need to wait until you have positive equity, or make extra principal payments to get there.

Will refinancing lower my monthly payment?

It can, in two ways: a lower APR, or a longer term. A lower rate saves you money overall. A longer term lowers the payment but can raise your total interest, so only stretch the term if you truly need the lower payment.

Is it worth refinancing for a 1% or 2% rate drop?

Often, yes, if you still owe a sizable balance. Experian found Q1 2026 refinancers cut their rate by about 2.2% and saved roughly $81 a month. On a larger balance with years left, even a 1-2 point drop can save four figures over the loan. Check that fees don’t erase it.

Where is the best place to refinance a car loan?

Compare a few options. Credit unions led auto refinancing in Q1 2026 and gave the biggest payment cut, so they’re a strong first stop, but banks and online lenders are worth quoting too. The best deal is the lowest total cost, not just the lowest payment.

About the author

Nimra Saleem is a personal-finance writer at MoneyMentorDesk.com. She turns car-buying, borrowing, and credit topics into plain-English guides that help everyday readers compare their options before they sign. She writes each guide directly from primary sources, including the CFPB, the FTC, and official Experian auto-finance data.

Disclosure

This guide was written by Nimra Saleem for MoneyMentorDesk.com and reviewed against Consumer Financial Protection Bureau (CFPB), Federal Trade Commission (FTC), and Experian auto-finance data. It is educational only and is not financial advice. Rates, fees, and lender rules change, so confirm details with the official sources below and with any lender before you refinance.